.png?h=35&w=35&mode=stretch)

CBSE Class 12 Accountancy Set 1 Question Paper PDF (Code: 67/2/1) is now available for download. CBSE conducted the Class 12 Accountancy examination on March 23, 2024, from 10:30 AM to 1:30 PM. The question paper consists of 34 questions carrying a total of 80 marks. Part A is compulsory for all candidates. Part B has two options. Candidates have to attempt only one of the given options. Option I : Analysis of Financial Statements and Option II : Computerised Accounting. Candidates can use the link below to download the CBSE Class 12 Accountancy Set 1 Question Paper with detailed solutions.

CBSE Class 12 Accountancy Question Paper 2024 (Set 1- 67/2/1) with Answer Key

| CBSE Class 12 2024 Accountancy Question Paper with Answer Key | Check Solution |

CBSE Class 12 2024 Accountancy Questions with Solutions

PART A

(Accounting for Partnership Firms and Companies)

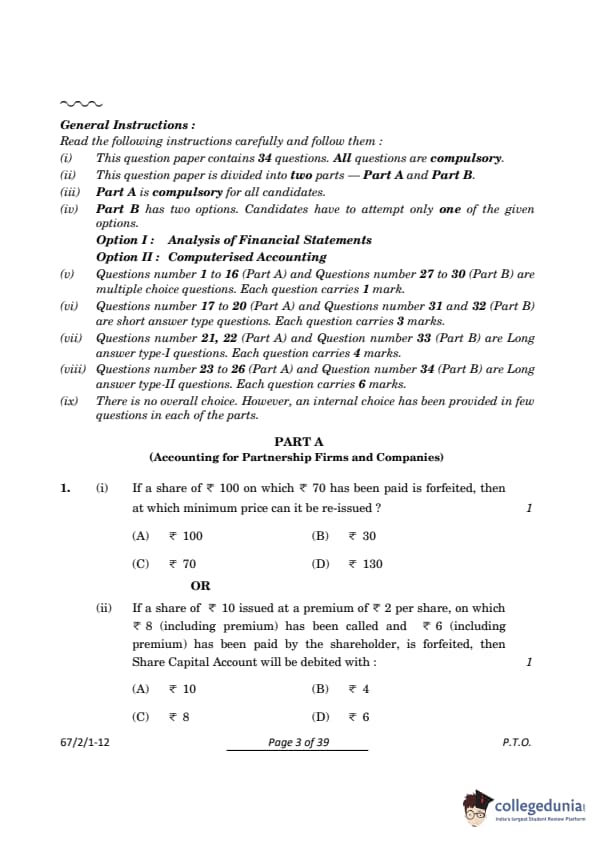

Question 1(a):

1(i).If a share of ₹100 on which ₹70 has been paid is forfeited, then at which minimum price can it be reissued?

View Solution

Solution:

For a forfeited share, the minimum re-issue price is the amount that was unpaid at the time of forfeiture. The unpaid amount here is:

₹100 - ₹70 = ₹30.

Hence, the minimum price at which the share can be reissued is ₹30.

Question 1(b):

1(ii). If a share of ₹10 issued at a premium of ₹2 per share, on which ₹8 (including premium) has been called and ₹6 (including premium) has been paid by the shareholder, is forfeited, then Share Capital Account will be debited with:

View Solution

Solution:

To calculate the amount debited to the Share Capital Account upon forfeiture of shares:

Step 1: Determine the nominal value of the share.

The nominal value is ₹10.

Step 2: Calculate the called-up amount excluding the premium.

The total called-up amount is ₹8, including a premium of ₹2. Exclude the premium to find the called-up capital:

Called-up Capital = ₹8 - ₹2 = ₹6.

Step 3: Debit the Share Capital Account.

Since ₹6 has been called up and ₹6 has been paid, the Share Capital Account is debited with ₹6.

Hence, the correct answer is (D) ₹6.

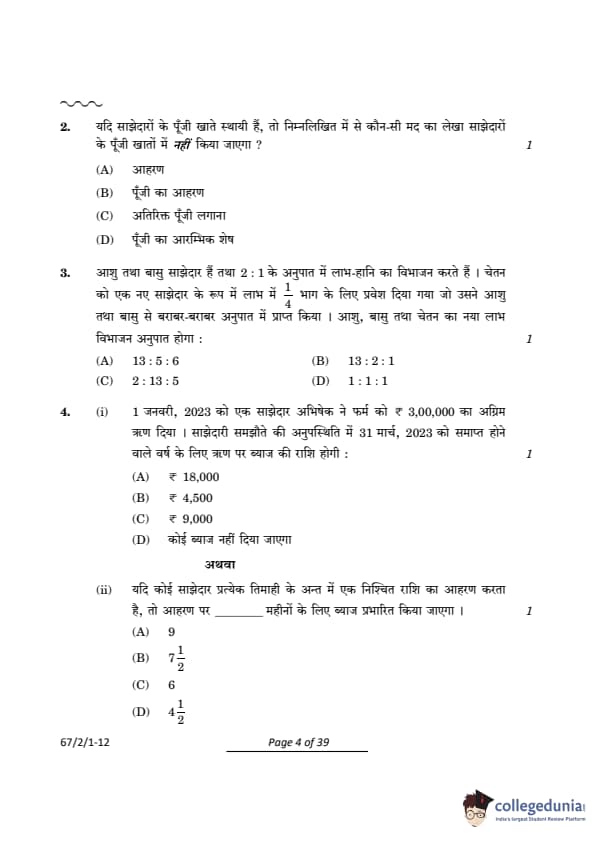

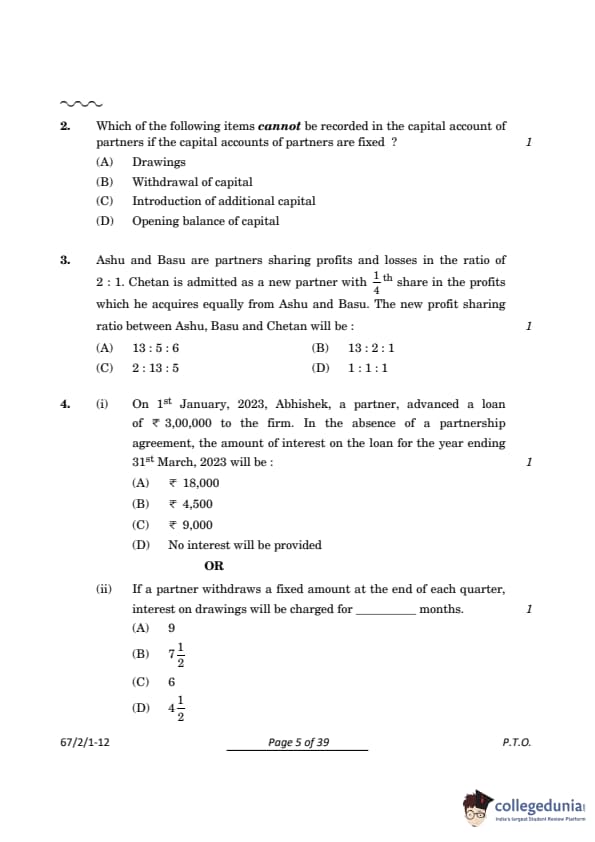

Question 2:

2. Which of the following items cannot be recorded in the capital account of partners if the capital accounts of partners are fixed?

View Solution

Solution:

In a partnership firm, when the capital accounts are fixed, only permanent changes like additional capital, withdrawal of capital, or opening balances are recorded in the capital account. Temporary adjustments, such as drawings, interest on capital, or share of profit/loss, are recorded in the current account. Therefore, drawings cannot be recorded in the fixed capital account.

Question 3:

3. Ashu and Basu are partners sharing profits and losses in the ratio of 2:1. Chetan is admitted as a new partner with 1⁄4 share in the profits, which he acquires equally from Ashu and Basu. The new profit-sharing ratio between Ashu, Basu, and Chetan will be:

View Solution

Solution:

Step 1: Determine the share sacrificed by Ashu and Basu.

Chetan's share is 1⁄4 , which is acquired equally from Ashu and Basu. Therefore:

Ashu's Sacrifice = 1⁄4 x 1⁄2 = 1⁄8 , Basu's Sacrifice = 1⁄4 x 1⁄2 = 1⁄8 .

Step 2: Calculate the new shares of Ashu and Basu.

Ashu's New Share = 2⁄3 - 1⁄8 = 16⁄24 - 3⁄24 = 13⁄24.

Basu's New Share = 1⁄3 - 1⁄8 = 8⁄24 - 3⁄24 = 5⁄24.

Chetan's Share = 1⁄4 = 6⁄24.

Step 3: Simplify the new ratio.

The new profit-sharing ratio is:

13:5:6.

Hence, the correct answer is (1).

Question 4(a):

4(i). On 1st January, 2023, Abhishek, a partner, advanced a loan of ₹3,00,000 to the firm. In the absence of a partnership agreement, the amount of interest on the loan for the year ending 31st March, 2023 will be:

View Solution

Solution:

In the absence of a partnership agreement, interest on loans provided by a partner is charged at 6% per annum. The loan was advanced on 1st January, 2023, and the year ends on 31st March, 2023, making the duration 3 months.

Interest = ₹3,00,000 x 6⁄100 x 3⁄12 = ₹4,500.

Hence, the correct answer is (2).

Question 4(b):

4(ii). If a partner withdraws a fixed amount at the end of each quarter, interest on drawings will be charged for ........ months.

View Solution

Solution:

If a partner withdraws a fixed amount at the end of each quarter, the average period for which interest is charged is calculated as: Average Period = Time from First Withdrawal + Time from Last Withdrawal⁄2 .

Withdrawals occur at the end of: - 1st quarter: Remaining time is 9 months. - 2nd quarter: Remaining time is 6 months. - 3rd quarter: Remaining time is 3 months. - 4th quarter: Remaining time is 0 months.

For average period: Average Period = 9 + 0⁄2 = 4.5 months.

Hence, the correct answer is (4).

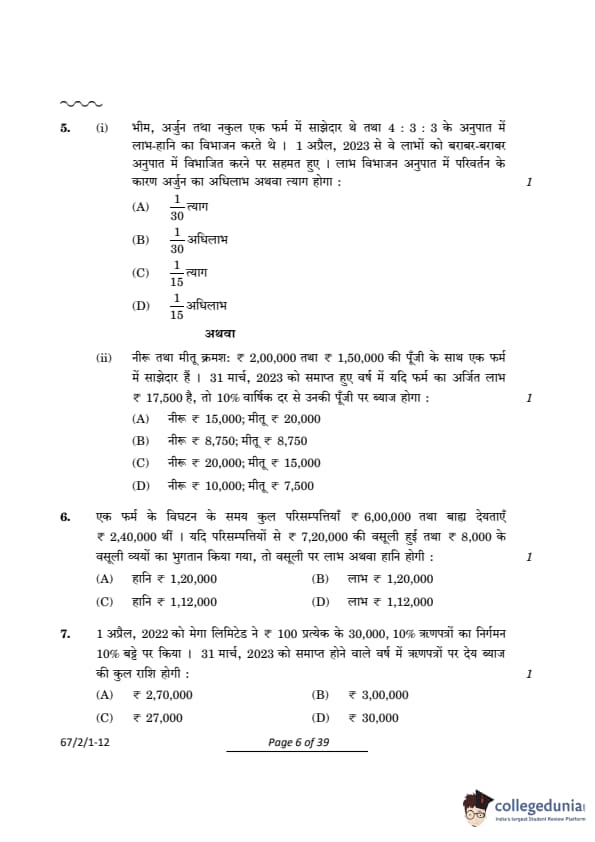

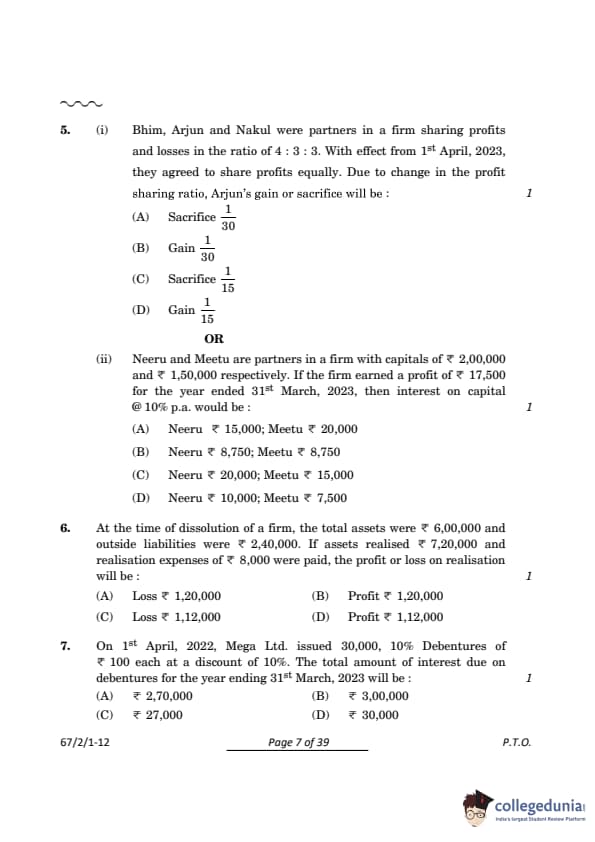

Question 5(i):

5(i). Bhim, Arjun, and Nakul were partners in a firm sharing profits and losses in the ratio of 4 : 3 : 3. With effect from 1st April 2023, they agreed to share profits equally. Due to the change in the profit-sharing ratio, Arjun's gain or sacrifice will be:

View Solution

Solution:

The initial profit-sharing ratio is 4 : 3 : 3, and the new profit-sharing ratio is 1:1:1 (equal sharing).

For Arjun:

Old Share = 3⁄10 , New Share = 1⁄3.

Calculate Arjun's sacrifice or gain:

Sacrifice or Gain = New Share - Old Share.

Substitute the values:

Sacrifice or Gain = 1⁄3 - 3⁄10.

Take the LCM of denominators 10 and 3, which is 30:

1⁄3 = 10⁄30 , 3⁄10 = 9⁄30.

Sacrifice or Gain = 10⁄30 - 9⁄30 = 1⁄30.

Since the result is positive, it represents a gain.

Hence, the correct answer is (2) Gain 1⁄30.

Question 5(ii):

5(ii). Neeru and Meetu are partners in a firm with capitals of ₹2,00,000 and ₹1,50,000 respectively. If the firm earned a profit of ₹17,500 for the year ended 31st March 2023, then interest on capital @ 10% p.a. would be:

View Solution

Solution:

The interest on capital (IOC) is calculated at the rate of 10% p.a. on the capital contributions.

IOC (Neeru) = 10⁄100 x 2,00,000 = ₹20,000 IOC (Meetu) = 10⁄100 x 1,50,000 = ₹15,000

The total interest exceeds the available profit of ₹17,500. Therefore, the interest will be adjusted in the ratio of their capitals, which is 2,00,000 : 1,50,000 = 4 : 3.

Adjusted IOC (Neeru) = 4⁄7 x 17,500 = ₹10,000 Adjusted IOC (Meetu) = 3⁄7 x 17,500 = ₹7,500

Hence, the correct answer is (4) Neeru ₹10,000; Meetu ₹7,500

Question 6:

6. At the time of dissolution of a firm, the total assets were ₹6,00,000 and outside liabilities were ₹2,40,000. If assets realised ₹7,20,000 and realisation expenses of ₹8,000 were paid, the profit or loss on realisation will be:

View Solution

Solution:

To calculate the profit or loss on realisation, use the formula: Profit or Loss on Realisation = Total Realisation - (Outside Liabilities + Realisation Expenses).

Substitute the values: Total Realisation = ₹7,20,000, Outside Liabilities = ₹2,40,000, Realisation Expenses = ₹8,000

Profit or Loss = ₹7,20,000 - (₹2,40,000 + ₹8,000) = ₹7,20,000 - ₹2,48,000 = ₹4,72,000

The profit on realisation is ₹4,72,000. However, after accounting for initial total assets ₹6,00,000, the net profit is: ₹7,20,000 - ₹6,00,000 - ₹8,000 = ₹1,12,000.

Hence, the correct answer is (4) Profit ₹1,12,000.

Question 7:

7. On 1st April, 2022, Mega Ltd. issued 30,000, 10% Debentures of ₹100 each at a discount of 10%. The total amount of interest due on debentures for the year ending 31st March, 2023 will be:

View Solution

Solution:

Step 1: Calculate the total debenture amount.

The face value of each debenture is ₹100, and 30,000 debentures were issued. Therefore: Total face value = 30,000 x ₹100 = ₹30,00,000.

Step 2: Calculate the annual interest.

The interest rate is 10%, so the total interest for one year is: Total interest = 10% x ₹30,00,000 = ₹3,00,000.

Hence, the correct answer is (2) ₹3,00,000

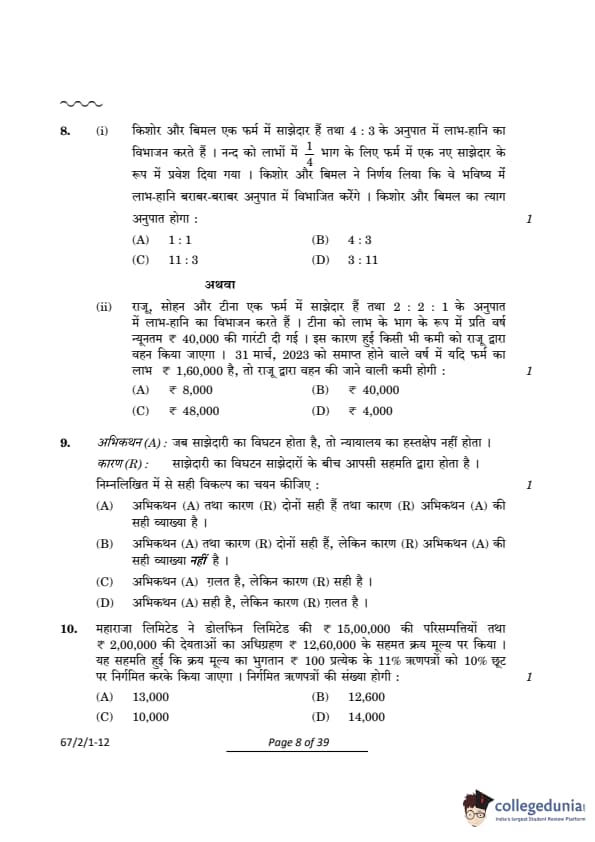

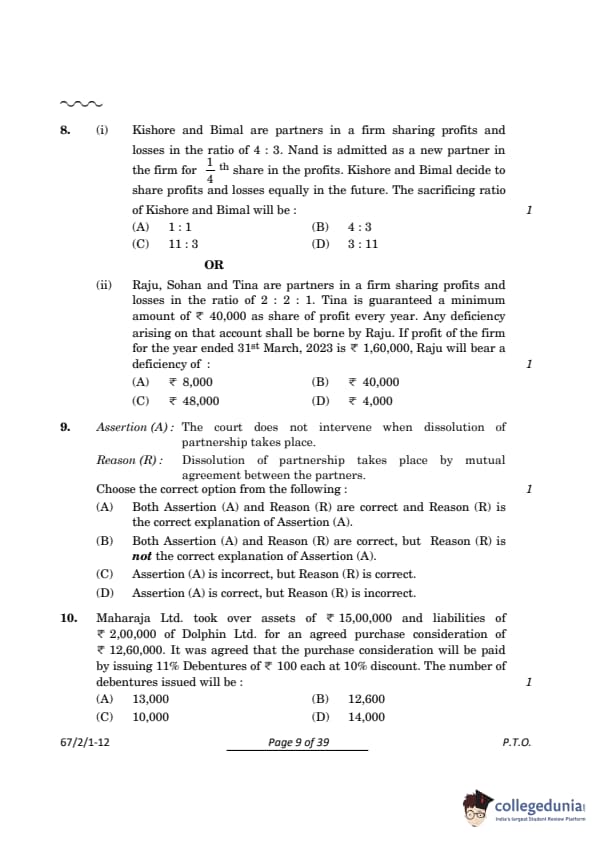

Question 8(i):

8(i). Kishore and Bimal are partners in a firm sharing profits and losses in the ratio of 4:3. Nand is admitted as a new partner in the firm for 1⁄4 share in the profits. Kishore and Bimal decide to share profits and losses equally in the future. The sacrificing ratio of Kishore and Bimal will be:

View Solution

Solution:

The old profit-sharing ratio of Kishore and Bimal is 4:3, and Nand takes 1⁄4 of the profits. The remaining 3⁄4 will be shared equally between Kishore and Bimal.

Step 1: Calculate old shares of Kishore and Bimal.

Kishore's old share = 4⁄7, Bimal's old share = 3⁄7.

Step 2: Calculate new shares of Kishore and Bimal.

The remaining 3⁄4 is shared equally: Kishore's new share = 3⁄4 x 1⁄2 = 3⁄8, Bimal's new share = 3⁄8.

Step 3: Calculate sacrifice.

Kishore's sacrifice = 4⁄7 - 3⁄8 = 32⁄56 - 21⁄56 = 11⁄56, Bimal's sacrifice = 3⁄7 - 3⁄8 = 24⁄56 - 21⁄56 = 3⁄56.

Step 4: Determine the sacrificing ratio.

The sacrificing ratio is 11:3.

Hence, the correct answer is (3).

Question 8(ii):

8(ii). Raju, Sohan, and Tina are partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. Tina is guaranteed a minimum amount of ₹40,000 as a share of profit every year. Any deficiency arising on that account shall be borne by Raju. If the profit of the firm for the year ended 31st March, 2023 is ₹1,60,000, Raju will bear a deficiency of:

View Solution

Solution:

Step 1: Calculate Tina's profit share based on the profit-sharing ratio.

The total profit is ₹1,60,000, and the profit-sharing ratio is 2:2:1. Tina’s share is: Tina's share = 1⁄5 x 1,60,000 = ₹32,000.

Step 2: Determine the deficiency.

Tina is guaranteed ₹40,000. Since her calculated share is ₹32,000, the deficiency is: Deficiency = ₹40,000 - ₹32,000 = ₹8,000.

Step 3: Allocate the deficiency.

The deficiency of ₹8,000 will be borne by Raju as per the agreement.

Hence, the correct answer is (1) ₹8,000.

Question 9:

9. Assertion (A): The court does not intervene when dissolution of partnership takes place.

Reason (R): Dissolution of partnership takes place by mutual agreement between the partners.

Choose the correct option from the following:

View Solution

Solution:

Dissolution of a partnership can take place by mutual agreement among partners, and in such cases, the court does not intervene. Assertion (A) correctly states this, and Reason (R) explains it accurately. Thus, both Assertion (A) and Reason (R) are correct, and Reason (R) provides the correct explanation.

Hence, the correct answer is (1).

Question 10:

10. Maharaja Ltd. took over assets of ₹15,00,000 and liabilities of ₹2,00,000 of Dolphin Ltd. for an agreed purchase consideration of ₹12,60,000. It was agreed that the purchase consideration will be paid by issuing 11% Debentures of ₹100 each at 10% discount. The number of debentures issued will be:

View Solution

Solution:

To calculate the number of debentures issued, use the formula: Number of Debentures = Purchase Consideration⁄Issue Price per Debenture .

Step 1: Calculate the Issue Price per Debenture.

The face value of each debenture is ₹100, and the discount is 10%. Hence, the issue price is: Issue Price = ₹100 - ₹10 = ₹90.

Step 2: Calculate the Number of Debentures.

Number of Debentures = 12,60,000⁄90 = 14,000.

Hence, the correct answer is (4) 14,000.

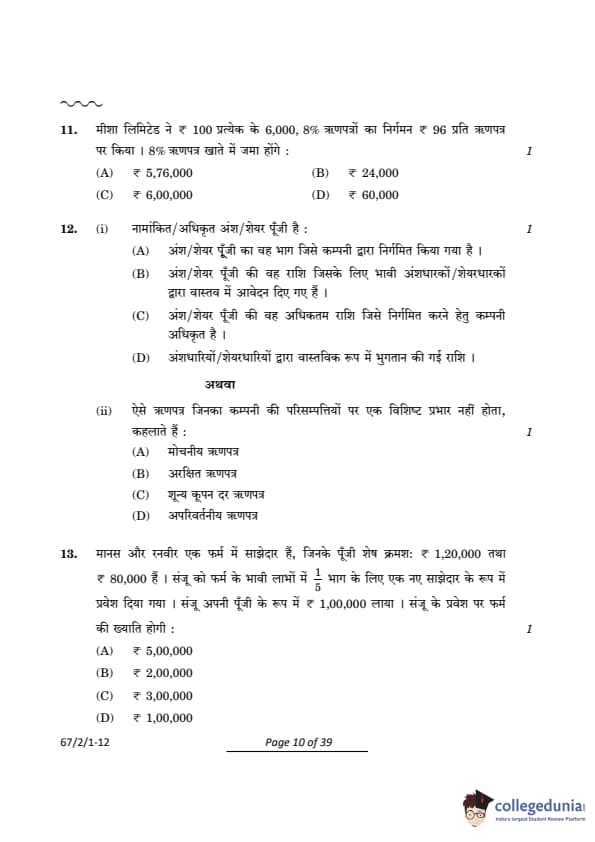

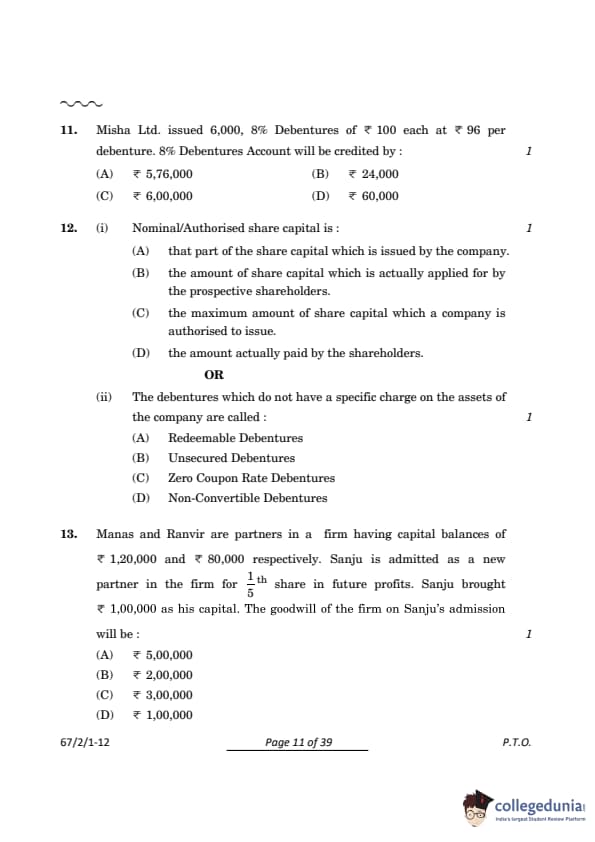

Question 11:

11. Misha Ltd. issued 6,000, 8% Debentures of ₹100 each at ₹96 per debenture. The 8% Debentures Account will be credited by:

View Solution

Solution:

The debentures account is always credited with the face value of the debentures, regardless of whether they are issued at a premium or a discount.

Calculation:

Face Value of Debentures = 6,000 x ₹100 = ₹6,00,000.

The discount amount of ₹4 per debenture (₹96 issue price) is recorded separately as a loss under “Discount on Issue of Debentures.”

Hence, the correct answer is (3) ₹6,00,000.

Question 12(i):

12(i). Nominal/Authorised share capital is:

View Solution

Solution:

Nominal or authorised share capital refers to the maximum value of shares that a company is authorised to issue as per its Memorandum of Association. It is the upper limit of share capital that a company can legally raise.

Hence, the correct answer is (3).

Question 12(ii):

12(ii). The debentures which do not have a specific charge on the assets of the company are called:

View Solution

Solution:

Debentures are classified based on whether they are secured against company assets. Unsecured Debentures, also known as naked debentures, do not have any specific charge on the company's assets. These debentures rely on the general creditworthiness of the issuer for repayment.

Hence, the correct answer is (2).

Question 13:

13. Manas and Ranvir are partners in a firm having capital balances of ₹1,20,000 and ₹80,000 respectively. Sanju is admitted as a new partner in the firm for 1⁄5 share in future profits. Sanju brought ₹1,00,000 as his capital. The goodwill of the firm on Sanju’s admission will be:

View Solution

Solution:

Step 1: Calculate the total capital of the firm based on Sanju’s share.

Sanju's share in the profits is 1⁄5. This means the total capital of the firm can be calculated as: Total Capital of the Firm = Sanju's Capital⁄Sanju's Share = 1,00,000⁄1⁄5 = 5,00,000.

Step 2: Calculate the combined capital of existing partners.

The combined capital of Manas and Ranvir is: Combined Capital = 1,20,000 + 80,000 = 2,00,000.

Step 3: Calculate the goodwill of the firm.

Goodwill of the firm is the difference between the total capital of the firm and the combined capital of the existing partners: Goodwill = Total Capital of the Firm – Combined Capital of Existing Partners. Goodwill = 5,00,000 - 2,00,000 = 3,00,000.

Final Answer: The goodwill of the firm on Sanju's admission is ₹2,00,000

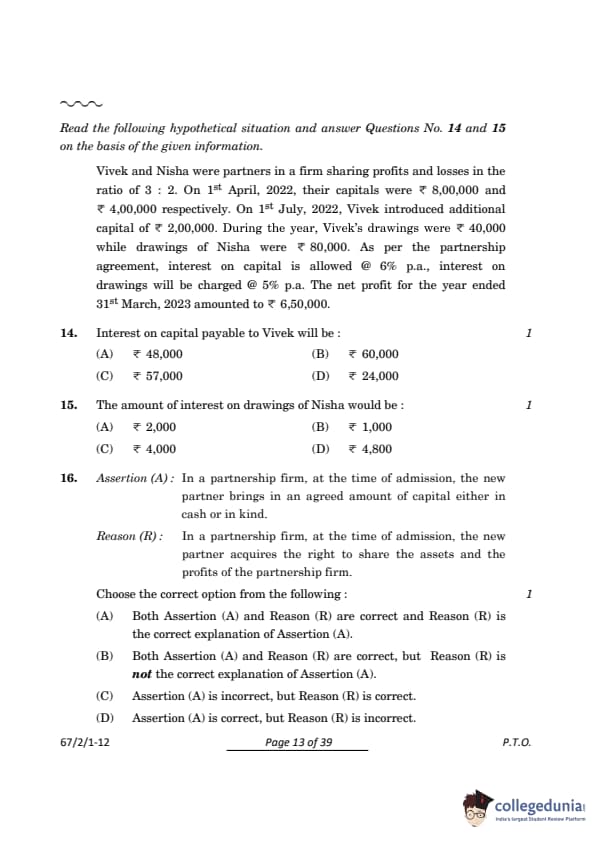

Question 14:

Read the following hypothetical situation and answer Questions No. 14 and 15 on the basis of the given information.

Vivek and Nisha were partners in a firm sharing profits and losses in the ratio of 3 : 2. On 1st April, 2022, their capitals were ₹ 8,00,000 and ₹ 4,00,000 respectively. On 1st July, 2022, Vivek introduced additional capital of ₹ 2,00,000. During the year, Vivek’s drawings were ₹ 40,000 while drawings of Nisha were ₹ 80,000. As per the partnership agreement, interest on capital is allowed @ 6% p.a., interest on drawings will be charged @ 5% p.a. The net profit for the year ended 31st March, 2023 amounted to ₹ 6,50,000.

Question 14:

The amount of interest on drawings of Nisha would be:

View Solution

Solution:

Interest on drawings is calculated as: Interest on Drawings = Amount Withdrawn × Rate of Interest × Average Period. Assuming regular withdrawals, the average period is 6 months: Interest on Drawings = ₹80,000 × 5⁄100 × 6⁄12 = ₹2,000.

Question 15:

Interest on capital payable to Vivek will be:

View Solution

Solution:

Interest on capital is calculated as: Interest on Capital = Capital Amount × Rate of Interest. Assuming Vivek's capital is ₹3,80,000, and the rate of interest is 15% per annum: Interest on Capital = ₹3,80,000 × 15% = ₹57,000. Thus, the correct answer is (3).

Question 16:

Ashu and Basu are partners sharing profits and losses in the ratio of 2:1. Chetan is admitted as a new partner with 1⁄4 share in the profits, which he acquires equally from Ashu and Basu. The new profit-sharing ratio between Ashu, Basu, and Chetan will be:

View Solution

Solution:

1. Chetan's share is 1⁄4, leaving 3⁄4 to be shared between Ashu and Basu. 2. Ashu and Basu sacrifice equally: Ashu's new share = 2⁄3 x 3⁄4 + 1⁄8 = 13⁄24 Basu's new share = 1⁄3 x 3⁄4 + 1⁄8 = 5⁄24 3. Chetan's share is 1⁄4 = 6⁄24. Thus, the new ratio is 13:5:6. Hence, the correct answer is (1).

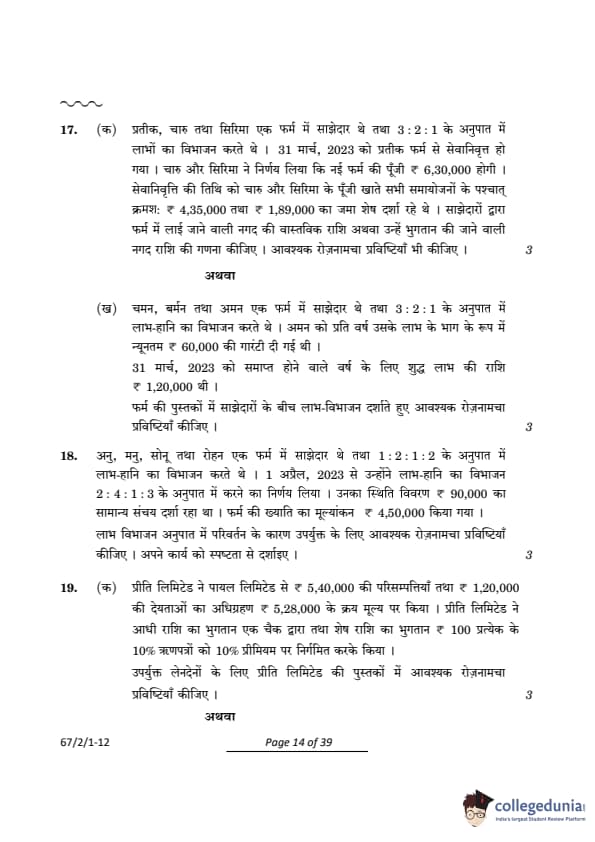

Question 17(a):

17(a). Prateek, Charu, and Sirima were partners in a firm sharing profits in the ratio of 3:2:1. Prateek retired from the firm on 31st March, 2023. Charu and Sirima decided that the capital of the new firm will be ₹6,30,000. The capital accounts of Charu and Sirima after all adjustments on the date of retirement showed a credit balance of ₹4,35,000 and ₹1,89,000 respectively. Calculate the amount of actual cash to be brought into the firm or to be paid to the partners. Also pass necessary journal entries.

View Solution

Solution:

Step 1: Calculate the total capital of Charu and Sirima in the new ratio. The new profit-sharing ratio between Charu and Sirima is 2:1. The total capital of the firm is 6,30,000.

Charu's Capital = 2⁄3 × 6,30,000 = 4,20,000 Sirima's Capital = 1⁄3 × 6,30,000 = 2,10,000

Step 2: Adjust the current balances of Charu and Sirima.

• Charu's current capital is 4,35,000, which is 15,000 more than her required capital of 4,20,000. Therefore, Charu will withdraw 15,000.

• Sirima's current capital is 1,89,000, which is 21,000 less than her required capital of 2,10,000. Therefore, Sirima will bring in 21,000.

Step 3: Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| 31st March, 2023 | Charu's Capital A/c Dr. | 15,000 | -- |

| To Bank A/c | -- | 15,000 | |

| (Being the excess capital withdrawn by Charu) | |||

| 31st March, 2023 | Bank A/c Dr. | 21,000 | -- |

| To Sirima's Capital A/c | -- | 21,000 | |

| (Being the deficit capital brought in by Sirima) | |||

• Charu will withdraw 15,000.

• Sirima will bring 21,000 into the firm.

Question 17(b):

17(b) Chaman, Burman, and Aman were partners in a firm sharing profits and losses in the ratio of 3:2:1. Aman was guaranteed a minimum amount of ₹60,000 as his share of profit every year. The net profit for the year ended 31st March, 2023 amounted to ₹1,20,000. Pass necessary journal entries in the books of the firm showing the distribution of profit amongst the partners.

View Solution

Solution:

Step 1: Distribution of Net Profit in the Profit-Sharing Ratio. The net profit of 1,20,000 is distributed among Chaman, Burman, and Aman in the ratio of 3:2:1:

Chaman's Share = 1,20,000 × 3⁄6 = 60,000

Burman's Share = 1,20,000 × 2⁄6 = 40,000 Aman's Share = 1,20,000 × 1⁄6 = 20,000

Step 2: Adjustment for Aman's Guaranteed Profit. Aman is guaranteed 60,000, but his calculated share is only 20,000. Hence, an adjustment of 40,000 needs to be made from the profits of Chaman and Burman in their profit-sharing ratio (3:2):

Adjustment from Chaman = 40,000 × 3⁄5 = 24,000

Adjustment from Burman = 40,000 × 2⁄5 = 16,000

Step 3: Final Distribution of Profit. After adjustments:

Chaman's Final Share = 60,000 - 24,000 = 36,000

Burman's Final Share = 40,000 – 16,000 = 24,000

Aman's Final Share = 20,000 + 40,000 = 60,000

Step 4: Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| 31st March, 2023 | Profit and Loss A/c Dr. | 1,20,000 | -- |

| To Chaman's Capital A/c | -- | 36,000 | |

| To Burman's Capital A/c | -- | 24,000 | |

| To Aman's Capital A/c | -- | 60,000 | |

| (Being the distribution of net profit adjusted for guaranteed profit to Aman) | |||

| 31st March, 2023 | Chaman's Capital A/c Dr. | 24,000 | -- |

| Burman's Capital A/c Dr. | 16,000 | -- | |

| To Aman's Capital A/c | -- | 40,000 | |

| (Being the adjustment of guaranteed profit to Aman) | |||

Question 18:

18. Madhu, Raj, Atul, and Prachi were partners in a firm sharing profit and losses in the ratio of 3:2:4:1. With effect from 1st April, 2023, they decided to share profits and losses equally. Their Balance Sheet showed a General Reserve of 1,00,000. The goodwill of the firm was valued at 20,00,000. Pass necessary journal entries for the above on account of change in the profit-sharing ratio. Show your working clearly.

View Solution

Solution:

Step 1: Calculate the old and new profit-sharing ratios.

Old Ratio = 3:2:4:1

New Ratio = 1 : 1 : 1 :1

Step 2: Calculate the sacrifice or gain for each partner.

Sacrificing Ratio = Old Share - New Share

Madhu's Share: 3⁄10 - 1⁄4 = 12⁄40 - 10⁄40 = 2⁄40 (Sacrifice)

Raj's Share: 2⁄10 - 1⁄4 = 8⁄40 - 10⁄40 = -2⁄40 (Gain)

Atul's Share: 4⁄10 - 1⁄4 = 16⁄40 - 10⁄40 = 6⁄40 (Sacrifice)

Prachi's Share: 1⁄10 - 1⁄4 = 4⁄40 - 10⁄40 = -6⁄40 (Gain)

Step 3: Distribute the goodwill. The goodwill of 20,00,000 is distributed based on the sacrificing ratio (Madhu:Atul = 2:6):

Madhu's Share of Goodwill = 20,00,000 × 2⁄8 = 5,00,000

Atul's Share of Goodwill = 20,00,000 × 6⁄8 = 15,00,000

Step 4: Distribute the General Reserve. The General Reserve of 1,00,000 is distributed in the old profit-sharing ratio (3:2:4:1):

Madhu's Share = 1,00,000 × 3⁄10 = 30,000

Raj's Share = 1,00,000 × 2⁄10 = 20,000

Atul's Share = 1,00,000 × 4⁄10 = 40,000

Prachi's Share = 1,00,000 × 1⁄10 = 10,000

Step 5: Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| 1st April, 2023 | Raj's Capital A/c Dr. | 5,00,000 | -- |

| Prachi's Capital A/c Dr. | 15,00,000 | -- | |

| To Madhu's Capital A/c | -- | 5,00,000 | |

| To Atul's Capital A/c | -- | 15,00,000 | |

| (Being the adjustment of goodwill in the sacrificing ratio) | |||

| 1st April, 2023 | General Reserve A/c Dr. | 1,00,000 | -- |

| To Madhu's Capital A/c | -- | 30,000 | |

| To Raj's Capital A/c | -- | 20,000 | |

| To Atul's Capital A/c | -- | 40,000 | |

| To Prachi's Capital A/c | -- | 10,000 | |

| (Being the General Reserve distributed in the old ratio) | |||

Question 19(a):

19(a). Priti Ltd. purchased assets worth ₹5,40,000 and took over liabilities of ₹1,20,000 of Payal Ltd. for a purchase consideration of ₹5,28,000. Priti Ltd. paid half the amount by cheque, and the balance was settled by issuing 10% Debentures of ₹100 each at a premium of 10%.

View Solution

Solution:

Step 1: Analyze the transaction.

• Assets taken over: 5,40,000

• Liabilities taken over: 1,20,000

• Purchase consideration: 5,28,000

• Payment:

Half of 5,28,000 = 2,64,000 paid by cheque.

Remaining 2,64,000 settled by issuing 10% Debentures.

• Debentures issued at a 10% premium:

Face Value of Debentures = 2,64,000⁄1.10 = 2,40,000

Premium Amount = 2,40,000 × 10% = 24,000

Step 2: Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| Sundry Assets A/c Dr. | 5,40,000 | - | |

| To Sundry Liabilities A/c | - | 1,20,000 | |

| To Payal Ltd. A/c | - | 5,28,000 | |

| (Being the assets and liabilities of Payal Ltd. taken over) | |||

| - | Payal Ltd. A/c Dr. | 5,28,000 | - |

| To Bank A/c | - | 2,64,000 | |

| To 10% Debentures A/c | - | 2,40,000 | |

| To Securities Premium A/c | - | 24,000 | |

| (Being the purchase consideration paid, half by cheque and the remaining settled by issuing 10% Debentures at a 10% premium) | |||

• Cheque Payment:

By Cheque = Purchase Consideration⁄2 = 2,64,000

• Debenture Value and Premium:

Debentures Face Value = Remaining Amount⁄1.10 = 2,40,000

Premium Amount = 2,40,000 × 10% = 24,000

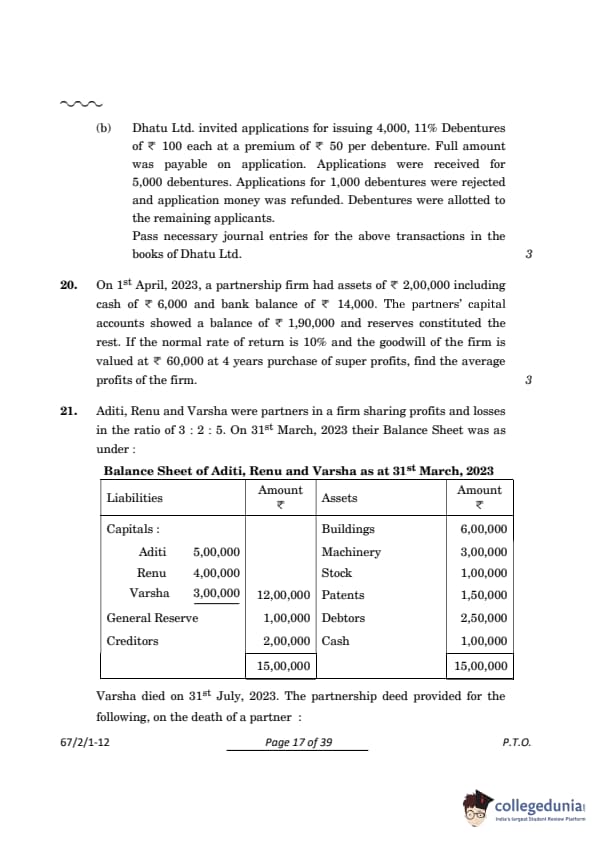

Question 19(b):

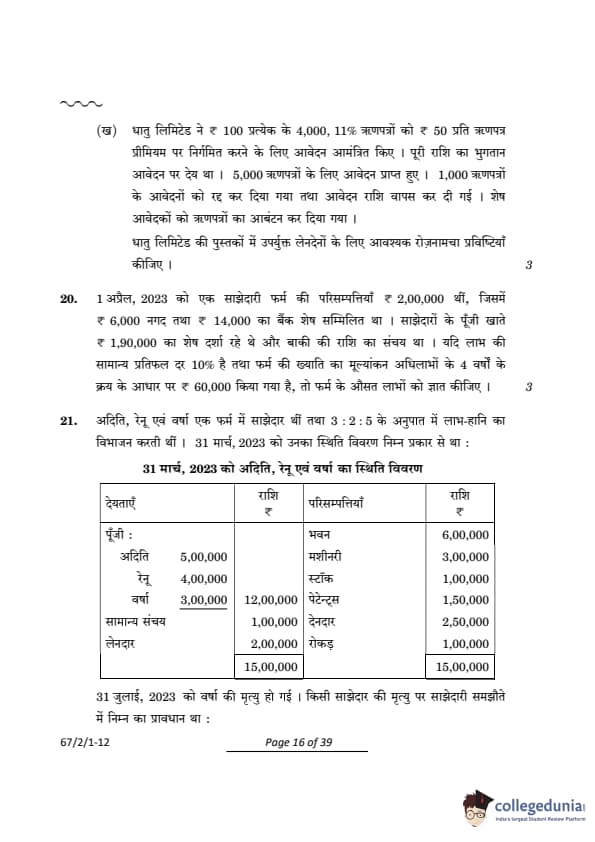

19(b) Dhatu Ltd. invited applications for issuing 4,000, 11% Debentures of ₹100 each at a premium of ₹50 per debenture. Full amount was payable on application.

View Solution

Solution:

Step 1: Analyze the transaction.

• Total debentures issued: 4,000 at 100 each + 50 premium 150 per debenture.

• Applications received: 5,000 debentures.

• Rejected applications: 1,000 debentures (150 per debenture refunded).

• Applications accepted: 4,000 debentures.

• Total application money received: 5,000 debentures × 150 = 7,50,000.

Step 2: Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| - | Bank A/c Dr. | 7,50,000 | -- |

| To Debentures Application A/c | -- | 7,50,000 | |

| (Being the application money received for 5,000 debentures) | |||

| - | Debentures Application A/c Dr. | 7,50,000 | -- |

| To Bank A/c (Refund for 1,000 debentures) | -- | 1,50,000 | |

| To 11% Debentures A/c | -- | 4,00,000 | |

| To Securities Premium A/c | -- | 2,00,000 | |

| (Being the application money adjusted for 4,000 debentures and refunded for 1,000 debentures) | |||

• Application money received for 5,000 debentures:

150 × 5,000 debentures = 7,50,000.

• Application money refunded for 1,000 debentures:

150 × 1,000 debentures = 1,50,000.

• Application money adjusted for 4,000 debentures:

150 × 4,000 debentures = 6,00,000.

100 per debenture credited to the 11% Debentures Account: 4,00,000. - 50 per debenture credited to the Securities Premium Account: 2,00,000.

Question 20:

20. On 1st April, 2023, the books of the firm of Kashish and Sagar showed assets of ₹9,00,000 including cash of ₹32,000 and bank balance of ₹1,68,000. The partners’ capital accounts showed a balance of ₹6,00,000 and reserves constituted the rest. If the normal rate of return is 8% and the goodwill of the firm is valued at ₹4,00,000 at 5 years purchase of super profits, find the average profits of the firm.

View Solution

Solution:

Goodwill = No. of years’ purchase X Super Profits

₹60,000 = 4 X Super Profits

Super Profits = ₹15,000

Capital Employed= Total Assets- Outside Liabilities = ₹2,00,000- Nil= ₹2,00,000

Normal Profit =10% of ₹2,00,000 = ₹20,000 Super Profit = Average Profit- Normal Profit

₹15,000 = Average profit- ₹20,000

Average Profit= ₹35,000

Question 21:

21. Aditi, Renu, and Varsha were partners in a firm sharing profits and losses in the ratio of 3:2:5. On 31st March, 2023, their Balance Sheet was as under:

Balance Sheet of Ravi, Tanu and Sara as at 31st March, 2023

| Liabilities | Amount (₹) | Assets | Amount (₹) |

|---|---|---|---|

| Capital: | Land and Buildings | 6,36,000 | |

| Ravi | 2,45,000 | Plant and Machinery | 3,10,000 |

| Tanu | 1,75,000 | Debtors | 2,00,000 |

| Sara | 1,00,000 | Less: Provision for doubtful debts | (10,000) |

| General Reserve | 40,000 | Stock | 70,000 |

| Ravi’s Loan A/c | 2,39,500 | Goodwill | 1,60,000 |

| Creditors | 1,87,000 | Cash | 61,000 |

| Profit and Loss A/c | 45,000 | ||

| Total | 9,86,500 | Total | 9,86,500 |

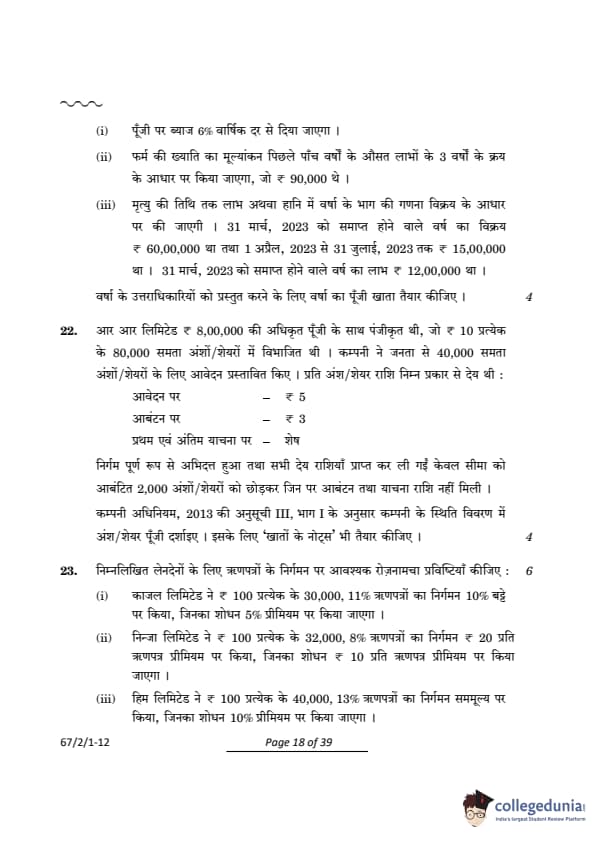

Varsha passed away on 31st July, 2023. The partnership deed required the following adjustments: 1. Interest on capital to be provided @6% p.a. 2. Goodwill of the firm to be valued at 3 years' purchase of the average profits of the previous five years, which were ₹90,000. 3. Varsha’s share of profit until the date of death to be calculated based on sales. Sales for the year ended 31st March, 2023, were ₹60,00,000, and sales from 1st April, 2023, to 31st July, 2023, amounted to ₹15,00,000. The profit for the year ended 31st March, 2023, was ₹12,00,000.

View Solution

Solution:

![]()

![]()

![]()

Question 22:

22. RR Ltd. was registered with an authorised capital of ₹8,00,000 divided into 80,000 equity shares of ₹10 each. The company offered to the public for subscription 40,000 equity shares. The amount per share was payable as follows:

• On Application: ₹5

• On Allotment: ₹3

• On First and Final Call: Balance

The issue was fully subscribed, and all amounts due were received except the allotment and call money on 2,000 shares allotted to Seema. Present the Share Capital in the Balance Sheet of the company as per Schedule III, Part I of the Companies Act, 2013. Also prepare ‘Notes to Accounts' for the same.

View Solution

Solution:

Balance Sheet of RR Ltd. as on ... (extract) Notes to Accounts:

![]()

![]()

![]()

Question 23:

Pass necessary journal entries for issue of debentures for the following transactions:

(i) Kajal Ltd. issued 30,000, 11% Debentures of Rs. 100 each at a discount of 10%, redeemable at a premium of 5%.

(ii) Ninja Ltd. issued 32,000, 8% Debentures of Rs. 100 each at a premium Rs. 20 per debenture, redeemable at a premium of Rs. 10 per debenture.

(iii) Him Ltd. issued 40,000, 13% Debentures of Rs. 100 each at par, redeemable at a premium of 10%.

View Solution

Solution:

(i) Books of Kajal Ltd. - Journal

| Date | Particulars | L.F. | Dr. Amount (₹) | Cr. Amount (₹) |

|---|---|---|---|---|

| Bank A/c Dr. | 27,00,000 | |||

| To Debenture Application and Allotment A/c | 27,00,000 | |||

| (Receipt of application money on 30,000, 11% Debentures of ₹100 each at a discount of 10%) | ||||

| Debenture Application and Allotment A/c Dr. | 27,00,000 | |||

| Loss on Issue of Debentures A/c Dr. | 4,50,000 | |||

| To 11% Debentures A/c | 30,00,000 | |||

| To Premium on Redemption of Debentures A/c | 1,50,000 | |||

| (Transfer of Debenture application money and provision for premium on redemption of Debentures made) | ||||

(Alternative entry combining the debit to the loss account is also acceptable.)

(ii) Books of Ninja Ltd. - Journal

| Date | Particulars | Dr. Amount (Rs.) | Cr. Amount (Rs.) |

|---|---|---|---|

| Bank A/c Dr. | 38,40,000 | ||

| To Debenture Application and Allotment A/c | 38,40,000 | ||

| (Receipt of application money on 32,000, 8% Debentures of Rs. 100 each at a premium) | |||

| Debenture Application and Allotment A/c Dr. | 38,40,000 | ||

| To 8% Debentures A/c | 32,00,000 | ||

| To Securities Premium A/c | 6,40,000 | ||

| To Premium on Redemption of Debentures A/c | 3,20,000 | ||

| (Transfer of Debenture application money and provision for premium on redemption) | |||

(iii) Books of Him Ltd. - Journal

| Date | Particulars | L.F. | Dr. Amount | Cr. Amount |

|---|---|---|---|---|

| Bank A/c Dr. | 40,00,000 | |||

| To Debenture Application and Allotment A/c | 40,00,000 | |||

| (Receipt of application money on 40,000, 13% Debentures of ₹100 each) | ||||

| Debenture Application and Allotment A/c Dr. | 40,00,000 | |||

| To 13% Debentures A/c | 40,00,000 | |||

| To Premium on redemption of Debentures A/c | 4,00,000 | |||

| (Transfer of debenture application money and provision for premium on redemption of Debentures made) | ||||

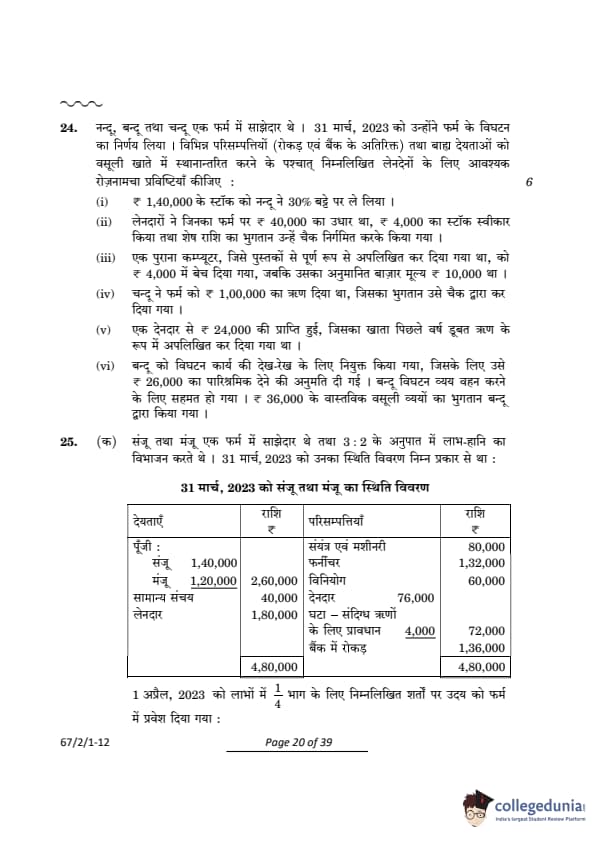

Question 24:

Nandu, Bandu, and Chandu were partners in a firm. On 31st March 2023 they decided to dissolve the firm. Pass necessary journal entries for the following transactions *after* the various assets (other than cash and bank) and outside liabilities have been transferred to Realisation Account:

(i) Stock of Rs. 1,40,000 was taken by Nandu at a discount of 30%.

(ii) Creditors to whom the firm owed Rs. 40,000 accepted stock at Rs. 4,000 and the balance amount was paid to them by cheque.

(iii) An old computer which had been written off completely from the books was sold for Rs. 4,000, whereas its estimated market value was Rs. 10,000.

(iv) Chandu had given a loan of Rs. 1,00,000 to the firm, which was paid to him through a cheque.

(v) Rs. 24,000 were recovered from a debtor which was written off as bad debt in the previous year.

(vi) Bandu was appointed to look after the dissolution work for which he was allowed a remuneration of Rs. 26,000. Bandu agreed to bear the dissolution expenses. Actual dissolution expenses of ₹ 36,000 were paid by Bandu.

View Solution

Solution: Books of Nandu, Bandu, and Chandu - Journal

| Date | Particulars | Dr. Amount (Rs.) | Cr. Amount (Rs.) |

|---|---|---|---|

| Nandu's Capital A/c Dr. | 98,000 | ||

| To Realisation A/c | 98,000 | ||

| (Stock taken over by Nandu at 30% discount) | |||

| Realisation A/c Dr. | 36,000 | ||

| To Bank A/c | 36,000 | ||

| (Creditors paid by cheque) | |||

| Cash/Bank A/c Dr. | 4,000 | ||

| To Realisation A/c | 4,000 | ||

| (Old computer sold) | |||

| Chandu's Loan A/c Dr. | 1,00,000 | ||

| To Bank A/c | 1,00,000 | ||

| (Chandu's loan paid through cheque) | |||

| Cash/Bank A/c Dr. | 24,000 | ||

| To Realisation A/c | 24,000 | ||

| (Bad Debts previously written off recovered) | |||

| Realisation A/c Dr. | 26,000 | ||

| To Bandu's Capital A/c | 26,000 | ||

| (Remuneration allowed to Bandu for carrying out dissolution work) | |||

| Bandu's Capital A/c Dr. | 36,000 | ||

| To Bank A/c | 36,000 | ||

| (Dissolution expenses paid by Bandu) | |||

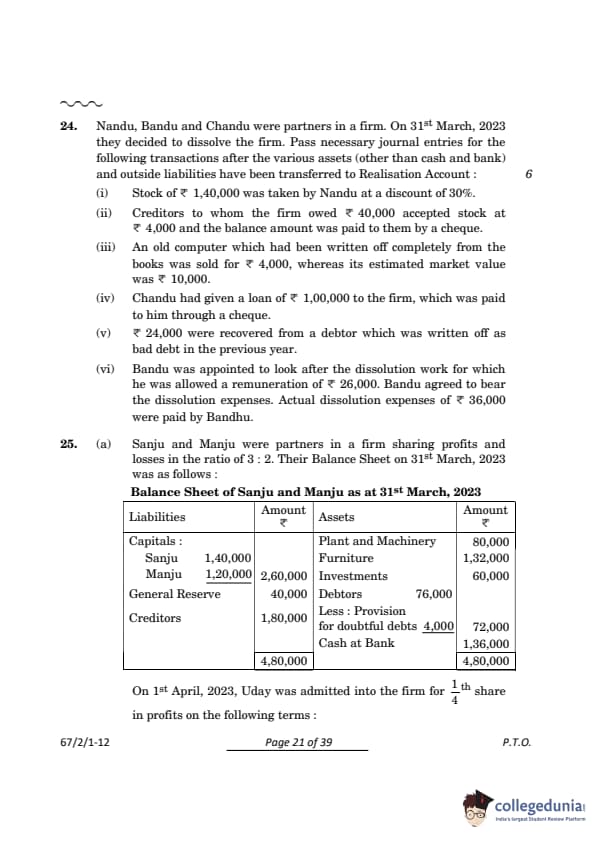

Question 25(a):

Sanju and Manju were partners in a firm sharing profits and losses in the ratio of 3:2. Their Balance Sheet on 31st March, 2023 was as follows:

Balance Sheet of Sanju and Manju as at 31st March, 2023

| Liabilities | Amount (₹) | Assets | Amount (₹) |

|---|---|---|---|

| Capitals: | Plant and Machinery | 80,000 | |

| Sanju | 1,40,000 | Furniture | 1,32,000 |

| Manju | 1,20,000 | Investments | 60,000 |

| Total Capitals | 2,60,000 | Debtors | 76,000 |

| General Reserve | 40,000 | Less: Provision for doubtful debts | (4,000) |

| Creditors | 1,80,000 | Cash at Bank | 1,36,000 |

| Total Liabilities | 4,80,000 | Total Assets | 4,80,000 |

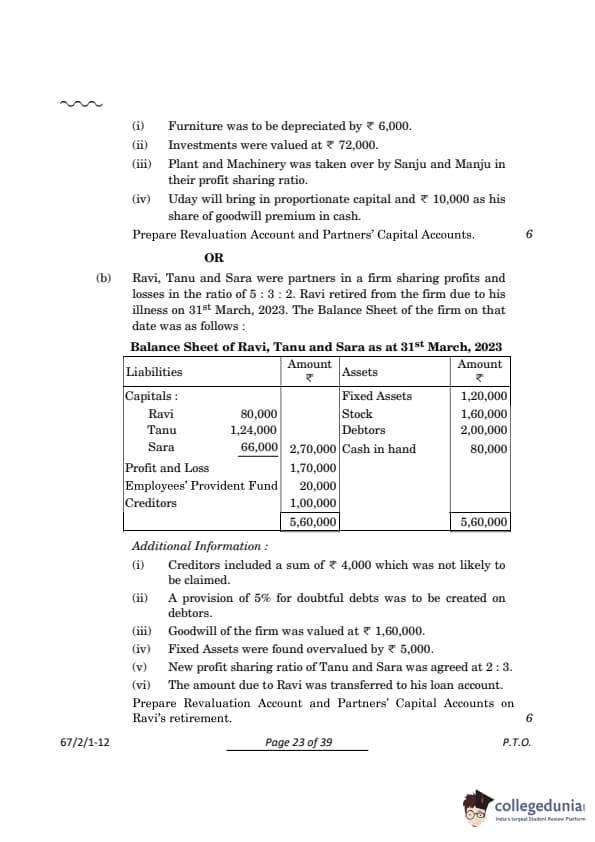

Adjustments:

1. Furniture was to be depreciated by 6,000.

2. Investments were valued at 72,000.

3. Plant and Machinery was taken over by Sanju and Manju in their profit-sharing ratio.

4. Uday will bring in proportionate capital and 10,000 as his share of goodwill premium in cash.

View Solution

Solution:

Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| Revaluation A/c Dr. | 6,000 | - | |

| To Furniture A/c | - | 6,000 | |

| (Depreciation of furniture recorded) | |||

| - | Investments A/c Dr. | 12,000 | - |

| To Revaluation A/c | - | 12,000 | |

| (Appreciation in the value of investments) | |||

| - | Revaluation A/c Dr. | 6,000 | - |

| To Sanju's Capital A/c | - | 3,600 | |

| To Manju's Capital A/c | - | 2,400 | |

| (Revaluation profit distributed in the ratio 3:2) | |||

| Cash A/c Dr. | 10,000 | - | |

| To Goodwill A/c | - | 10,000 | |

| (Uday's goodwill contribution received) | |||

| - | Goodwill A/c Dr. | 10,000 | - |

| To Sanju's Capital A/c | - | 6,000 | |

| To Manju's Capital A/c | - | 4,000 | |

| (Goodwill distributed to old partners in their profit-sharing ratio) | |||

| - | Cash A/c Dr. | 1,00,000 | - |

| To Uday's Capital A/c | - | 1,00,000 | |

| (Uday's proportionate capital brought in) | |||

Revaluation Account:

| Dr. | Amount (₹) | Cr. | Amount (₹) |

|---|---|---|---|

| Furniture (Depreciation) | 6,000 | Investments (Appreciation) | 12,000 |

| Profit transferred to: | |||

| Sanju's Capital A/c | 3,600 | ||

| Manju's Capital A/c | 2,400 | ||

| Total | 12,000 | Total | 12,000 |

Question 25(b):

Ravi, Tanu, and Sara were partners in a firm sharing profits and losses in the ratio of 5:3:2. Ravi retired from the firm due to his illness on 31st March, 2023. The Balance Sheet of the firm on that date was as follows:

Revaluation Account:

| Particulars | Amount (₹) |

|---|---|

| To Provision for Doubtful Debts (5% of 2,00,000) | 10,000 |

| To Creditors (Unclaimed Liability) | 4,000 |

| By Goodwill | 1,60,000 |

| By Fixed Assets (Overvaluation) | 5,000 |

| By Profit Transferred to: | |

| Ravi's Capital A/c (5/10) | 75,500 |

| Tanu's Capital A/c (3/10) | 45,300 |

| Sara's Capital A/c (2/10) | 30,200 |

| Total | 1,79,500 |

Partners' Capital Accounts:

| Particulars | Ravi (₹) | Tanu (₹) | Sara (₹) |

|---|---|---|---|

| By Balance b/d | 80,000 | 1,24,000 | 66,000 |

| By Revaluation Profit | 75,500 | 45,300 | 30,200 |

| To Goodwill Adjustment | 80,000 | 48,000 | 32,000 |

| To Loan Account (Ravi) | 75,500 | ||

| To Balance c/d | 1,21,300 | 64,200 | |

| Total | 1,55,500 | 1,69,300 | 98,200 |

View Solution

Solution:

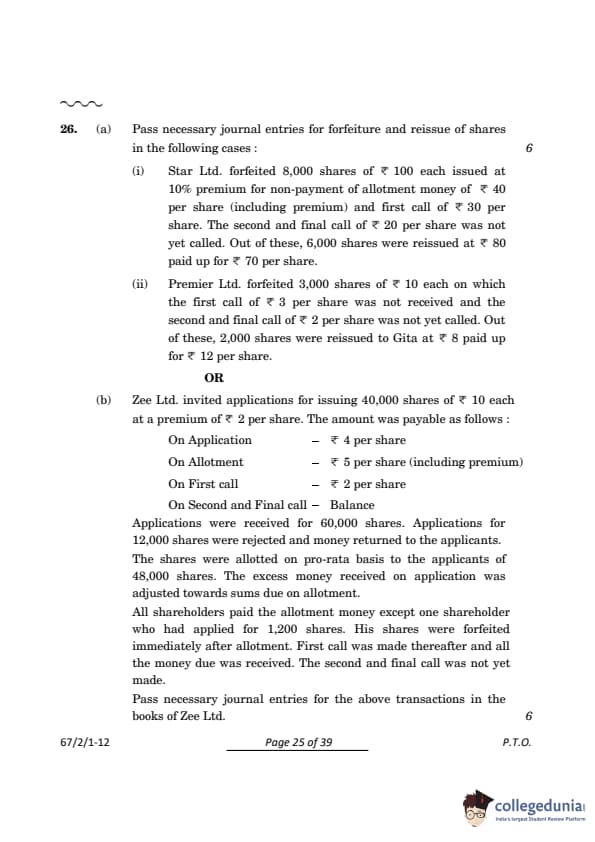

Question 26(a)(i):

Star Ltd. forfeited 8,000 shares of 100 each issued at 10% premium for non-payment of allotment money of 40 per share (including premium) and first call of 30 per share. The second and final call of 20 per share was not yet called. Out of these, 6,000 shares were reissued at 80 paid up for 70 per share. Pass necessary journal entries.

(i) Star Ltd.:

Given:

• 8,000 shares forfeited (100 each, 10% premium).

• Allotment unpaid: 40/share (including premium).

• First call unpaid: 30/share.

• Second and final call of 20/share not yet called.

• 6,000 shares reissued at 80 paid up for 70/share.

View Solution

Solution:

Journal Entries:

| Date | Particulars | Debit (₹) | Credit (₹) |

|---|---|---|---|

| - | Share Capital A/c Dr. | 6,40,000 | - |

| Securities Premium A/c Dr. | 80,000 | - | |

| To Share Forfeiture A/c | - | 5,60,000 | |

| To Share Allotment A/c | - | 3,20,000 | |

| To Share First Call A/c | - | 2,40,000 | |

| (Forfeiture of 8,000 shares for non-payment of allotment and first call money) | |||

| - | Bank A/c Dr. | 4,20,000 | - |

| Share Forfeiture A/c Dr. | 60,000 | - | |

| To Share Capital A/c | - | 4,80,000 | |

| (6,000 shares reissued at 70 each, fully paid-up at 80) | |||

| - | Share Forfeiture A/c Dr. | 5,00,000 | - |

| To Capital Reserve A/c | - | 5,00,000 | |

| (Transfer of remaining forfeiture balance to Capital Reserve) | |||

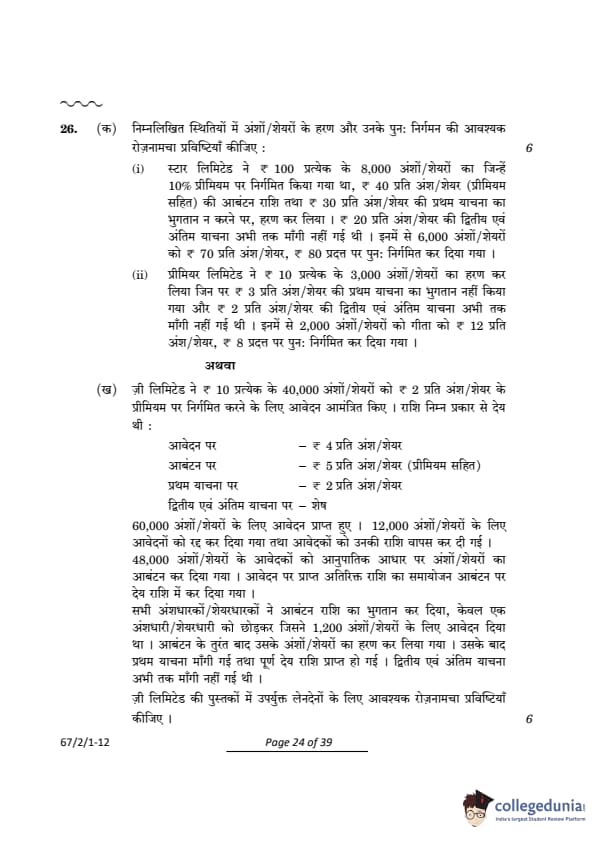

Question 26(a):

Pass necessary journal entries for forfeiture and reissue of shares in the following cases:

(i) Star Ltd. forfeited 8,000 shares of ₹100 each issued at 10% premium for non-payment of allotment money of ₹40 per share (including premium) and first call of ₹30 per share. The second and final call of ₹20 per share was not yet called. Out of these, 6,000 shares were reissued at ₹80 paid up for ₹70 per share.

(ii) Premier Ltd. forfeited 3,000 shares of ₹10 each on which the first call of ₹3 per share was not received and the second and final call of ₹2 per share was not yet called. Out of these, 2,000 shares were reissued to Gita at ₹8 paid up for ₹12 per share.

View Solution

Solution (i) Star Ltd.:

Books of Star Ltd. - Journal

| Date | Particulars | Dr. Amount (₹) | Cr. Amount (₹) |

|---|---|---|---|

| Share Capital A/c Dr. | 6,40,000 | ||

| Securities Premium A/c Dr. | 80,000 | ||

| To Share Forfeiture A/c | 1,60,000 | ||

| To Calls in Arrears A/c (Allotment) | 3,20,000 | ||

| To Calls in Arrears A/c (First Call) | 2,40,000 | ||

| (8,000 shares forfeited for non-payment of allotment and 1st call money) | |||

| Bank A/c Dr. | 4,20,000 | ||

| Share Forfeiture A/c Dr. | 60,000 | ||

| To Share Capital A/c | 4,80,000 | ||

| (6,000 shares reissued at ₹70, ₹80 paid up) | |||

| Share Forfeiture A/c Dr. | 5,00,000 | ||

| To Capital Reserve A/c | 5,00,000 | ||

| (Gain on reissue of 6,000 shares transferred to capital reserve) | |||

Solution (ii) Premier Ltd.:

Books of Premier Ltd. - Journal

| Date | Particulars | Dr. Amount (Rs.) | Cr. Amount (Rs.) |

|---|---|---|---|

| Share Capital A/c Dr. | 24,000 | ||

| To Share Forfeiture A/c | 9,000 | ||

| To Calls in Arrears A/c | 9,000 | ||

| (3,000 shares forfeited for non-payment of 1st call money) | |||

| Bank A/c Dr. | 16,000 | ||

| Share Forfeiture A/c Dr. | 4,000 | ||

| To Share Capital A/c | 20,000 | ||

| (2,000 shares reissued @ Rs. 12 per share, Rs. 8 paid up) | |||

| Share Forfeiture A/c Dr. | 1,000 | ||

| To Capital Reserve A/c | 1,000 | ||

| (Gain on reissue of 2,000 shares transferred to capital reserve) | |||

Question 26(b):

Zee Ltd. invited applications for issuing 40,000 shares of ₹10 each at a premium of ₹2 per share. The amount was payable as follows:

- On Application – ₹4 per share

- On Allotment – ₹5 per share (including premium)

- On First Call – ₹2 per share

- On Second and Final Call – Balance

Applications were received for 60,000 shares. Applications for 12,000 shares were rejected, and money returned to the applicants. The shares were allotted on a pro-rata basis to the applicants of 48,000 shares. The excess money received on application was adjusted towards sums due on allotment.

All shareholders paid the allotment money *except* one shareholder who had applied for 1,200 shares. His shares were forfeited immediately after allotment. The first call was made thereafter, and all the money due was received. The second and final call was not yet made.

Pass necessary journal entries for the above transactions in the books of Zee Ltd.

View Solution

Solution: Journal Entries

| Date | Particulars | Dr. Amount (₹) | Cr. Amount (₹) |

|---|---|---|---|

| Bank A/c Dr. | 2,40,000 | ||

| To Share Application A/c | 2,40,000 | ||

| (Application money received on 60,000 shares) | |||

| Share Application A/c Dr. | 2,40,000 | ||

| To Share Capital A/c | 1,60,000 | ||

| To Share Allotment A/c | 64,000 | ||

| To Bank A/c | 16,000 | ||

| (Application money transferred to Share Capital A/c, excess refunded, and adjusted towards allotment) | |||

| Share Allotment A/c Dr. | 2,00,000 | ||

| To Share Capital A/c | 1,20,000 | ||

| To Securities Premium A/c | 80,000 | ||

| (Amount due on allotment) | |||

| Bank A/c Dr. | 1,94,000 | ||

| Calls in Arrears A/c Dr. | 4,200 | ||

| To Share Allotment A/c | 1,98,200 | ||

| (Allotment money received, except on 1,200 shares at ₹5 each = ₹6000. Considering pro-rata allotment, the calls in arrears on these 1200 shares is ₹4*1200 = ₹4800 and thus ₹1200(₹6000-₹4800) needs to be adjusted from share allotment) | |||

| Share Capital A/c Dr. | 7,200 | ||

| Securities Premium A/c Dr. | 2,400 | ||

| To Share Forfeiture A/c | 9,600 | ||

| (1,200 shares forfeited for non-payment of allotment money) | |||

| Share First Call A/c Dr. | 78,000 | ||

| To Share Capital A/c | 78,000 | ||

| (Amount due on First call on 39,000 shares i.e., after forfeiture of 1200 shares) | |||

| Bank A/c Dr. | 78,000 | ||

| To Share First Call A/c | 78,000 | ||

| (First call money received) | |||

PART B

OPTION I

(Analysis of Financial Statements)

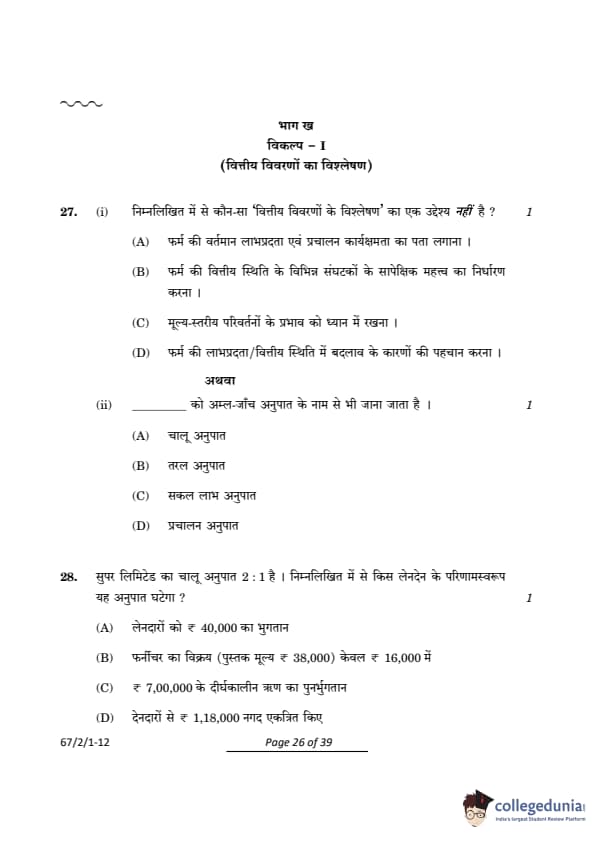

Question 27(i):

Which of the following is *not* an objective of ‘Analysis of Financial Statements’?

View Solution

Solution: The primary objective of financial statement analysis is to evaluate the profitability, financial health, and efficiency of the firm. It also helps understand the contribution of various financial components to the company's overall position. However, the analysis does *not* take into account price level changes; these are typically handled by inflation accounting or price level adjustment techniques.

Question 27(ii):

_____ is also known as Acid-Test Ratio.

View Solution

Solution: The Quick Ratio, often referred to as the Acid-Test Ratio, measures a company's ability to meet its short-term obligations using its most liquid assets (cash, marketable securities, and receivables). It excludes inventory and prepaid expenses as they are less liquid compared to other current assets.

Question 28:

Current Ratio of Super Ltd. is 2:1. Which of the following transactions will result in a decrease in this ratio?

View Solution

Solution: The current ratio is calculated as the ratio of current assets to current liabilities. Let's evaluate each transaction: 1. Payment of ₹40,000 to creditors: This reduces both current assets (cash) and current liabilities (creditors) equally, leaving the ratio unchanged. 2. Sale of furniture for ₹16,000: Furniture is a non-current asset, so this transaction does not impact the current ratio. 3. Repayment of long-term loan: This reduces current assets (cash) but does not affect current liabilities, leading to a decrease in the current ratio. 4. Cash collected from debtors: This is a movement within current assets (from debtors to cash), keeping the ratio unchanged.

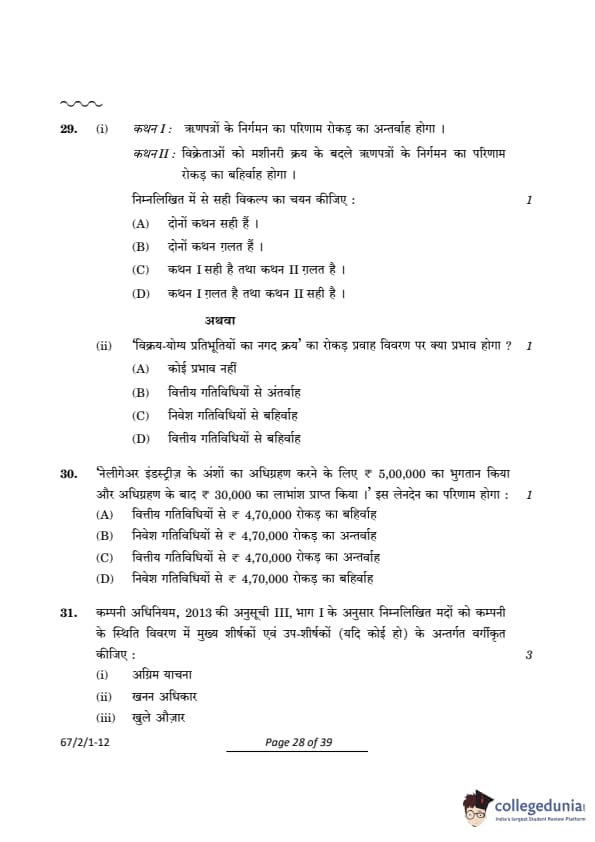

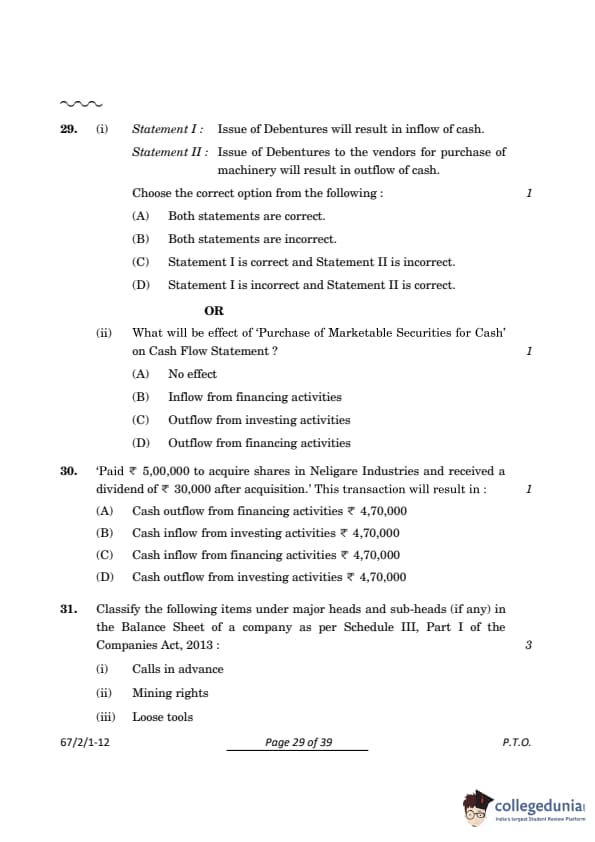

Question 29(i):

Statement I: Issue of Debentures will result in inflow of cash.

Statement II: Issue of Debentures to the vendors for purchase of machinery will result in outflow of cash.

Choose the correct option from the following:

View Solution

Solution:

Statement I: The issue of debentures results in cash inflow as it involves borrowing money from investors, leading to an increase in the firm's cash resources. Hence, this statement is correct.

Statement II: When debentures are issued to vendors for the purchase of machinery, no cash flow is involved in the transaction. It is a non-cash financing activity. Therefore, this statement is incorrect.

Question 29(ii):

What will be the effect of ‘Purchase of Marketable Securities for Cash’ on the Cash Flow Statement?

View Solution

Solution: The purchase of marketable securities for cash is classified as an investing activity because it involves acquiring a short-term asset. Such purchases lead to a reduction in cash resources, hence *no effect* will be there in the cash flow statement. It's a shift of assets, not a change in overall cash.

Question 30:

'Paid ₹5,00,000 to acquire shares in Neligare Industries and received a dividend of ₹30,000 after acquisition.' This transaction will result in:

View Solution

Solution: The payment for acquiring shares is considered an outflow under investing activities. Dividend income is also classified under investing activities and reduces the net outflow. Therefore:

Net Cash Flow = ₹5,00,000 – ₹30,000 = ₹4,70,000

This results in a cash outflow under investing activities.

Question 31:

Classify the following items under major heads and sub-heads (if any) in the Balance Sheet of a company as per Schedule III, Part I of the Companies Act, 2013 :

(i) Calls in advance

(ii) Mining rights

(iii) Loose tools

View Solution

Solution:

| S.No. | Items | Heads | Sub Heads |

|---|---|---|---|

| (i) | Calls in advance | Current Liabilities | Other Current Liabilities |

| (ii) | Mining rights | Non-Current Assets | Fixed Assets / Property, Plant & Equipment & Intangible Assets - Intangible Assets |

| (iii) | Loose tools | Current Assets | Inventories |

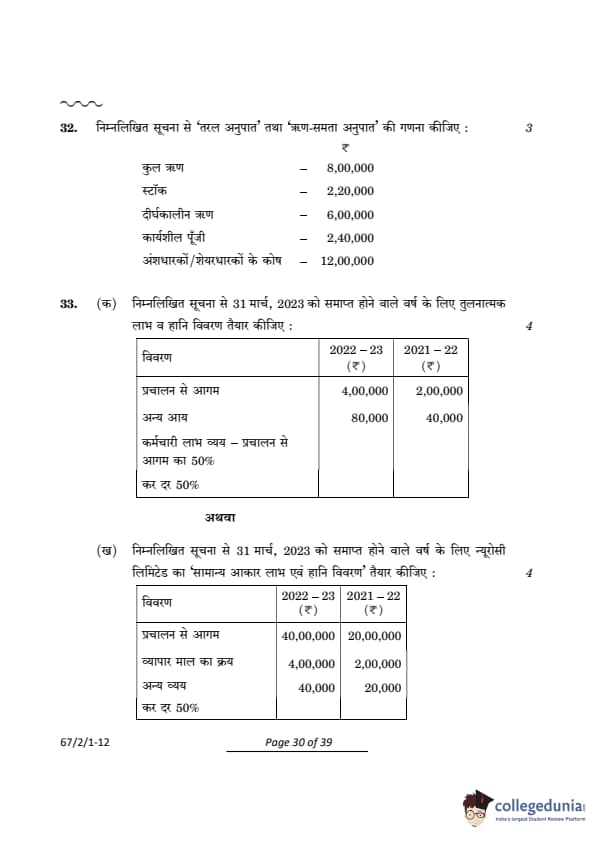

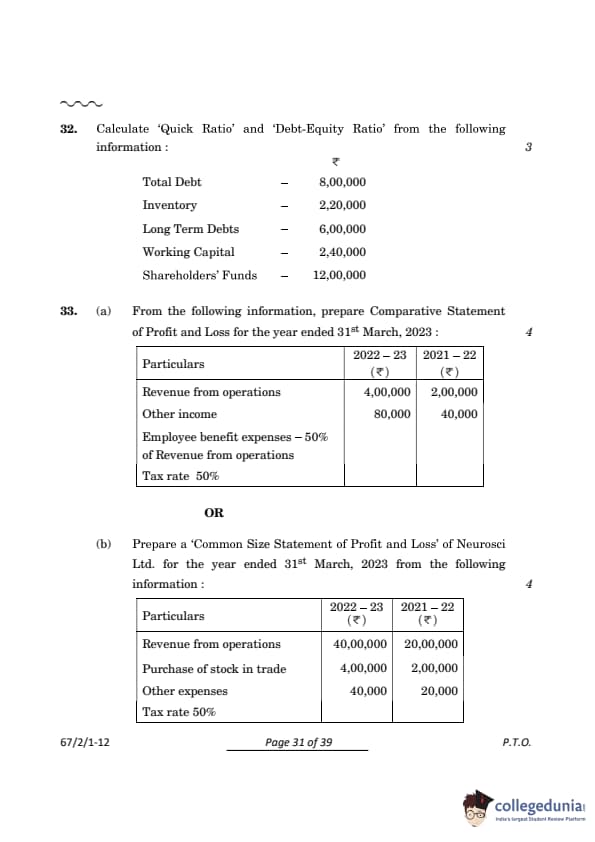

Question 32:

Calculate ‘Quick Ratio’ and ‘Debt-Equity Ratio’ from the following information:

| Particulars | Amount (Rs.) |

|---|---|

| Total Debt | 8,00,000 |

| Inventory | 2,20,000 |

| Long Term Debts | 6,00,000 |

| Working Capital | 2,40,000 |

| Shareholders' Funds | 12,00,000 |

View Solution

Solution:

Quick Ratio = Quick Assets⁄Current Liabilities

Current Liabilities = Total Debt - Long Term Debt

Current Liabilities = 8,00,000 – 6,00,000 = 2,00,000

Quick Assets = Current Assets - Inventory

Current Assets = Working Capital + Current Liabilities

Current Assets = 2,40,000 + 2,00,000 = 4,40,000

Quick Assets = 4,40,000 - 2,20,000 = 2,20,000

Quick Ratio = 2,20,000⁄2,00,000 = 1.1:1

Debt-Equity Ratio = Debt⁄Equity

Debt = Long Term Debt = 6,00,000

Equity = Shareholder's Funds = 12,00,000

Debt-Equity Ratio = 6,00,000⁄12,00,000 = 1:2 or 0.5:1

Question 33(a):

From the following information, prepare Comparative Statement of Profit and Loss for the year ended 31st March, 2023:

| Particulars | 2022-23 (₹) | 2021-22 (₹) |

|---|---|---|

| Revenue from operations | 4,00,000 | 2,00,000 |

| Other income | 80,000 | 40,000 |

| Employee benefit expenses - 50% of Revenue from operations | ||

| Tax rate 50% |

View Solution

Solution:

| Particulars | 2022-23 (₹) | 2021-22 (₹) | % Change |

|---|---|---|---|

| Revenue from operations | 4,00,000 | 2,00,000 | 100% |

| Other income | 80,000 | 40,000 | 100% |

| Total Income | 4,80,000 | 2,40,000 | 100% |

| Employee benefit expenses | 2,00,000 | 1,00,000 | 100% |

| Profit before tax | 2,80,000 | 1,40,000 | 100% |

| Tax (50%) | 1,40,000 | 70,000 | 100% |

| Profit after tax | 1,40,000 | 70,000 | 100% |

Question 33(b):

Prepare a ‘Common Size Statement of Profit and Loss' of Neurosci Ltd. for the year ended 31st March, 2023 from the following information:

| Particulars | 2022-23 (₹) | 2021–22 (₹) |

|---|---|---|

| Revenue from operations | 40,00,000 | 20,00,000 |

| Purchase of stock in trade | 4,00,000 | 2,00,000 |

| Other expenses | 40,000 | 20,000 |

| Tax rate | 50% | 50% |

View Solution

Solution:

| Particulars | % of Revenue (2022–23) | % of Revenue (2021–22) |

|---|---|---|

| Revenue from operations | 100.00% | 100.00% |

| Purchase of stock in trade | 10.00% | 10.00% |

| Other expenses | 1.00% | 1.00% |

| Profit before tax | 89.00% | 89.00% |

| Tax (50%) | 44.50% | 44.50% |

| Profit after tax | 44.50% | 44.50% |

Table 1: Common Size Statement of Profit and Loss for Neurosci Ltd.

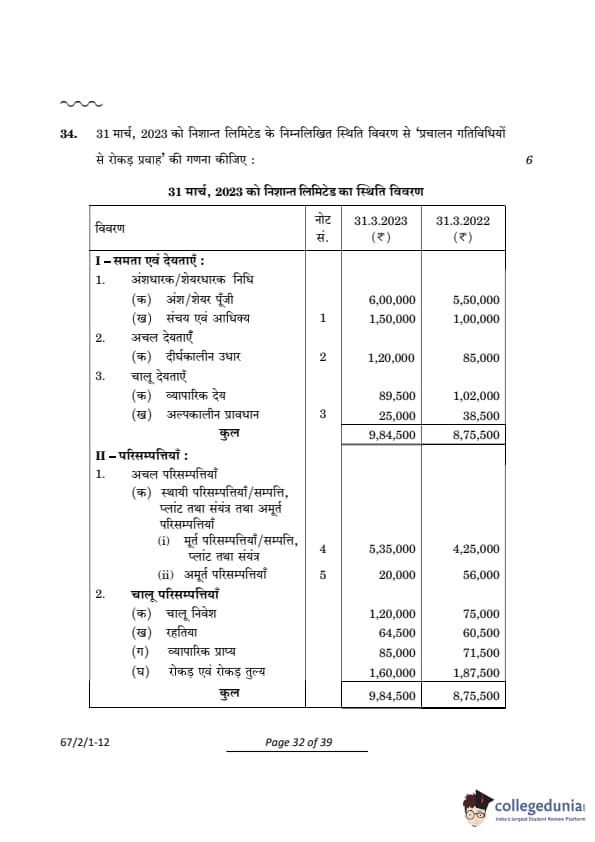

Question 34:

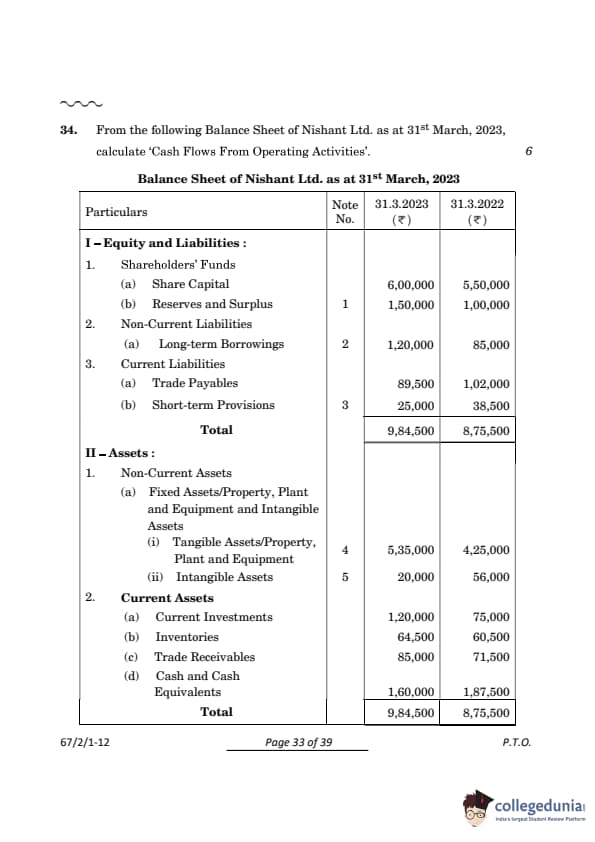

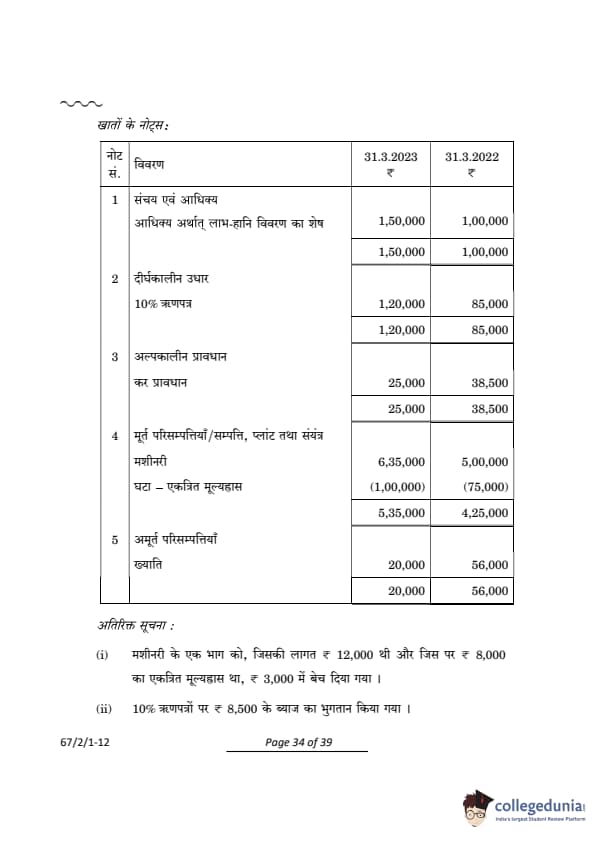

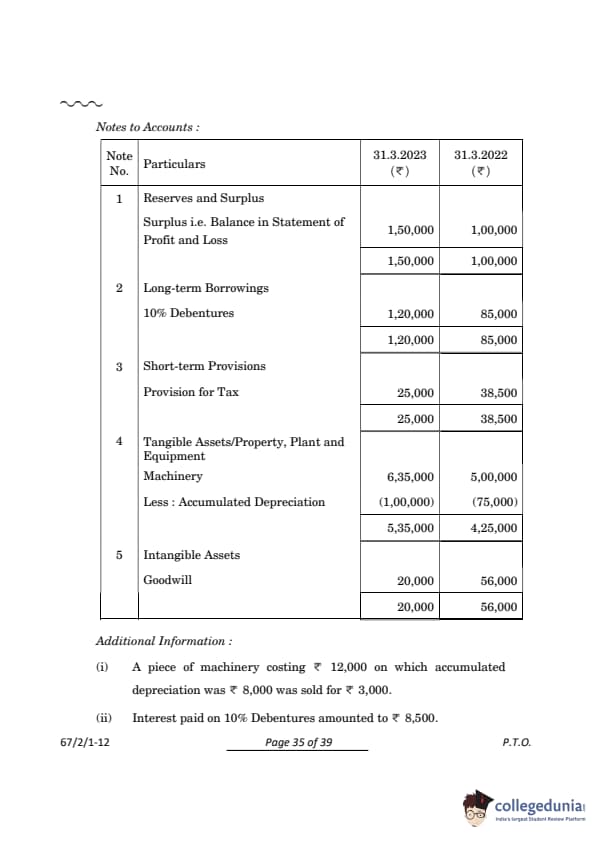

From the following Balance Sheet of Nishant Ltd. as at 31st March ```html 2023, calculate “Cash Flows From Operating Activities’.

(Note: The provided Balance Sheet and Notes to Accounts are extensive and have already been formatted in a previous response. To avoid redundancy, I will omit those tables here. Please refer back to the earlier formatted content for the full tables if needed.)

Additional Information:

- A piece of machinery costing ₹12,000 on which accumulated depreciation was ₹8,000 was sold for ₹3,000.

- Interest paid on 10% Debentures amounted to ₹8,500.

View Solution

Solution:

Calculation of Cash Flows from Operating Activities:

- Net Profit before Tax & Extraordinary Items:

- Net Profit (Increase in Reserves and Surplus) = ₹1,50,000 – ₹1,00,000 = ₹50,000

Add: Non-Cash and Non-Operating Items:

- Depreciation on Machinery (calculated below)

- Loss on Sale of Machinery = ₹1,000 (₹12,000 - ₹8,000 - ₹3,000)

- Interest on Debentures = ₹8,500

- Goodwill Written Off = ₹36,000 (Decrease in Goodwill from Balance Sheet)

- Changes in Working Capital:

Particulars 2023 (₹) 2022 (₹) Effect on Cash Flow Trade Payables 89,500 1,02,000 Decrease ₹12,500 Short-term Provisions 25,000 38,500 Decrease ₹13,500 Inventories 64,500 60,500 Increase ₹4,000 Trade Receivables 85,000 71,500 Increase ₹13,500 Net *Decrease* in Working Capital = ₹12,500 + ₹13,500 - ₹4,000 - ₹13,500 = ₹8,500

- Net Cash Flow from Operating Activities:

Net Cash Flow from Operating Activities = Net Profit Before Tax + Non-Cash and Non-Operating Items – Net Decrease in Working Capital.

Calculation of Depreciation:

| Dr. | Amount (₹) | Cr. | Amount (₹) |

|---|---|---|---|

| To Machinery A/c | 8,000 | By Balance b/d | 75,000 |

| To Balance c/d | 1,00,000 | By Depreciation A/c (Balancing Figure) | 33,000 |

| Total | 1,08,000 | Total | 1,08,000 |

Depreciation = ₹33,000

Net Cash Flow from Operating Activities: ₹50,000 + ₹33,000 + ₹1,000 + ₹8,500 + ₹36,000 - ₹8,500 = ₹120,500

PART B

OPTION II

(Computerised Accounting)

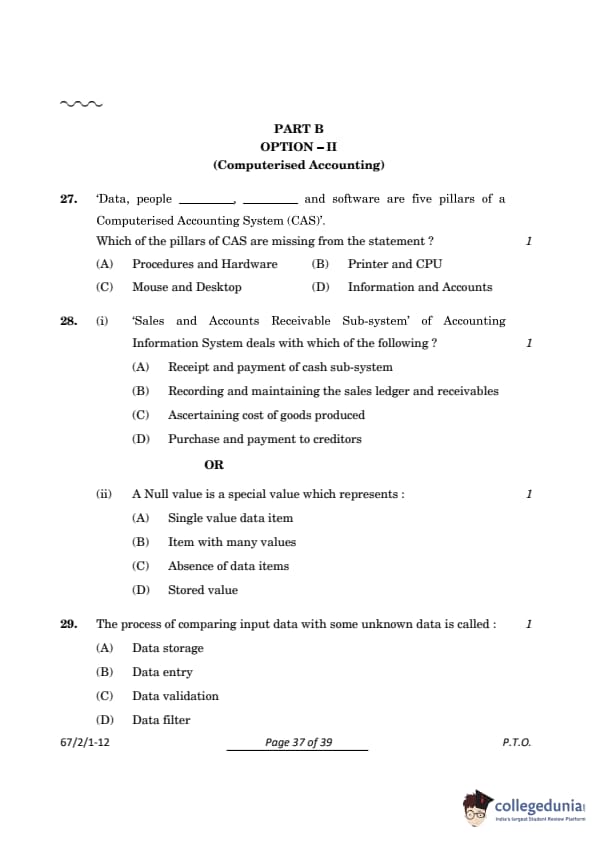

Question 27:

'Data, people _______, and software' are five pillars of a Computerised Accounting System (CAS). Which of the pillars of CAS are missing from the statement?

View Solution

Solution: The five pillars of a Computerised Accounting System (CAS) are:

1. Data

2. People

3. Procedures

4. Hardware

5. Software

Procedures define the methods and processes, while hardware refers to the physical infrastructure used in the system.

Question 28(a):

(i) ‘Sales and Accounts Receivable Sub-system' of Accounting Information System deals with which of the following?

View Solution

Solution: The Sales and Accounts Receivable Sub-system of an Accounting Information System (AIS) is responsible for managing sales records and tracking outstanding receivables. It ensures that all sales transactions are accurately recorded and customer balances are properly maintained.

Question 28(b):

(ii) A Null value is a special value which represents:

View Solution

Solution: A Null value is used in databases to indicate the absence of any data for a specific field or item. It signifies that no value has been entered or that the value is unknown, making it distinct from zero or an empty string.

Question 29:

The process of comparing input data with some unknown data is called:

View Solution

Solution: Data validation is the process of verifying whether input data meets specific criteria or matches known values. It ensures the accuracy and reliability of data by comparing it with a reference set or predefined rules. - Data storage involves saving data. Data entry refers to the act of inputting data into a system. - Data filtering is used to display or retrieve specific data based on certain conditions.

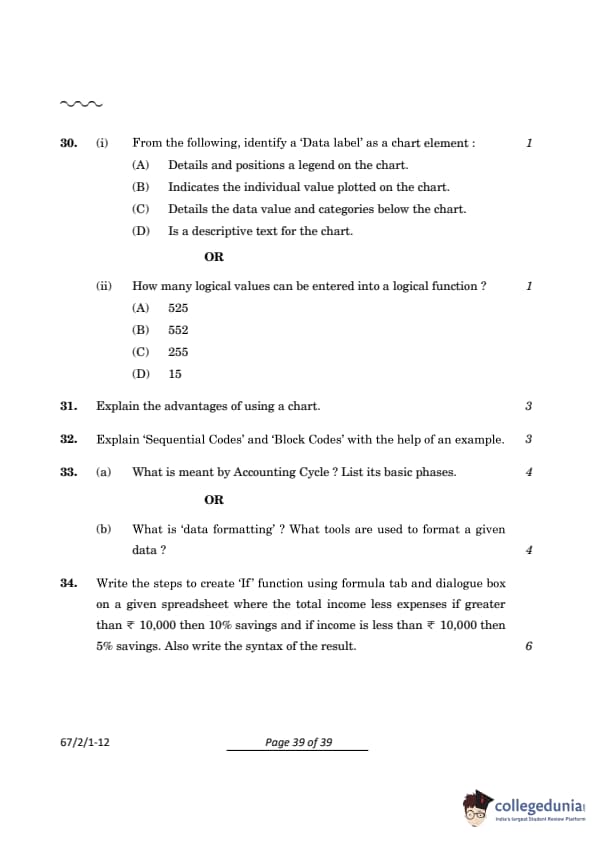

Question 30(a):

(i) From the following, identify a ‘Data label' as a chart element:

View Solution

Solution: Step 1: Understanding a Data Label. A data label is a chart element that displays the value of each data point directly on the chart, making it easier to interpret the information visually. It is typically placed near the corresponding data point for better clarity. Step 2: Analyze the options. Option (A): This refers to the legend, which explains the symbols or colors used in the chart, not the individual data points. Option (B): This is correct because a data label directly indicates the value of each individual data point plotted on the chart. Option (C): This describes the axis or gridlines, which are unrelated to data labels. - Option (D): This refers to the chart title or description, not a data label. Step 3: Finalize the answer. The correct answer is (B) Indicates the individual value plotted on the chart.

Question 30(b):

(ii) How many logical values can be entered into a logical function?

View Solution

Solution: Logical functions in spreadsheet software, such as ‘IF‘, ‘AND‘, or 'OR', typically allow up to 255 logical arguments. This ensures manageable complexity and efficient processing of the function.

Question 31:

Explain the advantages of using a chart.

View Solution

Solution: Charts offer various advantages, including:

- Visual Clarity: Charts provide a clear visual representation of data, making it easier to understand and interpret.

- Comparative Analysis: They allow easy comparison between different data points, helping to highlight trends and relationships.

- Summarizing Data: Complex data sets can be simplified into a more digestible format.

- Quick Insights: Charts offer immediate insight into data, enabling faster decision-making.

- Enhanced Communication: They make it easier to communicate information to a wider audience, particularly in presentations.

Question 32:

Explain 'Sequential Codes' and ‘Block Codes' with the help of an example.

View Solution

Solution:

Sequential Codes: Sequential codes are used when data is assigned in a predetermined, consecutive order. They help organize information based on a sequence. For example, in a product inventory system, products might be assigned sequential numbers (e.g., 001, 002, 003, etc.) for easy tracking.

Block Codes: Block codes assign numbers in a fixed-length format, where each part of the code represents specific information. For instance, in a coding system for products, the first two digits may represent the product category, and the next three digits represent a specific product in that category (e.g., 12-345 for product 345 in category 12).

Question 33(a):

What is meant by Accounting Cycle? List its basic phases.

View Solution

Solution: The accounting cycle is a systematic series of steps followed to record, process, and summarize financial transactions over a specific period, culminating in the preparation of financial statements.

The basic phases of the accounting cycle are:

1. Identifying Transactions: Recognizing financial events and transactions.

2. Recording Transactions: Entering transactions in the journal.

3. Posting to Ledger: Classifying transactions in ledger accounts.

4. Trial Balance: Preparing a trial balance to ensure the books are balanced.

5. Adjusting Entries: Making corrections for accrued and deferred items.

6. Financial Statements: Preparing the income statement, balance sheet, and cash flow statement.

7. Closing Entries: Closing temporary accounts and transferring balances to permanent accounts.

Question 33(b):

What is ‘data formatting'? What tools are used to format a given data?

View Solution

Solution: Data formatting involves modifying the appearance or arrangement of data to improve its clarity, presentation, and readability.

It includes setting number formats, text alignment, font styles, and applying conditional formatting.

Tools used for data formatting include:

1. Spreadsheet Software (e.g., Excel, Google Sheets): For formatting tables, charts, and data cells.

2. Data Visualization Tools (e.g., Tableau, Power BI): To create and format visual representations like graphs and dashboards.

3. Word Processing Tools (e.g., Microsoft Word): For formatting reports and tables for professional presentation.

Question 34:

Write the steps to create ‘If’ function using formula tab and dialogue box on a given spreadsheet where the total income less expenses if greater than ₹10,000 then 10% savings and if income is less than ₹10,000 then 5% savings. Also write the syntax of the result.

View Solution

Solution: To create the 'If' function in a spreadsheet:

1. Select the cell where you want the result to appear.

2. Open the formula tab and click on the “Insert Function” option.

3. From the function list, choose "IF”.

4. In the logical test field, input the condition: (income – expenses) > 10000.

5. In the value if true field, input: (income – expenses) × 10%.

6. In the value if false field, input: (income – expenses) × 5%.

7. Click "OK" to finalize and apply the formula.

The syntax of the function is:

=IF((income - expenses) > 10000, (income - expenses) ×10%, (income – expenses) × 5%)

Comments