UP Board Class 10 Commerce Question Paper 2024 PDF is available for download here. The Commerce exam was conducted on February 22, 2024 in the Afternoon Shift from 2:00 PM to 5:15 PM. The total marks for the theory paper are 70. Students reported the paper to be easy to moderate.

UP Board Class 10 Commerce Question Paper 2024 with Solutions

| UP Board Class 10 Commerce 2024 Question Paper with Answer Key | Check Solutions |

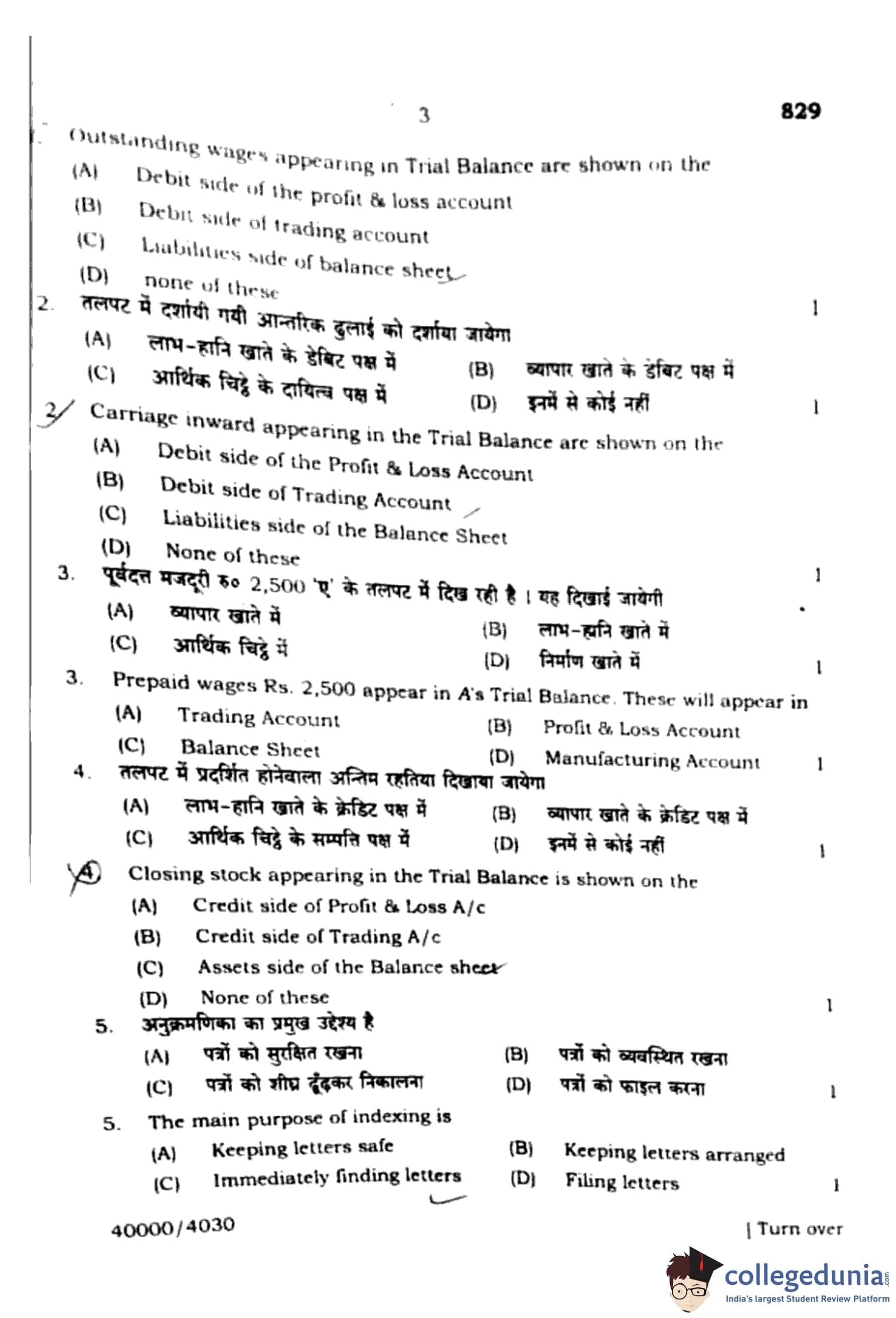

Outstanding wages appearing in the Trial Balance are shown on the:

View Solution

Step 1: Understanding Outstanding Wages.

Outstanding wages means the wages which are payable but not yet paid. Since these represent future obligations, they are considered as liabilities.

Step 2: Position in Financial Statements.

Outstanding wages do not appear on the debit side of the Profit \& Loss Account or the Trading Account. Instead, they are shown on the liabilities side of the Balance Sheet.

Step 3: Analyzing the Options.

(A) Debit side of the Profit \& Loss Account: Incorrect, as wages are expenses but outstanding wages are liability.

(B) Debit side of Trading Account: Incorrect, it does not relate to trading account.

(C) Liabilities side of the Balance Sheet: Correct, because outstanding wages are future obligations.

(D) None of these: Incorrect, since (C) is the correct choice.

Step 4: Conclusion.

Hence, the correct answer is (C) Liabilities side of the Balance Sheet.

Quick Tip: Outstanding expenses are always shown on the Liabilities side of the Balance Sheet since they represent obligations that are yet to be paid.

Carriage inward appearing in the Trial Balance is shown on the:

View Solution

Step 1: Understanding Carriage Inward.

Carriage inward refers to the transportation cost incurred to bring goods to the business premises. This is a direct expense related to purchasing goods.

Step 2: Position in Financial Statements.

Since carriage inward is a direct expense, it is shown on the debit side of the Trading Account, along with purchases, wages, and other direct costs.

Step 3: Analyzing the Options.

(A) Debit side of the Profit \& Loss Account: Incorrect, since it is not an indirect expense.

(B) Debit side of Trading Account: Correct, because it is a direct expense incurred for bringing goods.

(C) Liabilities side of the Balance Sheet: Incorrect, carriage inward is not a liability.

(D) None of these: Incorrect, since option (B) is correct.

Step 4: Conclusion.

Thus, the correct answer is (B) Debit side of Trading Account.

Quick Tip: Remember: Direct expenses like carriage inward are shown on the Debit side of the Trading Account, while indirect expenses go to the Profit \& Loss Account.

Prepaid wages Rs. 2,500 appear in A's Trial Balance. These will appear in:

View Solution

Step 1: Understanding Prepaid Wages.

Prepaid wages are the expenses which have been paid in advance for the next accounting period. These are not current expenses but future benefits.

Step 2: Position in Financial Statements.

Prepaid wages are shown as an asset in the Balance Sheet because they represent payments made in advance which will give benefit in the future.

Step 3: Analyzing the Options.

(A) Trading Account – Incorrect, as prepaid wages are not a trading expense for the current year.

(B) Profit \& Loss Account – Incorrect, they are not current expenses.

(C) Balance Sheet – Correct, shown under Current Assets.

(D) Manufacturing Account – Incorrect, since not related to manufacturing cost.

Step 4: Conclusion.

Hence, prepaid wages are shown in the Balance Sheet.

Quick Tip: Prepaid expenses are always shown as current assets in the Balance Sheet.

Closing stock appearing in the Trial Balance is shown on the:

View Solution

Step 1: Understanding Closing Stock.

Closing stock is the value of unsold goods at the end of an accounting period. If it is given in the Trial Balance, it means it has already been adjusted.

Step 2: Position in Financial Statements.

When closing stock is given in the Trial Balance, it is shown only in the Balance Sheet under Assets. It is not shown in the Trading Account again (to avoid double entry).

Step 3: Analyzing the Options.

(A) Credit side of Profit \& Loss A/c – Incorrect.

(B) Credit side of Trading A/c – Incorrect, already adjusted.

(C) Assets side of the Balance Sheet – Correct, since stock is an asset.

(D) None of these – Incorrect.

Step 4: Conclusion.

Thus, closing stock (when in Trial Balance) is shown on the Assets side of the Balance Sheet.

Quick Tip: Remember: If closing stock is given in the Trial Balance, show it only in the Balance Sheet. If it is outside the Trial Balance, show it in both Trading A/c (credit side) and Balance Sheet (assets side).

The main purpose of indexing is:

View Solution

Step 1: Understanding Indexing.

Indexing refers to the method of systematically arranging records or documents so that they can be quickly located when required.

Step 2: Analyzing the Options.

(A) Keeping letters safe – Incorrect, this is filing, not indexing.

(B) Keeping letters arranged – Partly correct, but arrangement alone is not the main purpose.

(C) Immediately finding letters – Correct, indexing ensures fast and accurate retrieval of documents.

(D) Filing letters – Incorrect, filing is a separate process of preserving documents.

Step 3: Conclusion.

The main purpose of indexing is to immediately find letters or records easily.

Quick Tip: Indexing = Easy retrieval. Filing = Safe storage. Always remember this difference.

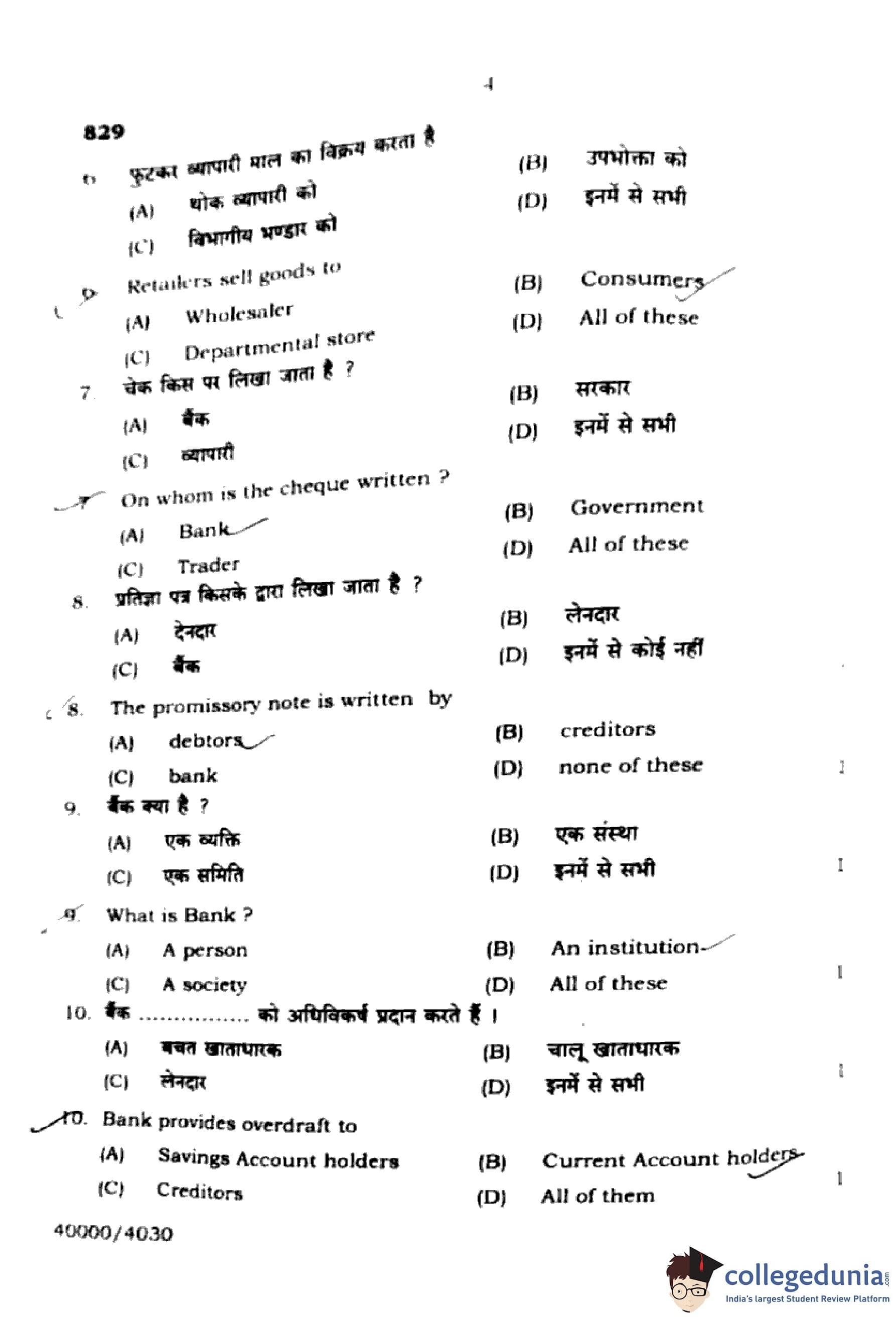

Retailers sell goods to:

View Solution

Step 1: Understanding retailers.

Retailers are the last link in the distribution chain. They buy goods from wholesalers and sell directly to the consumers.

Step 2: Analyzing the options.

(A) Wholesaler – Incorrect, retailers buy from wholesalers but do not sell to them.

(B) Consumers – Correct, retailers sell goods directly to consumers.

(C) Departmental store – Incorrect, it is also a type of retailer, not the buyer.

(D) All of these – Incorrect, since the correct and specific answer is consumers.

Step 3: Conclusion.

Thus, retailers sell goods to consumers.

Quick Tip: Always remember: Wholesaler → Retailer → Consumer.

On whom is the cheque written?

View Solution

Step 1: Understanding cheques.

A cheque is an unconditional order drawn by the account holder, directing the bank to pay a certain sum of money.

Step 2: Analyzing the options.

(A) Bank – Correct, because the cheque is always written on a bank.

(B) Government – Incorrect, cheques are not written on government.

(C) Trader – Incorrect, traders are not the drawee of cheques.

(D) All of these – Incorrect.

Step 3: Conclusion.

Hence, the cheque is always written on the bank.

Quick Tip: A cheque is always drawn on a bank where the drawer holds an account.

The promissory note is written by:

View Solution

Step 1: Understanding promissory notes.

A promissory note is a written promise made by one party (the debtor) to pay a certain sum of money to another party (the creditor).

Step 2: Analyzing the options.

(A) Debtors – Correct, because the debtor makes the promise to pay.

(B) Creditors – Incorrect, creditors receive the payment.

(C) Bank – Incorrect, though banks may hold promissory notes, they are not the writers.

(D) None of these – Incorrect.

Step 3: Conclusion.

Therefore, a promissory note is always written by the debtor.

Quick Tip: Debtor = Maker of the promissory note. Creditor = Payee.

What is Bank?

View Solution

Step 1: Understanding Bank.

A bank is a financial institution that accepts deposits, provides loans, and performs other financial services. It is not an individual or society in itself.

Step 2: Analyzing the options.

(A) A person – Incorrect, a bank is not a single person.

(B) An institution – Correct, a bank is a financial institution.

(C) A society – Incorrect, although some banks may be cooperative societies, in general a bank is not defined as one.

(D) All of these – Incorrect, as the precise definition is institution.

Step 3: Conclusion.

Thus, the correct answer is that a bank is an institution.

Quick Tip: Always define a bank as a financial institution that accepts deposits and provides credit.

Bank provides overdraft to:

View Solution

Step 1: Understanding overdraft.

Overdraft facility allows account holders to withdraw more than the available balance in their account, up to a certain limit approved by the bank.

Step 2: Position in practice.

This facility is generally provided only to Current Account holders, not to Savings Account holders or creditors.

Step 3: Analyzing the options.

(A) Savings Account holders – Incorrect, no overdraft facility.

(B) Current Account holders – Correct, overdraft is mainly for business persons with current accounts.

(C) Creditors – Incorrect, overdraft is unrelated to creditors.

(D) All of them – Incorrect.

Step 4: Conclusion.

Hence, overdraft is provided to Current Account holders.

Quick Tip: Remember: Overdraft = facility for Current Account holders only.

Reserve Bank of India was established in:

View Solution

Step 1: Historical fact.

The Reserve Bank of India (RBI) was established on 1st April 1935 under the Reserve Bank of India Act, 1934.

Step 2: Analyzing the options.

(A) 1935 – Correct.

(B) 1949 – Incorrect, this is when RBI was nationalized.

(C) 1401 – Incorrect, irrelevant year.

(D) 1619 – Incorrect.

Step 3: Conclusion.

Therefore, RBI was established in the year 1935.

Quick Tip: RBI established: 1935; Nationalized: 1949.

One rupee coin is minted in India by:

View Solution

Step 1: Understanding minting authority.

Coins in India are issued and minted by the Government of India under the Coinage Act.

Step 2: RBI’s role.

While RBI issues currency notes (except one rupee note), coins including the one rupee coin are issued by the Government of India.

Step 3: Analyzing the options.

(A) Reserve Bank of India – Incorrect, RBI issues notes, not coins.

(B) State Bank of India – Incorrect, not authorized to issue coins.

(C) Government of India – Correct, authority to mint coins.

(D) Commercial Banks – Incorrect.

Step 3: Conclusion.

Thus, the one rupee coin is minted by the Government of India.

Quick Tip: Coins = Government of India; Currency notes (₹2 and above) = Reserve Bank of India.

First of all Commercial Banks were nationalized in the year:

View Solution

Step 1: Background.

Nationalization of banks in India was done in two phases to bring major banks under government control.

Step 2: First phase.

In 1969, 14 major commercial banks were nationalized. This marked the beginning of government-controlled banking.

Step 3: Second phase.

In 1980, another 6 banks were nationalized.

Step 4: Analyzing the options.

(A) 1949 – Incorrect, this was RBI’s nationalization.

(B) 1969 – Correct, first bank nationalization of 14 banks.

(C) 1971 – Incorrect.

(D) 1980 – Incorrect, this was the second phase.

Step 5: Conclusion.

Thus, the first nationalization of commercial banks occurred in 1969.

Quick Tip: Bank Nationalization: 1st phase – 1969 (14 banks); 2nd phase – 1980 (6 banks).

Who controls commercial banks?

View Solution

Step 1: Control of banking system.

The Reserve Bank of India (RBI) is the central bank of the country and regulates all commercial banks.

Step 2: Role of RBI.

RBI controls monetary policy, supervises lending, deposits, and overall functioning of commercial banks.

Step 3: Analyzing options.

(A) Government of India – Incorrect, it frames policies but does not directly control banks.

(B) State Bank of India – Incorrect, it is only one bank, not a regulator.

(C) NABARD – Incorrect, it focuses on rural/agricultural credit.

(D) Reserve Bank of India – Correct, regulator of all banks.

Step 4: Conclusion.

Hence, commercial banks are controlled by the Reserve Bank of India.

Quick Tip: RBI is called the "Bank of Banks" because it regulates all commercial banks in India.

The reason for the conversion of Imperial Bank into State Bank was:

View Solution

Step 1: Background.

Imperial Bank of India was converted into the State Bank of India (SBI) in 1955.

Step 2: Reasons.

The Imperial Bank ignored agricultural finance, misused authorities, and had a defective branch expansion policy, limiting rural banking.

Step 3: Analyzing options.

(A) Ignorance of agricultural business – True, Imperial Bank was urban focused.

(B) Misuse of authorities – True, management issues existed.

(C) Defective branch policy – True, branches were not opened in rural areas.

(D) All of these – Correct, all were reasons.

Step 4: Conclusion.

Therefore, the Imperial Bank was converted into SBI due to all of these reasons.

Quick Tip: SBI was formed to expand banking in rural India and strengthen agricultural finance.

Which of the following will come under the category of indigenous bankers?

View Solution

Step 1: Understanding indigenous bankers.

Indigenous bankers are private money lenders or traditional financial intermediaries, often operating in local communities.

Step 2: Analyzing the options.

(A) Co-operative Bank – Incorrect, it is an organized bank.

(B) Mahajan – Correct, traditional moneylenders are indigenous bankers.

(C) Land Development Bank – Incorrect, deals with agricultural loans.

(D) Regional Rural Bank – Incorrect, these are scheduled banks, not indigenous.

Step 3: Conclusion.

Thus, indigenous bankers include Mahajans.

Quick Tip: Indigenous bankers = Mahajans, Seths, Shroffs, who lend money locally.

Exception to the law of diminishing marginal utility includes:

View Solution

Step 1: Understanding the law.

The law of diminishing marginal utility states that as a consumer consumes more units of a commodity, the additional satisfaction (utility) decreases.

Step 2: Exceptions.

- In case of money, more money increases satisfaction.

- In case of knowledge, more knowledge gives more utility.

- In case of hobbies like reading, satisfaction keeps increasing.

Step 3: Analyzing options.

(A) Reading – Exception.

(B) Money – Exception.

(C) Acquiring knowledge – Exception.

(D) All of these – Correct, as all listed cases are exceptions.

Step 4: Conclusion.

Therefore, all given examples are exceptions to the law of diminishing marginal utility.

Quick Tip: Law of Diminishing Utility applies to most goods, but not to money, knowledge, or hobbies.

We should keep our savings in banks because:

View Solution

Step 1: Understanding the purpose of savings in banks.

Banks provide a secure place to keep money. Savings accounts offer interest and provide liquidity as money can be withdrawn when needed.

Step 2: Analyzing the options.

(A) It is safe – Correct, banks keep deposits secure.

(B) It earns interest – Correct, savings earn interest.

(C) Can be withdrawn – Correct, savings can be withdrawn at any time.

(D) All of these – Correct, because all reasons are valid.

Step 3: Conclusion.

Thus, the correct answer is All of these.

Quick Tip: Saving in banks provides security, interest, and liquidity.

According to economical point of view a co-operative bank is an organisation of:

View Solution

Step 1: Understanding Co-operative Banks.

Co-operative banks are set up to serve the needs of weaker sections of society, especially poor farmers and small borrowers.

Step 2: Analyzing the options.

(A) Labourers – Not specifically labourers.

(B) Weak individuals – Not precise.

(C) Rich individuals – Incorrect, co-operative banks are not meant for the rich.

(D) Poor farmers – Correct, co-operative banks focus on providing credit to poor farmers.

Step 3: Conclusion.

Thus, co-operative banks are organisations of poor farmers.

Quick Tip: Co-operative banks are designed to provide financial support to farmers and rural communities.

Function of commercial banks is to:

View Solution

Step 1: Primary functions of commercial banks.

The main functions include accepting deposits, providing loans, and offering agency services.

Step 2: Analyzing the options.

(A) Accept deposits – Correct, banks accept deposits from the public.

(B) Provide loans – Correct, banks lend money to individuals and businesses.

(C) Work as an agent – Correct, banks provide services like payment, transfer, etc.

(D) All of these – Correct, because all listed functions are true.

Step 3: Conclusion.

Thus, the function of commercial banks is all of these.

Quick Tip: Commercial banks = Accept deposits + Provide loans + Offer agency services.

What is Net Profit?

View Solution

Step 1: Definition.

Net Profit is the profit remaining with a business after deducting all operating expenses, interest, depreciation, and taxes from the total revenue.

Step 2: Formula.

\[ Net Profit = Total Revenue - (Operating Expenses + Interest + Taxes + Depreciation) \]

Step 3: Importance.

Net Profit shows the actual profitability and financial health of a business. It is also known as “bottom line profit.”

Step 4: Conclusion.

Thus, Net Profit is the surplus income left with the business after meeting all expenses and liabilities.

Quick Tip: Gross Profit = before expenses. Net Profit = after all expenses.

State any two benefits of indexing.

View Solution

Step 1: Understanding indexing.

Indexing is the process of arranging records or documents in a systematic way so that they can be easily located.

Step 2: Benefits.

1. It saves time by allowing quick retrieval of documents.

2. It helps in systematic and scientific arrangement of records.

Step 3: Conclusion.

Thus, indexing provides efficiency in office work by making information retrieval easy and organized.

Quick Tip: Indexing = Easy search of records; Filing = Safe storage of records.

What functions does the State Bank perform as a commercial bank?

View Solution

Step 1: Primary functions.

- Accepting deposits from the public.

- Providing loans and advances.

Step 2: Secondary functions.

- Acting as an agent (collection of cheques, drafts, etc.).

- Providing facilities like overdraft, safe deposits, and remittances.

Step 3: Conclusion.

Thus, the State Bank, as a commercial bank, performs both deposit-taking and lending functions, along with customer service and financial facilities.

Quick Tip: Commercial Banks = Accept deposits + Provide loans + Offer agency services.

What do you understand by crossing of cheque?

View Solution

Step 1: Meaning.

Crossing of cheque means drawing two parallel lines on the face of a cheque, with or without the words “\& Co.” or “Account Payee Only.”

Step 2: Purpose.

Crossing ensures that the cheque cannot be encashed directly at the counter; it must be deposited in a bank account, which adds safety.

Step 3: Types of crossing.

- General crossing.

- Special crossing.

Step 4: Conclusion.

Thus, crossing of cheque is a security feature that prevents misuse and ensures safe transfer through banks.

Quick Tip: Always cross cheques before sending to others—it prevents direct cash encashment.

What do you understand by law of diminishing returns?

View Solution

Step 1: Definition.

The law of diminishing returns states that as more and more units of a variable factor (e.g., labour) are added to a fixed factor (e.g., land), after a certain point, the marginal (additional) output decreases.

Step 2: Example.

If labour is continuously added to a fixed piece of land, initially output increases, but later, each additional worker adds less output than the previous one.

Step 3: Importance.

It explains the limits of production and helps in resource allocation.

Step 4: Conclusion.

Thus, the law highlights that productivity does not increase proportionately with inputs when one factor is fixed.

Quick Tip: Law of Diminishing Returns = “Too many inputs with fixed resources → falling efficiency.”

Write any two merits and two demerits of wholesale trade.

View Solution

Step 1: Understanding wholesale trade.

Wholesale trade refers to buying goods in bulk from manufacturers and selling them in smaller lots to retailers.

Step 2: Merits.

1. Wholesalers help manufacturers by buying in bulk and reducing their storage burden.

2. Wholesalers provide goods to retailers in smaller quantities, ensuring availability.

Step 3: Demerits.

1. Presence of wholesalers may increase the cost of goods, as they add profit margins.

2. Sometimes wholesalers create artificial scarcity by hoarding goods.

Step 4: Conclusion.

Thus, wholesale trade is useful for smooth distribution but has drawbacks like higher prices and hoarding.

Quick Tip: Wholesaler = Link between manufacturer and retailer.

Explain the importance of filing.

View Solution

Step 1: Meaning of filing.

Filing is the systematic arrangement and preservation of office records and correspondence for easy reference.

Step 2: Importance.

1. Provides safety and security to documents.

2. Helps in quick reference and decision-making.

3. Protects against loss or damage of records.

4. Facilitates smooth functioning of office by keeping information organized.

Step 3: Conclusion.

Filing ensures systematic storage and easy retrieval of office documents.

Quick Tip: Filing = Safe storage; Indexing = Easy retrieval.

Write four features of a co-operative bank.

View Solution

Step 1: Understanding co-operative banks.

Co-operative banks are financial institutions established on co-operative principles to provide credit to members, especially farmers and weaker sections.

Step 2: Features.

1. Democratic control – one member, one vote system.

2. Aim is to provide service, not profit maximization.

3. Provides credit at reasonable interest rates.

4. Works for the welfare of poor farmers, small borrowers, and rural people.

Step 3: Conclusion.

Co-operative banks play a vital role in rural development and inclusive finance.

Quick Tip: Co-operative banks are service-oriented, not profit-oriented.

What is the difference between Cheque and Hundi?

View Solution

Step 1: Meaning of Cheque.

A cheque is a negotiable instrument drawn on a bank, directing it to pay a certain amount to a specified person.

Step 2: Meaning of Hundi.

A Hundi is a traditional Indian financial instrument used as a bill of exchange or promissory note, often outside the formal banking system.

Step 3: Key Differences.

1. Cheque is issued under the Negotiable Instruments Act; Hundi is based on custom and practice.

2. Cheque is always drawn on a bank; Hundi may be drawn on individuals or firms.

3. Cheques are used widely in modern banking; Hundis are traditional and less formal.

Step 4: Conclusion.

Thus, while both are negotiable instruments, cheques are modern and regulated, whereas Hundis are traditional and customary.

Quick Tip: Cheque = Modern, regulated. Hundi = Traditional, customary.

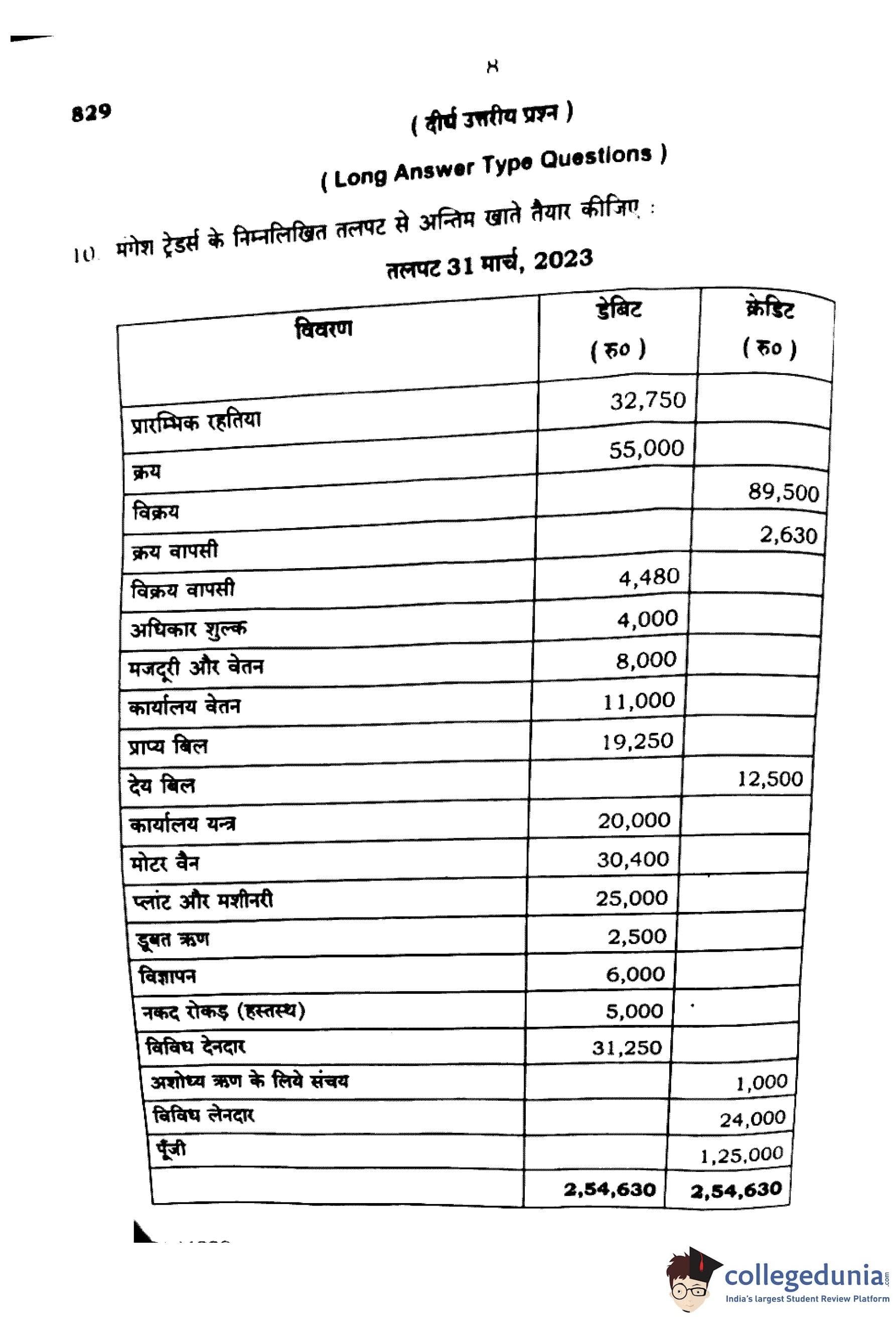

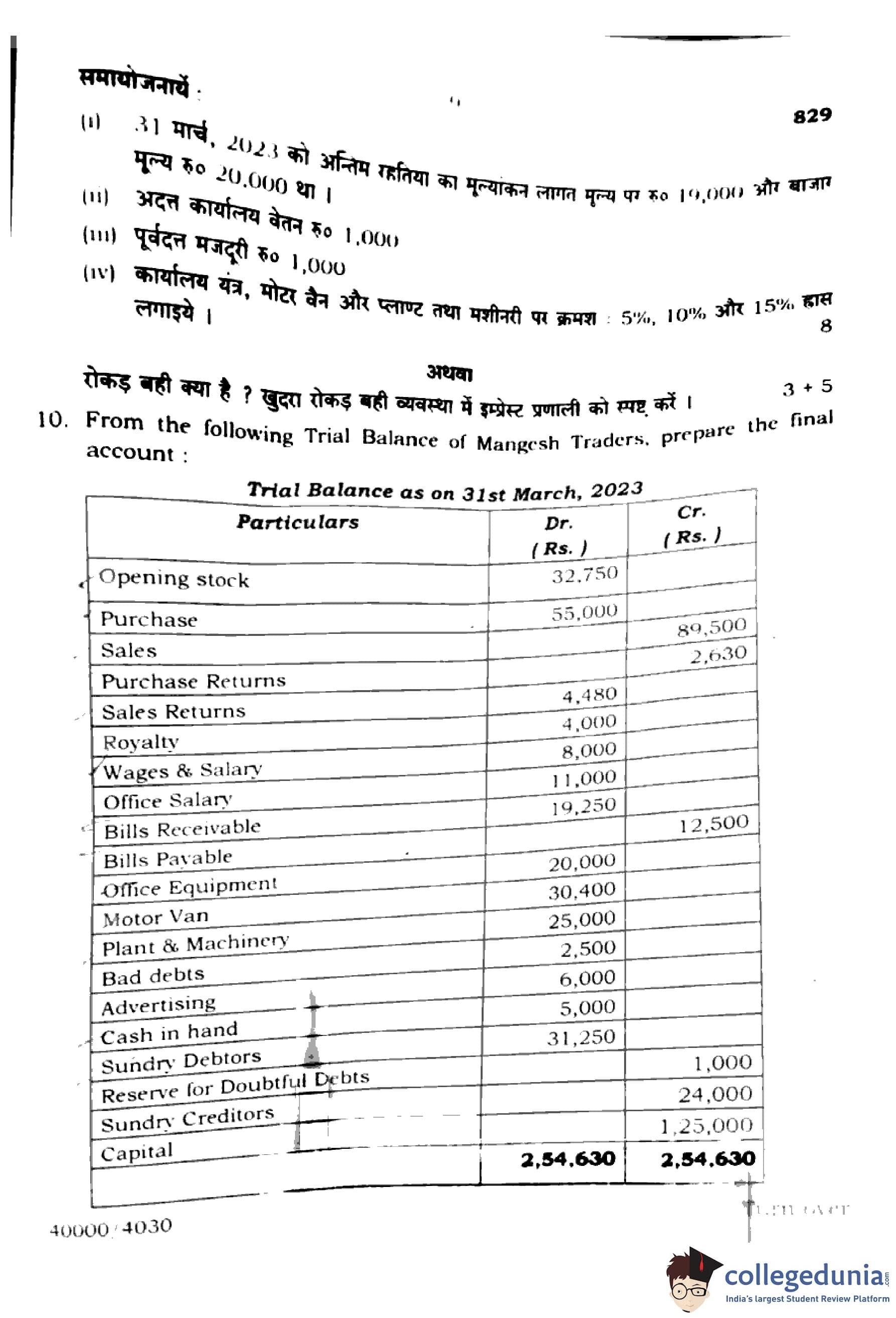

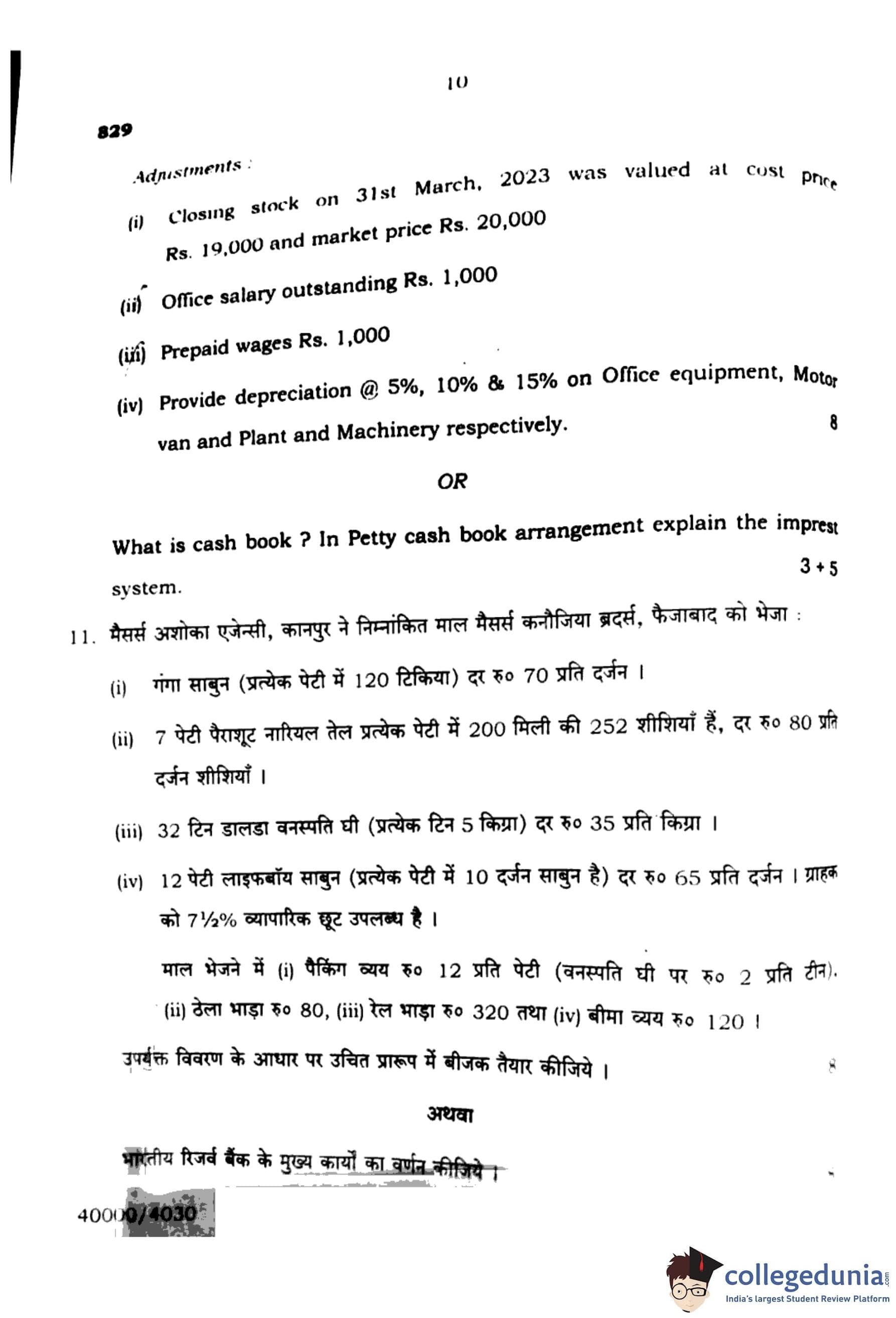

From the following Trial Balance of Mangesh Traders as on 31st March, 2023, prepare the Final Accounts:

% Trial Balance Table

\begin{tabular{|l|c|c|

\hline

Particulars & Dr. (Rs.) & Cr. (Rs.)

\hline

Opening Stock & 32,750 & --

Purchases & 55,000 & --

Sales & -- & 89,500

Purchase Returns & 4,480 & --

Sales Returns & 4,000 & --

Royalty & 8,000 & --

Wages \& Salary & 11,000 & --

Office Salary & 19,250 & --

Bills Receivable & 12,500 & --

Bills Payable & -- & 20,000

Office Equipment & 30,400 & --

Motor Van & 25,000 & --

Plant \& Machinery & 2,500 & --

Bad Debts & 6,000 & --

Advertising & 5,000 & --

Cash in Hand & 31,250 & --

Sundry Debtors & 40,000 & --

Reserve for Doubtful Debts & -- & 24,000

Sundry Creditors & -- & 1,25,000

Capital & -- & 2,54,630

\hline

Total & 2,54,630 & 2,54,630

\hline

\end{tabular

% Adjustments

Adjustments:

(i) Closing stock on 31st March, 2023 valued at Rs. 19,000 (market price Rs. 20,000).

(ii) Office salary outstanding Rs. 1,000.

(iii) Prepaid wages Rs. 1,000.

(iv) Provide depreciation: 5% on Office Equipment, 10% on Motor Van, 15% on Plant \& Machinery.

View Solution

Step 1: Trading Account for the year ending 31st March, 2023.

\begin{tabular{|l|c|c|

\hline

Particulars & Amount (Rs.) & Amount (Rs.)

\hline

Opening Stock & 32,750 & --

Purchases & 55,000 & --

Less: Purchase Returns & (4,480) & 50,520

Wages \& Salary (11,000 - 1,000 Prepaid) & 10,000 & --

Gross Profit c/d (Balancing Figure) & 19,230 & --

\hline

& 1,12,500 & 1,12,500

\hline

Sales & -- & 89,500

Less: Sales Returns & -- & (4,000)

Net Sales & -- & 85,500

Closing Stock & -- & 19,000

\hline

& -- & 1,04,500

\hline

\end{tabular

Step 2: Profit \& Loss Account for the year ending 31st March, 2023.

\begin{tabular{|l|c|c|

\hline

Particulars & Amount (Rs.) & Amount (Rs.)

\hline

Gross Profit b/d & -- & 19,230

Royalty & 8,000 & --

Office Salary (19,250 + 1,000 O/s) & 20,250 & --

Bad Debts & 6,000 & --

Advertising & 5,000 & --

Depreciation on: & &

\quad Office Equipment (30,400 × 5%) & 1,520 & --

\quad Motor Van (25,000 × 10%) & 2,500 & --

\quad Plant \& Machinery (2,500 × 15%) & 375 & --

Net Loss (Balancing Figure) & 24,915 & --

\hline

& 68,560 & 19,230

\hline

\end{tabular

Step 3: Balance Sheet of Mangesh Traders as on 31st March, 2023.

\begin{tabular{|l|c|l|c|

\hline

Liabilities & Amount (Rs.) & Assets & Amount (Rs.)

\hline

Capital & 1,25,000 & Cash in Hand & 31,250

Less: Net Loss & (24,915) & Sundry Debtors & 40,000

Adjusted Capital & 1,00,085 & Less: Reserve for Doubtful Debts & (24,000)

Bills Payable & 20,000 & Net Debtors & 16,000

Sundry Creditors & 24,000 & Bills Receivable & 12,500

Outstanding Office Salary & 1,000 & Closing Stock & 19,000

& & Office Equipment (30,400 - 1,520 Dep.) & 28,880

& & Motor Van (25,000 - 2,500 Dep.) & 22,500

& & Plant \& Machinery (2,500 - 375 Dep.) & 2,125

\hline

Total & 1,45,085 & Total & 1,45,085

\hline

\end{tabular

% Conclusion

Conclusion:

The Final Accounts of Mangesh Traders show a Net Loss of Rs. 24,915 and the Balance Sheet balances at Rs. 1,45,085.

Quick Tip: Always apply adjustments like closing stock, outstanding/prepaid expenses, and depreciation carefully—they affect both Profit \& Loss A/c and Balance Sheet.

What is Cash Book? In Petty Cash Book arrangement explain the Imprest System.

View Solution

Step 1: Meaning of Cash Book.

A cash book is a subsidiary book of accounts that records all cash transactions—both receipts and payments—on a daily basis. It functions both as a journal and a ledger for cash transactions.

Step 2: Features of Cash Book.

1. It records only cash and bank transactions.

2. It has debit and credit sides, like a ledger.

3. The balance of the cash book always shows a debit balance (since cash cannot be negative).

Step 3: Petty Cash Book.

A petty cash book is a record maintained to track small day-to-day expenses such as postage, stationery, carriage, etc. These expenses are recorded by a petty cashier under a fixed system.

Step 4: The Imprest System.

- Under the imprest system, a fixed amount (say Rs. 5,000) is given to the petty cashier at the beginning of a period (week or month).

- During the period, the cashier spends from this amount on minor expenses and records them.

- At the end of the period, the petty cashier submits vouchers and receipts.

- The amount spent is reimbursed, so that the petty cashier again starts the next period with the same fixed imprest amount.

Step 5: Advantages of Imprest System.

1. Controls petty expenses effectively.

2. Avoids misuse of cash.

3. Saves time of the main cashier.

4. Provides a systematic record of all minor expenditures.

Step 6: Conclusion.

Thus, a cash book records all cash transactions, while the petty cash book (under the imprest system) ensures efficient control over small routine expenses.

Quick Tip: Imprest System = “Fixed float of petty cash is maintained and reimbursed after spending.”

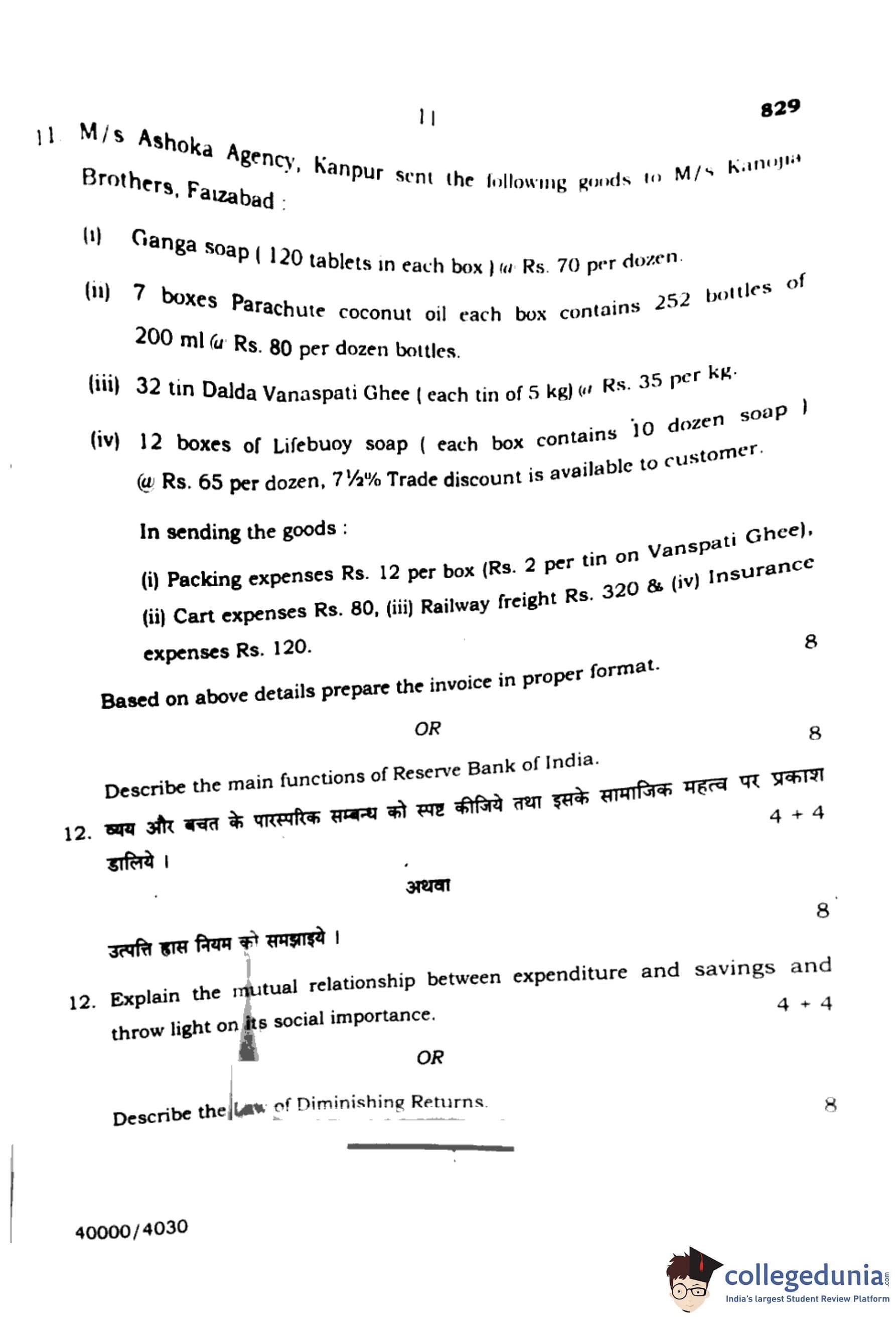

M/s Ashoka Agency, Kanpur sent the following goods to M/s Kanpuria Brothers, Faizabad:

(1) Ganga Soap (120 tablets in each box) at Rs. 70 per dozen.

(2) 7 boxes Parachute Coconut Oil, each box contains 252 bottles of 200 ml @ Rs. 80 per dozen bottles.

(3) 32 tins Dalda Vanaspati Ghee (each tin of 5 kg) @ Rs. 35 per kg.

(4) 12 boxes Lifebuoy Soap (each box contains 10 dozen soap) @ Rs. 65 per dozen.

7.5% Trade discount is available to the customer.

In sending the goods:

(i) Packing expenses Rs. 12 per box (Rs. 2 per tin on Vanaspati Ghee).

(ii) Cart expenses Rs. 80.

(iii) Railway freight Rs. 320.

(iv) Insurance expenses Rs. 120.

Based on the above details, prepare the invoice in proper format.

View Solution

M/s Ashoka Agency, Kanpur

Invoice to: M/s Kanpuria Brothers, Faizabad

\begin{tabular{|c|l|c|c|c|

\hline

S. No. & Particulars & Quantity & Rate (Rs.) & Amount (Rs.)

\hline

1 & Ganga Soap (120 tablets = 10 dozen) & 10 dozen & 70 & 700

\hline

2 & Parachute Coconut Oil (7 boxes × 252 bottles = 1764 bottles = 147 dozen) & 147 dozen & 80 & 11,760

\hline

3 & Dalda Vanaspati Ghee (32 tins × 5 kg = 160 kg) & 160 kg & 35 & 5,600

\hline

4 & Lifebuoy Soap (12 boxes × 10 dozen = 120 dozen) & 120 dozen & 65 & 7,800

\hline

\multicolumn{4{|r|{Total & 25,860

\hline

\multicolumn{4{|r|{Less: Trade Discount 7.5% & 1,939.50

\hline

\multicolumn{4{|r|{Net Amount after Discount & 23,920.50

\hline

\end{tabular

% Additional Charges

Add: Expenses

(i) Packing Expenses = Rs. 12 per box (12 boxes) = Rs. 144 + Rs. 2 per tin (32 tins) = Rs. 64 → Total = Rs. 208

(ii) Cartage = Rs. 80

(iii) Railway Freight = Rs. 320

(iv) Insurance = Rs. 120

Total Expenses = 208 + 80 + 320 + 120 = Rs. 728

Net Amount Payable = Rs. 23,920.50 + Rs. 728 = Rs. 24,648.50

% Final Statement

Conclusion:

The invoice prepared for M/s Kanpuria Brothers shows the Net Amount Payable = Rs. 24,649 (approx.).

Quick Tip: In invoice preparation: First compute gross amount, then deduct trade discount, finally add packing, cartage, freight, and insurance to find the net payable.

Describe the main functions of the Reserve Bank of India.

View Solution

Step 1: Introduction.

The Reserve Bank of India (RBI) is the central bank of the country, established in 1935. It regulates the issue of currency, controls credit, manages foreign exchange, and supervises banks to ensure financial stability in the economy.

Step 2: Main Functions of RBI.

1. Issue of Currency: RBI has the sole authority to issue currency notes (except the one rupee note and coins, which are issued by the Government of India). This maintains uniformity and public confidence in the monetary system.

2. Monetary Control: RBI controls the supply of money and credit in the economy through monetary policies like Repo Rate, Reverse Repo Rate, and Cash Reserve Ratio (CRR).

3. Lender of Last Resort: In times of financial crisis, RBI provides emergency finance to commercial banks to ensure liquidity and stability.

4. Regulation of Banks: RBI supervises commercial banks, co-operative banks, and other financial institutions. It issues licenses, regulates reserves, and ensures sound banking practices.

5. Foreign Exchange Management: RBI manages foreign currency reserves and ensures stability of the Indian Rupee in the international market under FEMA (Foreign Exchange Management Act).

6. Control of Inflation and Deflation: By adjusting monetary tools, RBI ensures price stability and economic growth.

7. Promotion of Development: RBI supports agriculture, small industries, and rural development through credit policies and financial inclusion measures.

Step 3: Conclusion.

Thus, the Reserve Bank of India performs multiple functions such as issuing currency, controlling credit, regulating banks, managing foreign exchange, and promoting overall financial stability in the economy.

Quick Tip: RBI = “Bank of Banks” → Issues currency, controls money supply, and safeguards the economy.

Explain the mutual relationship between expenditure and savings and throw light on its social importance.

View Solution

Step 1: Introduction.

Income of an individual is generally divided into two parts: (i) Expenditure, and (ii) Savings. The balance between these two determines the financial security of a person and the flow of money in the economy.

Step 2: Mutual Relationship between Expenditure and Savings.

1. Expenditure and savings are inversely related – when expenditure increases, savings decrease, and vice versa.

2. If income is fixed, a person has to maintain a balance between current needs (expenditure) and future security (savings).

3. Higher savings reduce current consumption but provide funds for future investment.

4. Excessive expenditure may lead to very little or no savings, creating insecurity.

Step 3: Social Importance of Savings.

1. Capital Formation: Savings of individuals, when deposited in banks, help in capital formation which promotes industrial and economic growth.

2. Economic Stability: Adequate savings act as a buffer during economic crises and ensure stability in society.

3. Social Security: Savings provide financial protection to families during emergencies like illness, unemployment, or old age.

4. National Development: Collective savings of society are utilized for building infrastructure, industries, and welfare projects.

Step 4: Conclusion.

Thus, expenditure and savings are two sides of the same coin. A proper balance between them ensures individual financial security and contributes to social and economic development.

Quick Tip: “Spend wisely and save regularly” — Savings ensure future security while expenditure fulfills present needs.

Describe the Law of Diminishing Returns.

View Solution

Step 1: Introduction.

The Law of Diminishing Returns is an important principle in economics. It states that if more and more units of a variable factor (e.g., labour) are applied to a fixed factor (e.g., land), the additional output (marginal product) obtained from each successive unit of the variable factor will eventually decrease.

Step 2: Statement of the Law.

According to Marshall:

\textit{"An increase in the amount of one factor of production, while other factors remain fixed, after a certain point, results in a less than proportionate increase in output."

Step 3: Assumptions.

1. At least one factor of production is fixed (e.g., land).

2. The technique of production remains constant.

3. The units of variable factor are homogeneous.

4. It applies to the short run only.

Step 4: Explanation with Example.

Suppose labour is applied to a fixed piece of land:

- The first few workers increase output significantly.

- Later workers add smaller increases in output.

- Finally, additional workers may not increase output at all or may even reduce it due to overcrowding.

Step 5: Importance.

1. Explains why excessive use of a factor is unproductive.

2. Basis for the law of variable proportions in production.

3. Helps in determining the optimum combination of inputs.

4. Useful in agriculture and industries with fixed resources.

Step 6: Conclusion.

Thus, the law of diminishing returns shows that output cannot increase indefinitely by adding more units of a variable factor to a fixed factor, and efficiency decreases beyond a certain point.

Quick Tip: Law of Diminishing Returns = “Too many workers on fixed land → less output per worker.”

Comments