.png?h=35&w=35&mode=stretch)

CBSE Class 12 Accountancy Set 2 Question Paper PDF (Code: 67/4/2) is now available for download. CBSE conducted the Class 12 Accountancy examination on March 23, 2024, from 10:30 AM to 1:30 PM. The question paper consists of 34 questions carrying a total of 80 marks. Part A is compulsory for all candidates. Part B has two options. Candidates have to attempt only one of the given options. Option I : Analysis of Financial Statements and Option II : Computerised Accounting. Candidates can use the link below to download the CBSE Class 12 Accountancy Set 2 Question Paper with detailed solutions.

CBSE Class 12 Accountancy Question Paper 2024 (Set 2- 67/4/2) with Answer Key

| CBSE Class 12 2024 Accountancy Question Paper with Answer Key | Check Solution |

CBSE Class 12 2024 Accountancy Questions with Solutions

PART A

(Accounting for Partnership Firms and Companies)

Question 1:

If vendors are issued fully paid shares of Rs. 1,25,000 in purchase consideration of net assets of Rs. 1,50,000, the balance of Rs. 25,000 will be credited to:

View Solution

When shares valued at Rs. 1,25,000 are issued to vendors against net assets worth Rs. 1,50,000, a gain of Rs. 25,000 results. This gain, which arises from the net assets exceeding the issued share value, is recorded in the Capital Reserve Account, following accounting norms. Quick Tip: When the value of acquired net assets surpasses the consideration paid, the excess is allocated to the Capital Reserve Account, signifying a financial advantage from the transaction.

(a) Riya, Rita and Renu were partners in a firm. On 31st March, 2023 Renu retired. The amount payable to Renu Rs. 2,17,000 was transferred to her loan account. Renu agreed to receive interest on this amount as per the provisions of Partnership Act, 1932. The rate at which interest would be paid to Renu is:

View Solution

Under the Indian Partnership Act of 1932, unless otherwise specified in the partnership agreement, the interest on a partner’s loan is calculated at \(6%\ p.a.\). In this case, as no alternate rate is specified, \(6%\ p.a.\) is the interest rate to be applied. Quick Tip: Refer to the Indian Partnership Act, 1932, when the partnership deed does not specify terms. The standard interest rate for a partner's loan is \(6%\ p.a.\) unless stated differently in the agreement.

(b) Ravi, Vani and Toni were equal partners in a firm. After the retirement of Vani, the capital balances of Ravi and Toni were Rs. 1,56,000 and Rs. 1,08,000 respectively. The new capital of the firm was determined at Rs. 2,80,000. It was decided that the capital will be in proportion of the profit sharing ratio of the remaining partners. Toni will bring ..... for deficiency in his new capital.

View Solution

Step 1: Calculate the required new capital for each partner.

With Vani's retirement, the remaining partners, Ravi and Toni, share the new capital equally. The new capital for each should be \( \frac{2,80,000}{2} = Rs.1,40,000 \).

Step 2: Determine Toni's capital deficiency.

Toni's existing capital is Rs.1,08,000. The deficiency to meet the new requirement is: \[ Rs.1,40,000 - Rs.1,08,000 = Rs.32,000 \] Quick Tip: It is crucial to adjust capital contributions in line with the predefined profit-sharing ratio after any changes in partnership, such as a partner's retirement.

Assertion (A): Interest on bearer debentures is paid to a person who produces the interest coupon attached to such debentures.

Reason (R): Bearer debentures are transferred by way of delivery and the company does not keep any record of these debenture holders.

Choose the correct option from the following:

View Solution

Bearer debentures are securities where the holder's name is not registered; interest is paid to the bearer upon coupon submission. Therefore, Assertion (A) is valid.

Moreover, these debentures can be transferred simply by handing them over, and companies do not keep a record of their holders. Hence, Reason (R) is accurate and illustrates the basis for paying interest upon coupon submission. Quick Tip: Bearer debentures allow for easy transfer as they are not registered to a specific owner, though this increases the risk as no records are kept of ownership.

Vishnu and Mishu are partners in a firm. Mishu draws a fixed amount at the end of every quarter. Interest on drawings is charged @ \(15% \ p.a.\). At the end of the year interest on Mishu's drawings amounted to Rs. 9,000. Interest on drawings was charged on drawings of Mishu for:

View Solution

Step 1: Understanding the time period for interest calculation.

Since Mishu makes drawings at the end of each quarter, the amount is available for interest calculation for a lesser period.

Step 2: Weighted average period for quarterly end drawings.

For quarterly end drawings, the standard weighted average period is 4 ½ months.

Step 3: Matching with options.

Among the given choices, the closest and correct answer is 4 ½ months. Quick Tip: When calculating interest on regular fixed withdrawals, use established average periods: 6 months (beginning of the period), 7.5 months (end of the period), and \(5 \frac{1}{2}\) months (mid-period).

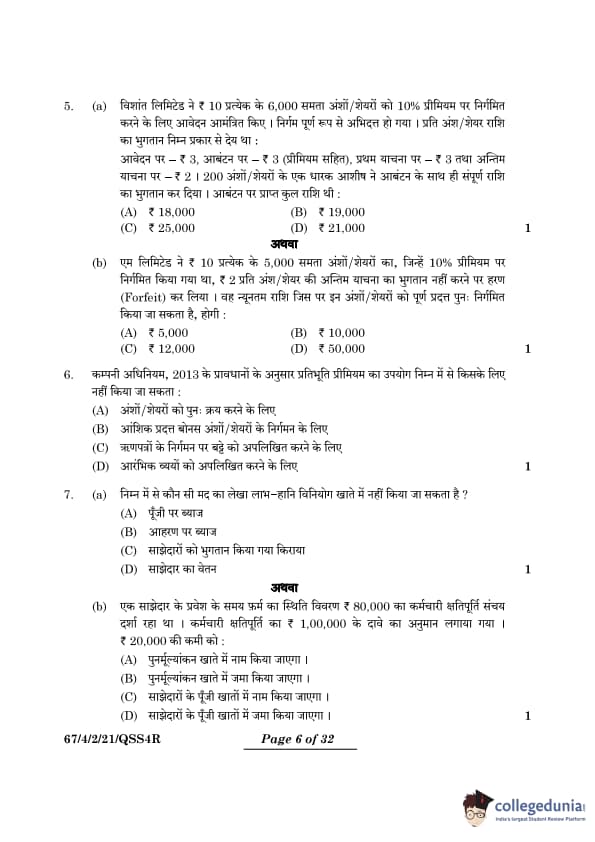

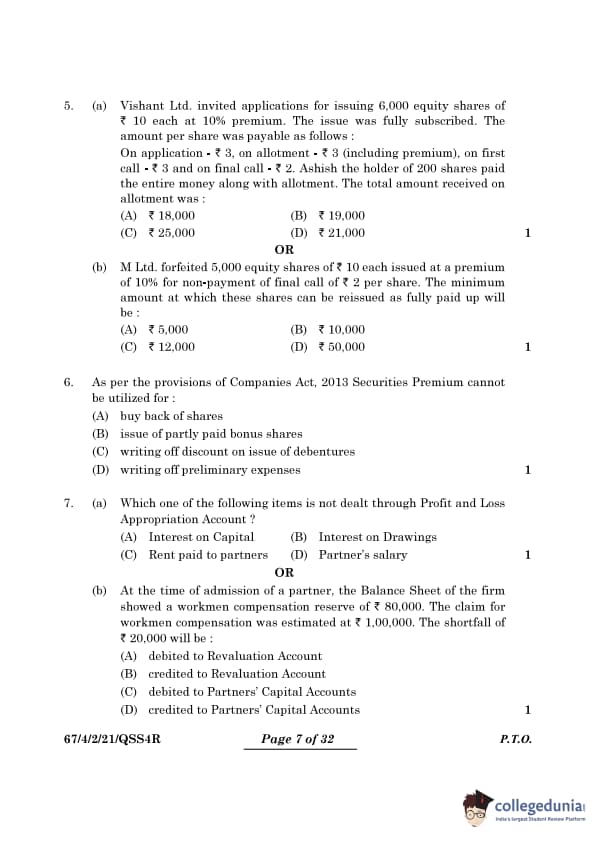

(a) Vishant Ltd. invited applications for issuing 6,000 equity shares of Rs. 10 each at 10% premium. The issue was fully subscribed. The amount per share was payable as follows: On application - Rs. 3, on allotment - Rs. 3 (including premium), on first call - Rs. 3 and on final call - Rs. 2. Ashish the holder of 200 shares paid the entire money along with allotment. The total amount received on allotment was:

View Solution

Calculate the Total Amount Due on Allotment (Excluding Ashish's Advance):

Amount due per share (including premium): Rs.3

Number of shares (excluding Ashish's): 6,000 - 200 = 5,800

Total amount due: Rs.3 * 5,800 = Rs.17,400

Calculate the Amount Ashish Paid in Advance:

Ashish paid for First Call and Final Call along with allotment.

Amount paid in advance per share: Rs.3 (First Call) + Rs.2 (Final Call) = Rs.5

Total amount paid in advance: Rs.5 * 200 = Rs.1,000

Calculate the Amount Ashish Paid on Allotment:

Amount due on allotment per share: Rs.3

Ashish's shares: 200

Amount Ashish paid on allotment: Rs.3 * 200 = Rs.600

Calculate the Total Amount Received on Allotment:

\begin{align*

\text{Total amount received &= \text{Amount due (excluding Ashish)

&+ \text{Ashish's allotment payment

&+ \text{Ashish's advance

&= Rs.17,400 + Rs.600 + Rs.1,000

&= Rs.19,000

\end{align*

Therefore, the total amount received on allotment was Rs.19,000.

Answer: (B) Rs.19,000 Quick Tip: When shares are paid in installments, ensure to account for any additional payments made by shareholders at different stages.

Question 5:

(b) M Ltd. forfeited 5,000 equity shares of Rs. 10 each issued at a premium of 10% for non-payment of final call of Rs. 2 per share. The minimum amount at which these shares can be reissued as fully paid up will be:

View Solution

Calculate the Called-Up Value per Share:

Face value of each share: Rs.10

Final call not paid: Rs.2

Called-up value per share: Rs.10 - Rs.2 = Rs.8

Calculate the Total Called-Up Value of Forfeited Shares:

Called-up value per share: Rs.8

Number of forfeited shares: 5,000

Total called-up value: Rs.8 5,000 = Rs.40,000

Determine the Minimum Reissue Price:

The minimum reissue price is the amount that has already been called up.

Therefore, the minimum amount at which these shares can be reissued is Rs.8 per share.

Total minimum reissue amount: Rs.8 5,000 = Rs.40,000

Check the Options:

None of the provided options match the calculated minimum reissue amount of Rs.40,000.

However, the question asks for the minimum amount at which the shares can be reissued as fully paid up, meaning the shares are reissued as if the full face value of Rs.10 has been paid.

This means the company can reissue the shares at any price above the amount forfeited.

The amount forfeited is Rs.8 per share, so the minimum reissue price is Rs.8 per share.

Total minimum amount is Rs.8 5000 = Rs.40,000.

Consider the Discount Allowed:

The maximum discount allowed on reissue is the amount forfeited per share, which is Rs.8.

Since the shares are being reissued as fully paid up (Rs.10), the minimum reissue price is Rs.2 per share (Rs.10 - Rs.8).

Total minimum amount: Rs.2 5,000 = Rs.10,000.

Therefore, the minimum amount at which these shares can be reissued as fully paid up is Rs.10,000.

Answer: (B) Rs.10,000 Quick Tip: Accurately track payments made in stages for shares, including any overpayments by shareholders at each phase.

As per the provisions of Companies Act, 2013 Securities Premium cannot be utilized for:

View Solution

Per the Companies Act, 2013, the Securities Premium Account may be employed for:

1. Eliminating preliminary expenses.

2. Clearing discounts on the issuance of shares or debentures.

3. Distributing fully paid bonus shares to shareholders.

4. Repurchasing shares.

It is not permissible to use the Securities Premium Account for the issuance of partly paid bonus shares. Quick Tip: Consult Section 52 of the Companies Act, 2013 to understand the legal uses of the Securities Premium Account.

(a) Which one of the following items is not dealt through Profit and Loss Appropriation Account?

View Solution

The Profit and Loss Appropriation Account is utilized to distribute profits among partners. It records transactions such as interest on capital, interest on drawings, and partner salaries. Conversely, rent paid to a partner is treated as an expense and should be recorded in the Profit and Loss Account, not in the Profit and Loss Appropriation Account. Quick Tip: It's important to distinguish that items related to partner compensation and interest adjustments are accounted for in the Profit and Loss Appropriation Account, whereas rent to a partner is categorized as an expense.

Question 7:

(b) At the time of admission of a partner, the Balance Sheet of the firm showed a workmen compensation reserve of Rs. 80,000. The claim for workmen compensation was estimated at Rs. 1,00,000. The shortfall of Rs. 20,000 will be:

View Solution

The existing workmen compensation reserve amounting to Rs. 80,000 falls short of covering the claim worth Rs. 1,00,000. This deficit of Rs. 20,000 is recorded as a debit in the Revaluation Account, signifying an adjustment to liabilities. Quick Tip: When liabilities surpass reserves during a partner's admission, retirement, or the firm's dissolution, reconcile the difference using the Revaluation Account.

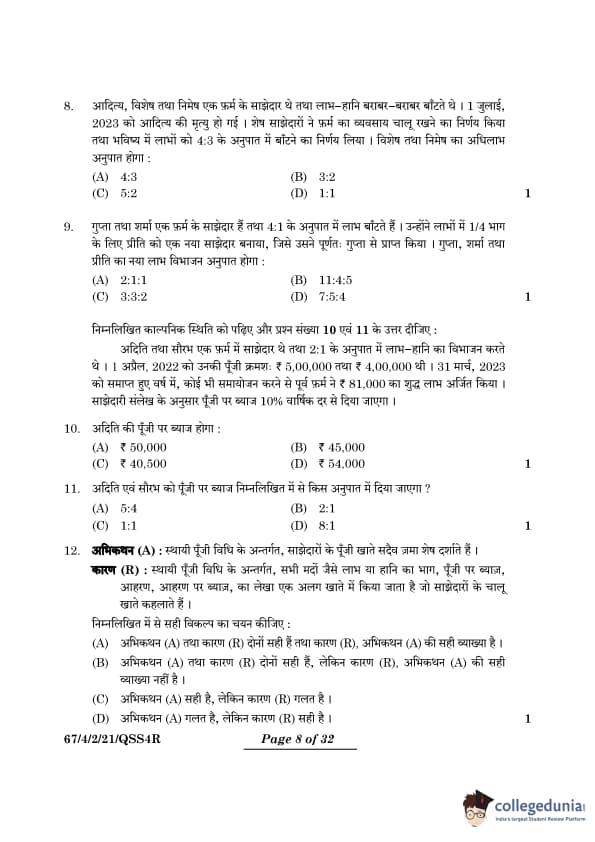

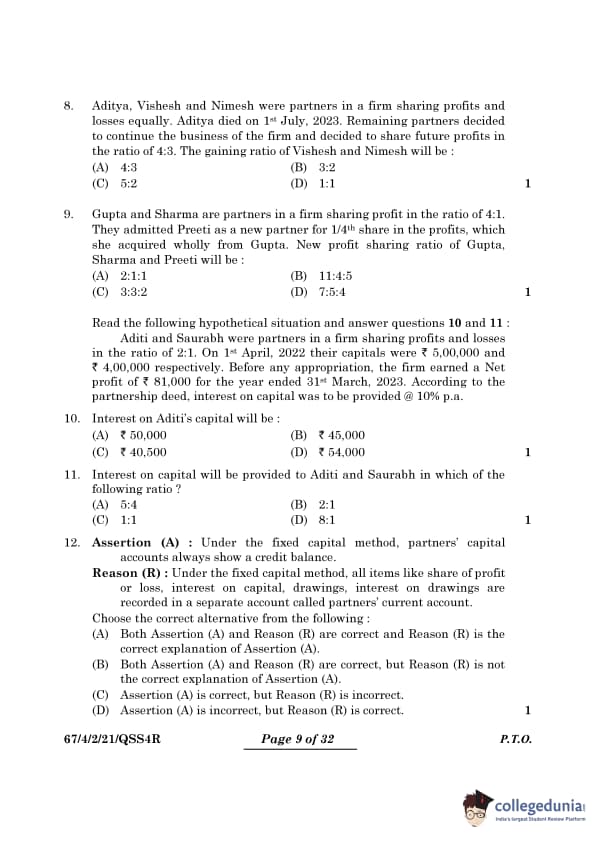

Aditya, Vishesh and Nimesh were partners in a firm sharing profits and losses equally. Aditya died on 1st July, 2023. Remaining partners decided to continue the business of the firm and decided to share future profits in the ratio of 4:3. The gaining ratio of Vishesh and Nimesh will be:

View Solution

Calculate the Initial Share of Each Partner:

Total ratio parts: 1 + 1 + 1 = 3

Each partner's initial share: \(\frac{1}{3}\)

Calculate the New Share of Vishesh and Nimesh:

New profit sharing ratio: 4:3

Total ratio parts: 4 + 3 = 7

Vishesh's new share: \(\frac{4}{7}\)

Nimesh's new share: \(\frac{3}{7}\)

Calculate the Gaining Share of Vishesh:

\begin{align

Vishesh's Gaining Share &= \text{New Share - \text{Old Share

&= \frac{4{7 - \frac{1{3

&= \frac{12 - 7{21

&= \frac{5{21

\end{align

Calculate the Gaining Share of Nimesh:

\begin{align

\text{Nimesh's Gaining Share &= \text{New Share - \text{Old Share

&= \frac{3{7 - \frac{1{3

&= \frac{9 - 7{21

&= \frac{2{21

\end{align

Determine the Gaining Ratio:

Gaining ratio of Vishesh and Nimesh: \(\frac{5{21} : \frac{2}{21}\)

Simplify by multiplying by 21: 5:2

Therefore, the gaining ratio of Vishesh and Nimesh is 5:2.

Answer: (C) 5:2 Quick Tip: Calculate the gaining ratio in cases of partner retirement or death by assessing the shift from old to new profit-sharing ratios of the remaining partners.

Gupta and Sharma are partners in a firm sharing profit in the ratio of 4:1. They admitted Preeti as a new partner for 1/4th share in the profits, which she acquired wholly from Gupta. New profit sharing ratio of Gupta, Sharma and Preeti will be:

View Solution

Preeti acquires a share of \(\frac{1}{4}\), entirely from Gupta.

After the transfer, Gupta's share is reduced to \(4/5 - 1/4 = 11/20\).

Sharma retains his original share of \(1/5 = 4/20\).

Preeti's acquired share is \(\frac{1}{4} = 5/20\).

New profit sharing ratio:

The updated distribution between Gupta, Sharma, and Preeti is \(11:4:5\). Quick Tip: Adjust the profit-sharing ratios appropriately when a new partner joins and takes over a portion of an existing partner’s share.

Read the following hypothetical situation and answer questions 10 and 11:

Aditi and Saurabh were partners in a firm sharing profits and losses in the ratio of 2:1. On 1st April, 2022 their capitals were ₹ 5,00,000 and ₹ 4,00,000 respectively. Before any appropriation, the firm earned a Net profit of ₹ 81,000 for the year ended 31st March, 2023. According to the partnership deed, interest on capital was to be provided @ 10% p.a.

Question 10:

Interest on Aditi's capital will be:

View Solution

Step 1: Formula for Interest on Capital

The formula to calculate interest on capital is: \[ Interest = Capital \times Rate \times Time \]

Given:

- Aditi's Capital = Rs. 5,00,000

- Rate of Interest = 10% per annum

- Time = 1 year

Step 2: Computing the Interest on Capital \[ Interest = 5,00,000 \times \frac{10}{100} \times 1 \] \[ = 50,000 \]

Step 3: Adjusting for Available Profit

Total Net Profit = Rs. 81,000

Total Interest on Capital before adjustment:

- Aditi: Rs. 50,000

- Saurabh: Rs. 40,000 \[ Total Interest = 50,000 + 40,000 = 90,000 \]

Since the available profit (Rs. 81,000) is less than the total interest required (Rs. 90,000), interest must be distributed proportionally.

Step 4: Applying the Proportional Reduction Formula \[ Reduction Factor = \frac{Available Profit}{Total Interest} = \frac{81,000}{90,000} = 0.9 \]

Step 5: Computing Adjusted Interest \[ Adjusted Interest for Aditi = 50,000 \times 0.9 = 45,000 \]

Final Answer: Rs. 45,000 Quick Tip: Interest on capital should be computed based on the starting balance in the partner’s capital account, unless otherwise directed.

Interest on capital will be provided to Aditi and Saurabh in which of the following ratio?

View Solution

Step 1: Using the Interest on Capital Formula

The formula for interest on capital is: \[ Interest = Capital \times Rate \times Time \]

Given:

- Aditi’s capital = Rs. 5,00,000

- Saurabh’s capital = Rs. 4,00,000

- Rate = 10% per annum

- Time = 1 year

Step 2: Calculating Interest for Aditi and Saurabh \[ Interest for Aditi = 5,00,000 \times \frac{10}{100} \times 1 = 50,000 \] \[ Interest for Saurabh = 4,00,000 \times \frac{10}{100} \times 1 = 40,000 \]

Step 3: Finding the Ratio \[ Ratio = \frac{50,000}{40,000} = \frac{5}{4} \]

Thus, the ratio in which interest is provided is 5:4.

Final Answer: 5:4 Quick Tip: Always verify the partnership agreement for specific terms that may modify the standard method of capital distribution.

Assertion (A): Under the fixed capital method, partners' capital accounts always show a credit balance.

Reason (R): Under the fixed capital method, all items like share of profit or loss, interest on capital, drawings, interest on drawings are recorded in a separate account called partners' current account.

Choose the correct alternative from the following:

View Solution

In the fixed capital method, the capital account reflects only the initial contribution by the partners. All other transactions, such as profit, loss, or interest, are recorded separately in the current account. This ensures that the capital account consistently maintains a credit balance. Therefore, both Assertion (A) and Reason (R) are correct, and Reason (R) effectively explains Assertion (A). Quick Tip: The fixed capital method streamlines bookkeeping by distinguishing between capital contributions and operational activities.

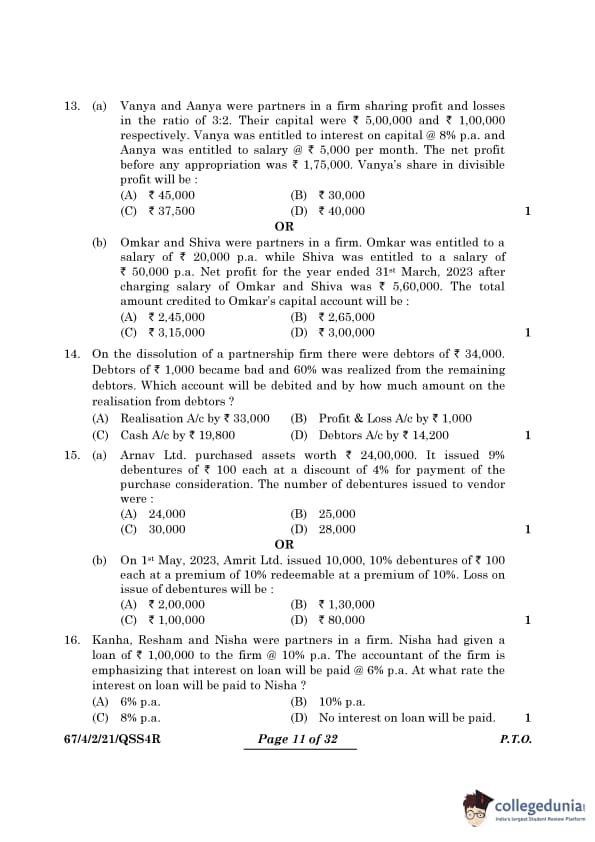

(a) Vanya and Aanya were partners in a firm sharing profit and losses in the ratio of 3:2. Their capital were Rs. 5,00,000 and Rs. 1,00,000 respectively. Vanya was entitled to interest on capital @ 8% p.a. and Aanya was entitled to salary @ Rs. 5,000 per month. The net profit before any appropriation was Rs. 1,75,000. Vanya's share in divisible profit will be:

View Solution

Calculate Vanya's Interest on Capital:

\begin{align*

\text{Vanya's Interest &= \text{Capital \times \text{Rate

&= Rs.5,00,000 \times 8%

&= Rs.40,000

\end{align*

Calculate Aanya's Annual Salary:

\begin{align*

\text{Aanya's Annual Salary &= \text{Monthly Salary \times 12

&= Rs.5,000 \times 12

&= Rs.60,000

\end{align*

Calculate the Total Appropriations:

\begin{align*

\text{Total Appropriations &= \text{Vanya's Interest + \text{Aanya's Salary

&= Rs.40,000 + Rs.60,000

&= Rs.1,00,000

\end{align*

Calculate the Divisible Profit:

\begin{align*

\text{Divisible Profit &= \text{Net Profit - \text{Total Appropriations

&= Rs.1,75,000 - Rs.1,00,000

&= Rs.75,000

\end{align*

Calculate Vanya's Share of Divisible Profit:

\begin{align*

\text{Vanya's Share &= \frac{\text{Vanya's Ratio{\text{Total Ratio \times \text{Divisible Profit

&= \frac{3{3+2 \times Rs.75,000

&= \frac{3{5 \times Rs.75,000

&= Rs.45,000

\end{align*

Therefore, Vanya's share in divisible profit is Rs.45,000.

Answer: (A) Rs.45,000 Quick Tip: Ensure that appropriations, such as interest on capital and partner salaries, are subtracted before allocating the remaining profit to partners.

Question 13:

(b) Omkar and Shiva were partners in a firm. Omkar was entitled to a salary of Rs. 20,000 p.a. while Shiva was entitled to a salary of Rs. 50,000 p.a. Net profit for the year ended 31st March, 2023 after charging salary of Omkar and Shiva was Rs. 5,60,000. The total amount credited to Omkar’s capital account will be:

View Solution

Step 1: Understanding the Given Data

- Omkar’s salary = Rs. 20,000 per annum

- Shiva’s salary = Rs. 50,000 per annum

- Net profit after charging salaries = Rs. 5,60,000

Step 2: Calculating the Total Profit Before Salaries \[ Total Profit = Net Profit + (Omkar’s Salary + Shiva’s Salary) \] \[ = 5,60,000 + (20,000 + 50,000) = 6,30,000 \]

Step 3: Allocating Profit Between Omkar and Shiva

Since the profit-sharing ratio is not mentioned, we assume it is 1:1 (equal sharing). \[ Omkar’s Share = \frac{6,30,000}{2} = 3,00,000 \]

Step 4: Computing Omkar’s Total Credit \[ Omkar’s Total Credit = Salary + Profit Share \] \[ = 20,000 + 2,80,000 = 3,00,000 \]

Final Answer: Rs. 3,00,000 Quick Tip: When calculating profit distribution, include appropriations like salaries before dividing the remaining profit based on the profit-sharing ratio.

On the dissolution of a partnership firm there were debtors of Rs. 34,000. Debtors of Rs. 1,000 became bad and 60% was realized from the remaining debtors. Which account will be debited and by how much amount on the realisation from debtors?

View Solution

Step 1: Determine the realizable amount:

Good debtors = Rs. 34,000 - Rs. 1,000 = Rs. 33,000

Realized amount = 60% of Rs. 33,000 = Rs. 19,800

Step 2: Record the realization entry:

Cash A/c is debited with the realized amount of Rs. 19,800. Quick Tip: First, subtract bad debts from total debtors, then calculate the realizable value as a percentage of the remaining balance.

(a) Arnav Ltd. purchased assets worth Rs. 24,00,000. It issued 9% debentures of Rs. 100 each at a discount of 4% for payment of the purchase consideration. The number of debentures issued to vendor were:

View Solution

Calculate the Discount per Debenture:

\begin{align*

\text{Discount per Debenture &= \text{Face Value \times \text{Discount Rate

&= Rs.100 \times 4%

&= Rs.4

\end{align*

Calculate the Issue Price per Debenture:

\begin{align*

\text{Issue Price per Debenture &= \text{Face Value - \text{Discount per Debenture

&= Rs.100 - Rs.4

&= Rs.96

\end{align*

Calculate the Number of Debentures Issued:

\begin{align*

\text{Number of Debentures &= \frac{\text{Asset Value{\text{Issue Price per Debenture

&= \frac{Rs.24,00,000{Rs.96

&= 25,000

\end{align*

Therefore, the number of debentures issued to the vendor were 25,000.

Answer: (B) 25,000 Quick Tip: When debentures are issued at a discount, deduct the discount from the face value to find the effective issue price.

Question 15:

(b) On 1st May, 2023, Amrit Ltd. issued 10,000, 10% debentures of Rs. 100 each at a premium of 10% redeemable at a premium of 10%. Loss on issue of debentures will be:

View Solution

Step 1: Understanding the Given Data

- Number of Debentures Issued = 10,000

- Face Value of Each Debenture = Rs. 100

- Issue Price of Each Debenture (including 10% premium) = \[ 100 + 10% of 100 = 100 + 10 = Rs. 110 \]

- Redemption Price of Each Debenture (including 10% premium) = \[ 100 + 10% of 100 = 100 + 10 = Rs. 110 \]

Step 2: Computing the Loss on Issue of Debentures

Loss on issue of debentures arises when debentures are redeemed at a premium. It is calculated as: \[ Loss = (Redemption Price - Issue Price) \times Number of Debentures \] \[ = (110 - 100) \times 10,000 \] \[ = 10 \times 10,000 = Rs. 1,00,000 \]

Final Answer: Rs. 1,00,000 Quick Tip: The loss on issue of debentures arises when debentures are redeemed at a premium higher than the premium received during issuance.

Kanha, Resham and Nisha were partners in a firm. Nisha had given a loan of Rs. 1,00,000 to the firm @ 10% p.a. The accountant of the firm is emphasizing that interest on the loan will be paid @ 6% p.a. At what rate the interest on loan will be paid to Nisha?

View Solution

The agreed rate of interest prevails unless there is a specific agreement to change it. Therefore, the interest on the loan will be paid to Nisha at the agreed rate of 10% p.a.

Answer: (B) 10% p.a. Quick Tip: In the absence of a partnership agreement, always rely on the default provisions outlined in the Indian Partnership Act, 1932.

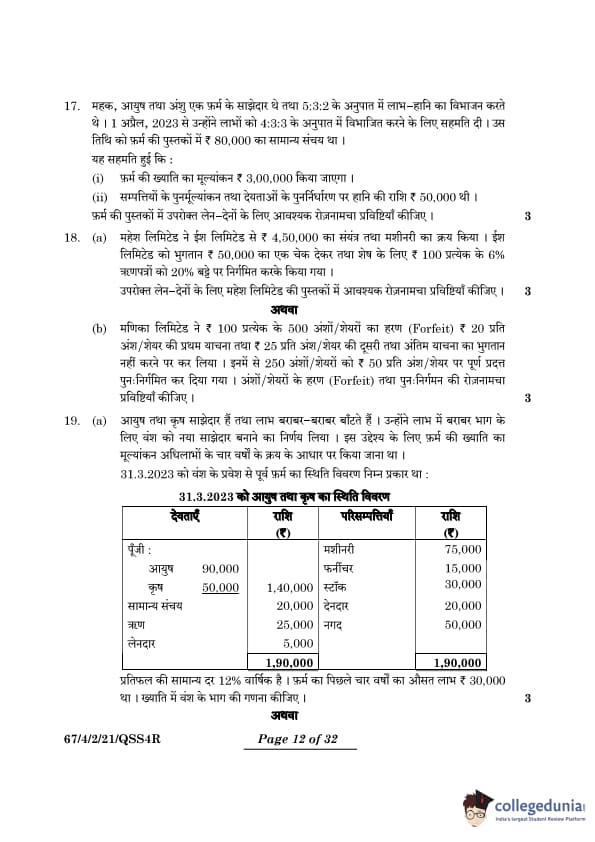

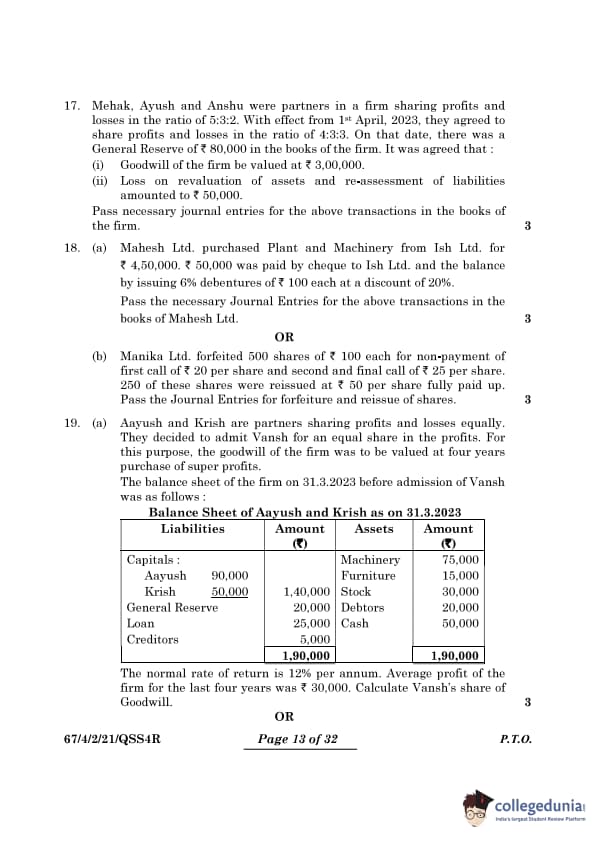

Mehak, Ayush and Anshu were partners in a firm sharing profits and losses in the ratio of 5:3:2. With effect from 1st April, 2023, they agreed to share profits and losses in the ratio of 4:3:3. On that date, there was a General Reserve of Rs. 80,000 in the books of the firm. It was agreed that:

Goodwill of the firm be valued at Rs. 3,00,000.

Loss on revaluation of assets and re-assessment of liabilities amounted to Rs. 50,000.

Pass necessary journal entries for the above transactions in the books of the firm.

View Solution

Journal Entries:

Quick Tip: Reserves and revaluation losses should always be distributed using the old profit-sharing ratio, while goodwill adjustments must be based on the gaining ratio.

(a) Mahesh Ltd. purchased Plant and Machinery from Ish Ltd. for Rs. 4,50,000. Rs. 50,000 was paid by cheque to Ish Ltd. and the balance by issuing 6% debentures of Rs. 100 each at a discount of 20%. Pass the necessary Journal Entries for the above transactions in the books of Mahesh Ltd.

View Solution

Journal Entries:

\begin{tabular{|l|p{8cm|r|r|

\hline

Date & Particulars & Debit (Rs.) & Credit (Rs.)

\hline

1st May, 2023 & Plant and Machinery A/c & 4,50,000 & --

& To Bank A/c & -- & 50,000

& To Ish Ltd. A/c & -- & 4,00,000

& \textit{(Purchase of Plant and Machinery with part payment through cheque) & &

\hline

1st May, 2023 & Ish Ltd. A/c & 4,00,000 & --

& Discount on Issue of Debentures A/c & 1,00,000 & --

& To 6% Debentures A/c & -- & 5,00,000

& \textit{(Settlement of remaining amount by issuing debentures at a 20% discount) & &

\hline

\end{tabular Quick Tip: If debentures are issued at a discount, the amount by which the nominal value exceeds the issue price is classified as a "Discount on Issue of Debentures" and is accounted for as a loss.

Question 18:

(b) Manika Ltd. forfeited 500 shares of Rs. 100 each for non-payment of first call of Rs. 20 per share and second and final call of Rs. 25 per share. 250 of these shares were reissued at Rs. 50 per share fully paid up. Pass the Journal Entries for forfeiture and reissue of shares.

View Solution

Quick Tip: When forfeited shares are reissued at a discount, the forfeited amount is utilized to cover the discount. Any surplus balance from forfeiture is credited to the Capital Reserve account.

(a) Aayush and Krish are partners sharing profits and losses equally. They decided to admit Vansh for an equal share in the profits. For this purpose, the goodwill of the firm was to be valued at four years purchase of super profits.

The balance sheet of the firm on 31.3.2023 before admission of Vansh was as follows:

Balance Sheet of Aayush and Krish as on 31.3.2023

The normal rate of return is 12% per annum. Average profit of the firm for the last four years was Rs. 30,000. Calculate Vansh's share of Goodwill.

View Solution

Step 1: Calculate Capital Employed

\[ Capital Employed = Aayush's Capital + Krish's Capital + General Reserve \]

\[ = 90,000 + 50,000 + 20,000 = 1,60,000 \]

Alternatively,

\[ Capital Employed = Total Assets - External Liabilities (Loan + Creditors) \]

\[ = 1,90,000 - (25,000 + 5,000) = 1,60,000 \]

Step 2: Calculate Normal Profit

\[ Normal Profit = 12% of Capital Employed \]

\[ = \frac{12}{100} \times 1,60,000 = 19,200 \]

Step 3: Calculate Super Profit

\[ Super Profit = Average Profit - Normal Profit \]

\[ = 30,000 - 19,200 = 10,800 \]

Step 4: Calculate Goodwill

\[ Goodwill = Super Profit \times Years of Purchase \]

\[ = 10,800 \times 4 = 43,200 \]

Step 5: Vansh’s Share of Goodwill

Since Vansh is admitted for an equal share, his share in the goodwill will be:

\[ Vansh's Share = \frac{Goodwill}{3} \]

\[ = \frac{43,200}{3} = 14,400 \] Quick Tip: To value goodwill using the super profit method, first calculate normal profit. Subtract it from average profit to find super profit, and then multiply by the years' purchase factor to compute goodwill.

Question 19:

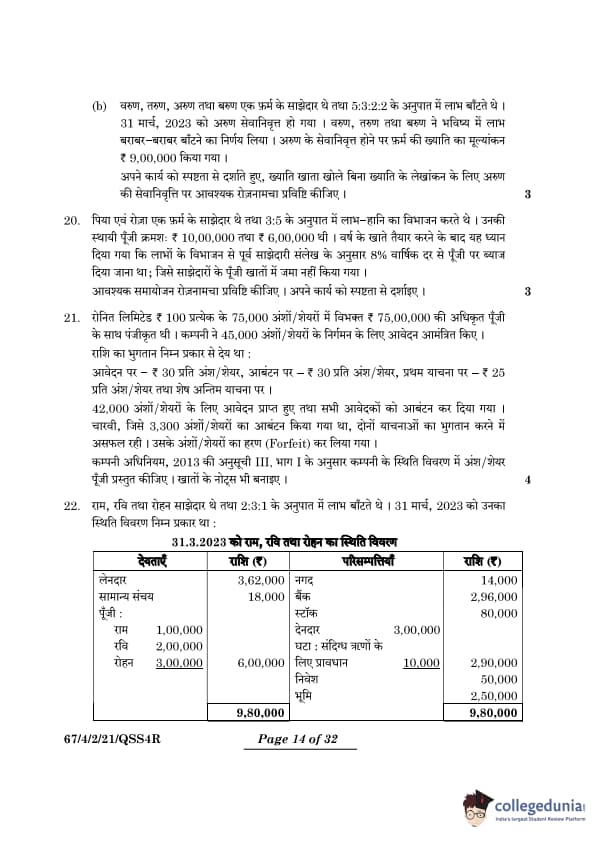

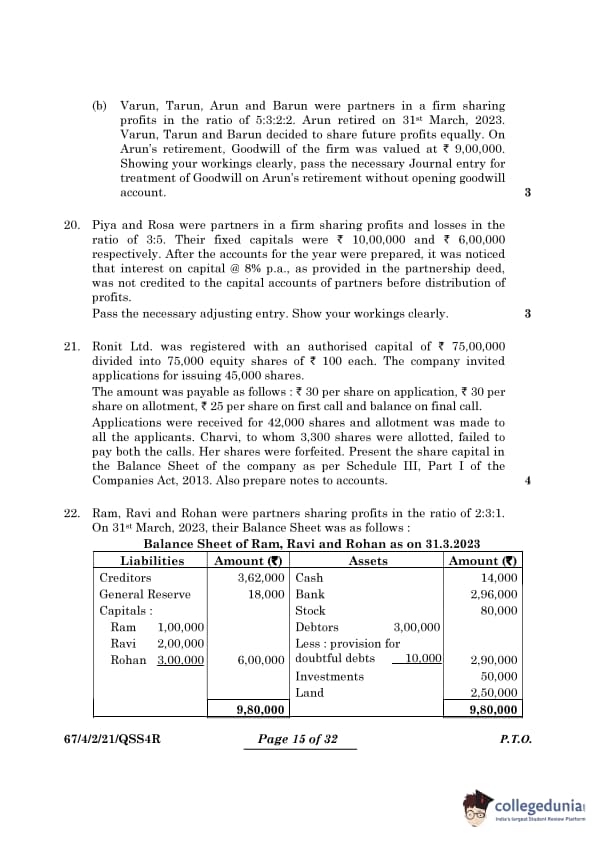

(b) Varun, Tarun, Arun and Barun were partners in a firm sharing profits in the ratio of 5:3:2:2. Arun retired on 31st March, 2023. Varun, Tarun and Barun decided to share future profits equally. On Arun’s retirement, Goodwill of the firm was valued at Rs. 9,00,000. Showing your workings clearly, pass the necessary Journal entry for treatment of Goodwill on Arun’s retirement without opening goodwill account.

View Solution

Quick Tip: When a partner retires, the remaining partners adjust the retiring partner’s share of goodwill in their gaining ratio through their capital accounts.

Piya and Rosa were partners in a firm sharing profits and losses in the ratio of 3:5. Their fixed capitals were Rs. 10,00,000 and Rs. 6,00,000 respectively. After the accounts for the year were prepared, it was noticed that interest on capital @ 8% p.a., as provided in the partnership deed, was not credited to the capital accounts of partners before distribution of profits. Pass the necessary adjusting entry. Show your workings clearly.

View Solution

Quick Tip: When interest on capital is missed, an adjustment is made by debiting the Profit and Loss Adjustment Account and crediting the partners’ capital accounts accordingly.

Ronit Ltd. was registered with an authorised capital of Rs. 75,00,000 divided into 75,000 equity shares of Rs. 100 each. The company invited applications for issuing 45,000 shares.

The amount was payable as follows: Rs. 30 per share on application, Rs. 30 per share on allotment, Rs. 25 per share on first call and balance on final call.

Applications were received for 42,000 shares and allotment was made to all the applicants. Charvi, to whom 3,300 shares were allotted, failed to pay both the calls. Her shares were forfeited. Present the share capital in the Balance Sheet of the company as per Schedule III, Part I of the Companies Act, 2013. Also prepare notes to accounts.

View Solution

Quick Tip: When shares are forfeited, the amount is subtracted from share capital, and securities premium is calculated only on shares issued at a premium.

Ram, Ravi and Rohan were partners sharing profits in the ratio of 2:3:1. On 31st March, 2023, their Balance Sheet was as follows:

Balance Sheet of Ram, Ravi and Rohan as on 31.3.2023

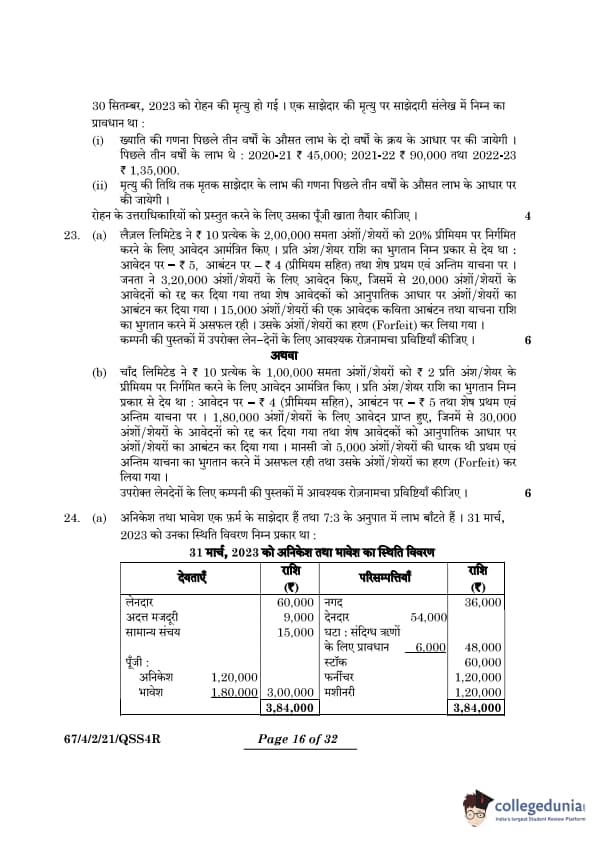

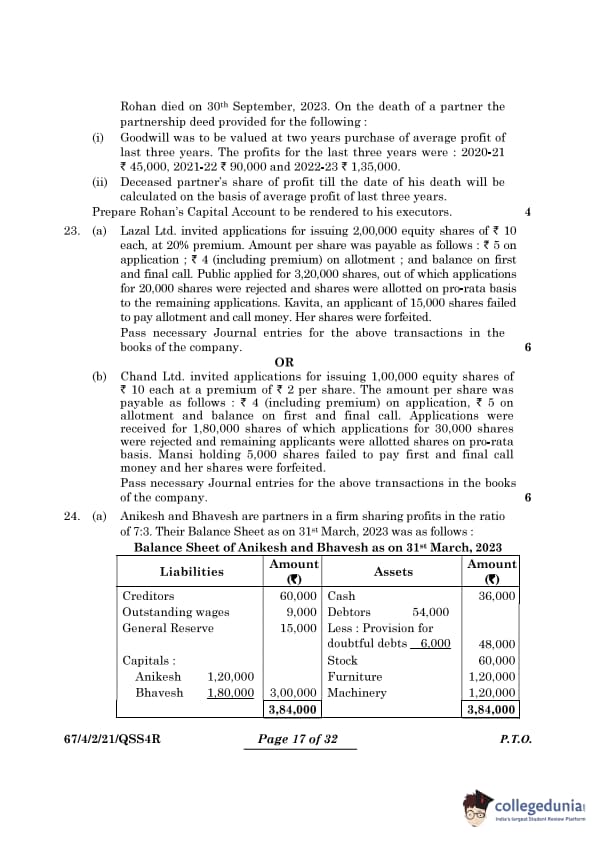

Rohan died on 30th September, 2023. On the death of a partner the partnership deed provided for the following:

(i) Goodwill was to be valued at two years purchase of average profit of last three years. The profits for the last three years were: 2020-21 Rs. 45,000, 2021-22 Rs. 90,000, and 2022-23 Rs. 1,35,000.

(ii) Deceased partner’s share of profit till the date of his death will be calculated on the basis of average profit of last three years.

Prepare Rohan’s Capital Account to be rendered to his executors.

View Solution

% Correct Answer

Rohan’s Capital Account:

\begin{tabular{|l|r|r|

\hline

Date & Particulars & Amount (Rs.)

\hline

1st April, 2023 & Balance b/d & 3,00,000

30th September, 2023 & General Reserve (1/6 share) & 3,000

30th September, 2023 & Goodwill (1/6 share of Rs. 90,000) & 15,000

30th September, 2023 & Profit till date (1/6 of Rs. 67,500) & 11,250

\hline

30th September, 2023 & To Executors A/c & 3,29,250

\hline

Total & & 3,29,250

\hline

\end{tabular

Workings:

Goodwill: Average profit = \( \frac{45,000 + 90,000 + 1,35,000}{3} = 90,000 \)

Goodwill of the firm = \( 90,000 \times 2 = 1,80,000 \)

Rohan's share = \( \frac{1}{6} \times 1,80,000 = 30,000 \).

Profit till death: Average profit = 90,000

Profit up to 30th September = \( 90,000 \times \frac{6}{12} = 45,000 \).

Rohan's share = \( \frac{1}{6} \times 45,000 = 7,500 \). Quick Tip: Distribute goodwill and reserves among partners according to their profit-sharing ratio, and calculate the share of profit for the deceased partner for the period leading to their death.

(a) Lazal Ltd. invited applications for issuing 2,00,000 equity shares of Rs. 10 each, at 20% premium. Amount per share was payable as follows: Rs. 5 on application, Rs. 4 (including premium) on allotment, and balance on first and final call. Public applied for 3,20,000 shares, out of which applications for 20,000 shares were rejected and shares were allotted on pro-rata basis to the remaining applications. Kavita, an applicant of 15,000 shares, failed to pay allotment and call money. Her shares were forfeited. Pass necessary Journal entries for the above transactions in the books of the company.

View Solution

Journal Entries:

\begin{tabular{|l|p{8cm|r|r|

\hline

Date & Particulars & Debit (Rs.) & Credit (Rs.)

\hline

-- & Bank A/c & 16,00,000 & --

& To Share Application A/c & -- & 16,00,000

& \textit{(Receipt of application money for 3,20,000 shares) & &

\hline

-- & Share Application A/c & 16,00,000 & --

& To Share Capital A/c & -- & 10,00,000

& To Share Allotment A/c & -- & 5,00,000

& To Bank A/c & -- & 1,00,000

& \textit{(Adjustment of application money for 2,00,000 shares, refund for 20,000 shares) & &

\hline

-- & Share Allotment A/c & 8,00,000 & --

& To Share Capital A/c & -- & 6,00,000

& To Securities Premium A/c & -- & 2,00,000

& \textit{(Allotment due, including premium) & &

\hline

-- & Bank A/c & 7,40,000 & --

& To Share Allotment A/c & -- & 7,40,000

& \textit{(Receipt of allotment money except for Kavita’s Rs. 60,000) & &

\hline

-- & First and Final Call A/c & 10,00,000 & --

& To Share Capital A/c & -- & 10,00,000

& \textit{(Due for first and final call) & &

\hline

-- & Bank A/c & 9,25,000 & --

& To First and Final Call A/c & -- & 9,25,000

& \textit{(Receipt of first and final call money except for Kavita’s Rs. 75,000) & &

\hline

-- & Share Capital A/c & 90,000 & --

& Securities Premium A/c & 30,000 & --

& To Share Forfeiture A/c & -- & 45,000

& To Calls in Arrears A/c & -- & 75,000

& \textit{(15,000 shares forfeited due to non-payment by Kavita) & &

\hline

\end{tabular Quick Tip: Forfeited shares require adjustments in the share capital, premium, and arrears accounts. Ensure the entries correspond to the unpaid amounts.

Question 23:

(b) Chand Ltd. invited applications for issuing 1,00,000 equity shares of Rs. 10 each at a premium of Rs. 2 per share. The amount per share was payable as follows: Rs. 4 (including premium) on application, Rs. 5 on allotment and balance on first and final call. Applications were received for 1,80,000 shares of which applications for 30,000 shares were rejected and remaining applicants were allotted shares on pro-rata basis. Mansi holding 5,000 shares failed to pay first and final call money and her shares were forfeited. Pass necessary Journal entries for the above transactions in the books of the company.

View Solution

Journal Entries:

\begin{tabular{|l|p{8cm|r|r|

\hline

Date & Particulars & Debit (Rs.) & Credit (Rs.)

\hline

-- & Bank A/c & 7,20,000 & --

& To Share Application A/c & -- & 7,20,000

& \textit{(Receipt of application money for 1,80,000 shares) & &

\hline

-- & Share Application A/c & 7,20,000 & --

& To Share Capital A/c & -- & 4,00,000

& To Share Allotment A/c & -- & 2,80,000

& To Bank A/c & -- & 40,000

& \textit{(Adjustment of application money for 1,00,000 shares, refund for 30,000 shares) & &

\hline

-- & Share Allotment A/c & 5,00,000 & --

& To Share Capital A/c & -- & 5,00,000

& \textit{(Allotment money due) & &

\hline

-- & Bank A/c & 5,00,000 & --

& To Share Allotment A/c & -- & 5,00,000

& \textit{(Receipt of full allotment money) & &

\hline

-- & First and Final Call A/c & 1,00,000 & --

& To Share Capital A/c & -- & 1,00,000

& \textit{(First and final call due) & &

\hline

-- & Bank A/c & 95,000 & --

& To First and Final Call A/c & -- & 95,000

& \textit{(Receipt of first and final call except for Mansi’s Rs. 5,000) & &

\hline

-- & Share Capital A/c & 50,000 & --

& Securities Premium A/c & 10,000 & --

& To Share Forfeiture A/c & -- & 35,000

& To Calls in Arrears A/c & -- & 25,000

& \textit{(5,000 shares forfeited due to Mansi’s non-payment) & &

\hline

\end{tabular Quick Tip: Ensure proper pro-rata adjustments for oversubscription and accurate treatment of forfeited shares when calculating forfeiture amounts.

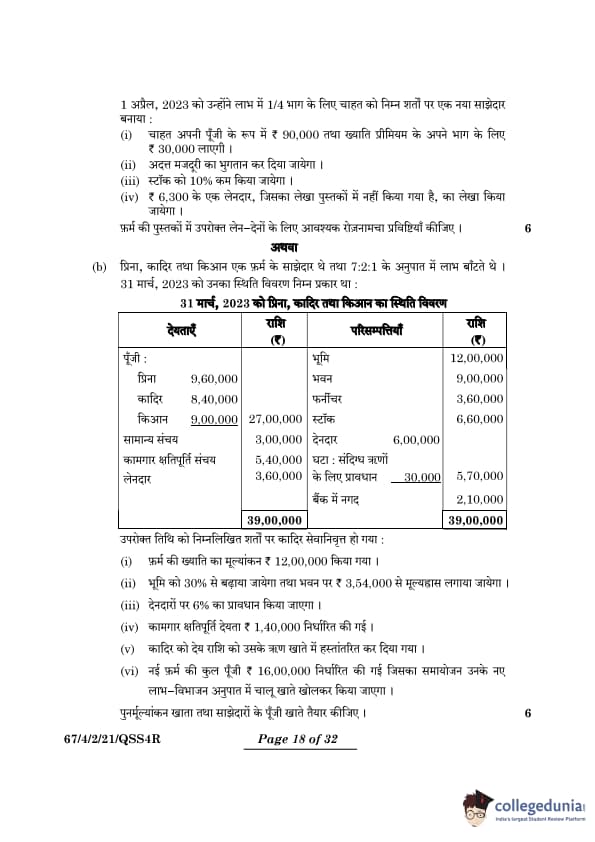

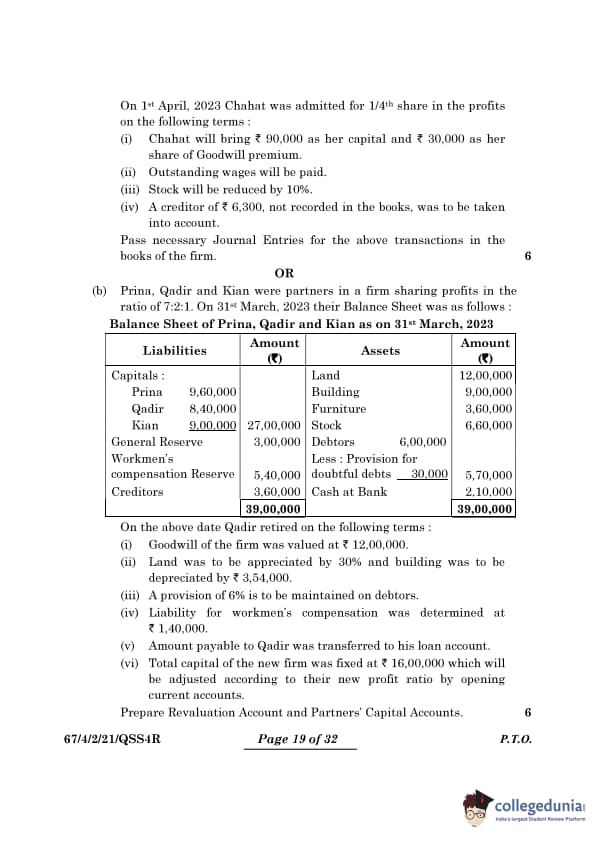

(a) Anikesh and Bhavesh are partners in a firm sharing profits in the ratio of 7:3. Their Balance Sheet as on 31st March, 2023 was as follows:

Balance Sheet of Anikesh and Bhavesh as on 31st March, 2023

Adjustments:

Chahat will bring Rs. 90,000 as her capital and Rs. 30,000 as her share of goodwill premium.

Outstanding wages will be paid.

Stock will be reduced by 10%.

A creditor of Rs. 6,300, not recorded in the books, was to be taken into account.

View Solution

Journal Entries:

\begin{tabular{|l|p{8cm|r|r|

\hline

Date & Particulars & Debit (Rs.) & Credit (Rs.)

\hline

1st April, 2023 & Bank A/c & 90,000 & --

& To Chahat’s Capital A/c & -- & 90,000

& \textit{(Chahat’s capital contribution) & &

\hline

1st April, 2023 & Bank A/c & 30,000 & --

& To Anikesh’s Capital A/c & -- & 21,000

& To Bhavesh’s Capital A/c & -- & 9,000

& \textit{(Goodwill premium contributed by Chahat, credited in the old ratio of 7:3) & &

\hline

1st April, 2023 & Outstanding Wages A/c & 9,000 & --

& To Bank A/c & -- & 9,000

& \textit{(Payment of outstanding wages) & &

\hline

1st April, 2023 & Revaluation A/c & 6,000 & --

& To Stock A/c & -- & 6,000

& \textit{(Reduction in stock by 10%) & &

\hline

1st April, 2023 & Revaluation A/c & 6,300 & --

& To Creditors A/c & -- & 6,300

& \textit{(Recognition of unrecorded creditor) & &

\hline

1st April, 2023 & Anikesh’s Capital A/c & 1,260 & --

& Bhavesh’s Capital A/c & 540 & --

& To Revaluation A/c & -- & 1,800

& \textit{(Transfer of revaluation loss to partners’ capital accounts in the ratio 7:3) & &

\hline

\end{tabular Quick Tip: Before admitting a new partner, adjust for revaluation losses and unrecorded liabilities. Ensure goodwill is allocated among existing partners according to their profit-sharing ratio.

Question 24:

Prina, Qadir and Kian were partners in a firm sharing profits in the ratio of 7:2:1. On 31st March, 2023, their Balance Sheet was as follows:

Balance Sheet of Prina, Qadir and Kian as on 31st March, 2023

Adjustments:

Goodwill of the firm was valued at Rs. 12,00,000.

Land to be appreciated by 30%, and building to be depreciated by Rs. 3,54,000.

A provision of 6% is to be maintained on debtors.

Liability for workmen’s compensation was determined at Rs. 1,40,000.

Amount payable to Qadir was transferred to his loan account.

Prina’s and Kian’s capital to be adjusted in their new profit-sharing ratio.

View Solution

Revaluation Account:

\begin{tabular{|l|r|l|r|

\hline

Particulars & Amount (Rs.) & Particulars & Amount (Rs.)

\hline

To Building A/c (Depreciation) & 3,54,000 & By Land A/c (Appreciation) & 3,60,000

To Provision for Doubtful Debts & 6,000 & &

To Workmen’s Compensation Reserve & 4,00,000 & &

Total & 7,60,000 & Total & 3,60,000

\hline

\end{tabular

Partners’ Capital Accounts:

\begin{tabular{|l|r|r|r|r|

\hline

Particulars & Prina (Rs.) & Qadir (Rs.) & Kian (Rs.) & Total (Rs.)

\hline

Balance b/d & 9,60,000 & 8,40,000 & 9,00,000 & 27,00,000

General Reserve & 2,10,000 & 60,000 & 30,000 & 3,00,000

Goodwill (Adjustment for Qadir) & 7,00,000 & -- & 5,00,000 & 12,00,000

Revaluation Loss & (4,90,000) & (1,40,000) & (70,000) & (7,00,000)

Adjusted Balance & 13,80,000 & -- & 13,60,000 & 27,40,000

\hline

\end{tabular Quick Tip: Any revaluation gains or losses should be allocated among partners according to their previous profit-sharing ratio. Ensure that the retiring partner’s share of goodwill and revaluation is adjusted before making final settlements.

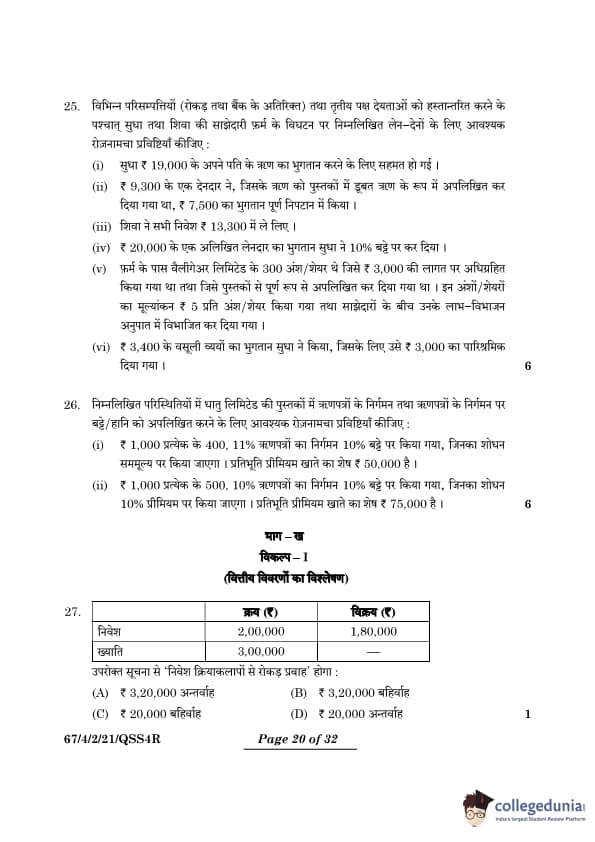

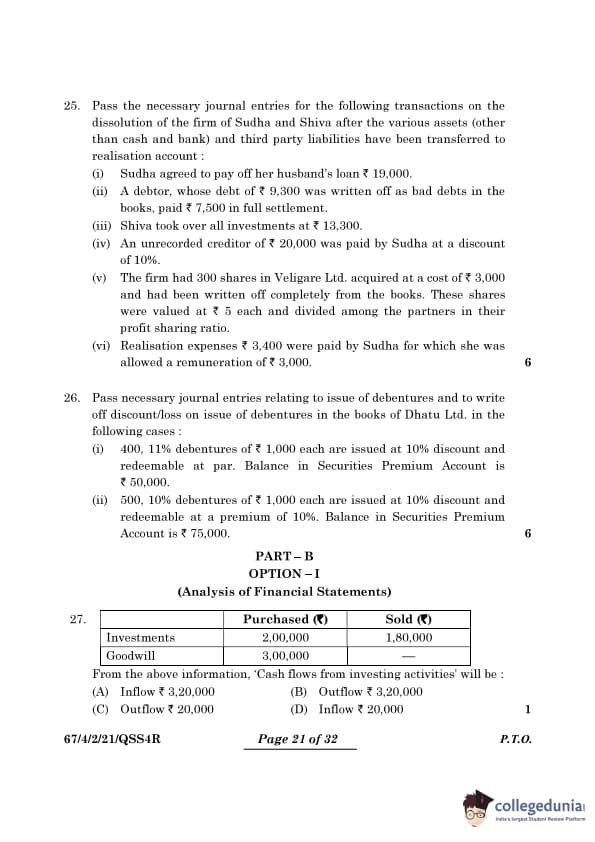

Pass the necessary journal entries for the following transactions on the dissolution of the firm of Sudha and Shiva after the various assets (other than cash and bank) and third-party liabilities have been transferred to realisation account:

Sudha agreed to pay off her husband’s loan Rs. 19,000.

A debtor, whose debt of Rs. 9,300 was written off as bad debts in the books, paid Rs. 7,500 in full settlement.

Shiva took over all investments at Rs. 13,300.

An unrecorded creditor of Rs. 20,000 was paid by Sudha at a discount of 10%.

The firm had 300 shares in Veligare Ltd. acquired at a cost of Rs. 3,000 and had been written off completely from the books. These shares were valued at Rs. 5 each and divided among the partners in their profit-sharing ratio.

Realisation expenses Rs. 3,400 were paid by Sudha for which she was allowed a remuneration of Rs. 3,000.

View Solution

Journal Entries:

\begin{tabular{|l|p{8cm|r|r|

\hline

Date & Particulars & Debit (Rs.) & Credit (Rs.)

\hline

-- & Realisation A/c & 19,000 & --

& To Sudha’s Capital A/c & -- & 19,000

& \textit{(Sudha agrees to settle her husband's loan) & &

\hline

-- & Bank A/c & 7,500 & --

& To Realisation A/c & -- & 7,500

& \textit{(Recovery of bad debt from debtor) & &

\hline

-- & Shiva’s Capital A/c & 13,300 & --

& To Realisation A/c & -- & 13,300

& \textit{(Shiva takes over investments) & &

\hline

-- & Realisation A/c & 18,000 & --

& To Bank A/c & -- & 18,000

& \textit{(Unrecorded creditor of Rs. 20,000 settled at a 10% discount) & &

\hline

-- & Realisation A/c & 1,500 & --

& To Sudha’s Capital A/c & 1,050 & --

& To Shiva’s Capital A/c & 450 & --

& \textit{(Distribution of Veligare Ltd. shares among partners in profit-sharing ratio) & &

\hline

-- & Realisation A/c & 3,400 & --

& To Bank A/c & -- & 3,400

& \textit{(Payment of realization expenses by Sudha) & &

\hline

-- & Realisation A/c & 3,000 & --

& To Sudha’s Capital A/c & -- & 3,000

& \textit{(Remuneration given to Sudha for realization duties) & &

\hline

\end{tabular Quick Tip: During dissolution, all activities like asset realization, liability settlement, and expense payments are recorded through the Realisation Account.

Pass necessary journal entries relating to issue of debentures and to write off discount/loss on issue of debentures in the books of Dhatu Ltd. in the following cases:

(i) 400, 11% debentures of Rs. 1,000 each are issued at 10% discount and redeemable at par. Balance in Securities Premium Account is Rs. 50,000.

(ii) 500, 10% debentures of Rs. 1,000 each are issued at 10% discount and redeemable at a premium of 10%. Balance in Securities Premium Account is Rs. 75,000.

View Solution

Journal Entries:

\begin{tabular{|l|p{8cm|r|r|

\hline

Date & Particulars & Debit (Rs.) & Credit (Rs.)

\hline

-- & Bank A/c & 3,60,000 & --

& Discount on Issue of Debentures A/c & 40,000 & --

& To 11% Debentures A/c & -- & 4,00,000

& \textit{(400 debentures issued at a 10% discount, redeemable at par) & &

\hline

-- & Loss on Issue of Debentures A/c & 40,000 & --

& To Discount on Issue of Debentures A/c & -- & 40,000

& \textit{(Transfer of loss on debentures to the Loss on Issue of Debentures Account) & &

\hline

-- & Bank A/c & 4,50,000 & --

& Discount on Issue of Debentures A/c & 50,000 & --

& To 10% Debentures A/c & -- & 5,00,000

& To Premium on Redemption A/c & -- & 50,000

& \textit{(500 debentures issued at a 10% discount, redeemable at a 10% premium) & &

\hline

-- & Securities Premium A/c & 75,000 & --

& To Loss on Issue of Debentures A/c & -- & 75,000

& \textit{(Adjusting loss against the Securities Premium Account) & &

\hline

\end{tabular Quick Tip: When debentures are issued at a discount and redeemed at a premium, both the discount and premium must be reflected in the Loss on Issue of Debentures Account.

PART B

OPTION I

(Analysis of Financial Statements)

Question 27:

From the above information, ‘Cash flows from investing activities’ will be:

View Solution

To determine the cash flows from investing activities, we account for both the cash outflows for purchases and the cash inflows from sales:

Cash Outflows:

Investments purchased = Rs. 2,00,000

Goodwill purchased = Rs. 3,00,000

Total cash outflow = Rs. 2,00,000 + Rs. 3,00,000 = Rs. 5,00,000

Cash Inflows:

Investments sold = Rs. 1,80,000

Total cash inflow = Rs. 1,80,000

Net Cash Flow: \[ Net cash flow = Cash inflows - Cash outflows = Rs. 1,80,000 - Rs. 5,00,000 = Outflow of Rs. 3,20,000. \] Quick Tip: When calculating cash flows from investing activities, consider all asset purchases as outflows and all asset sales as inflows. The net result will reflect the cash flow from investing activities.

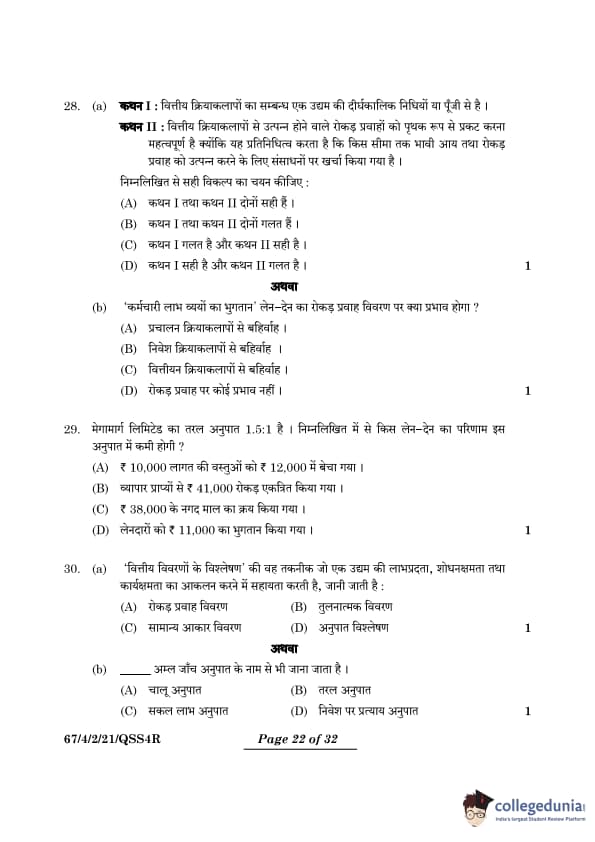

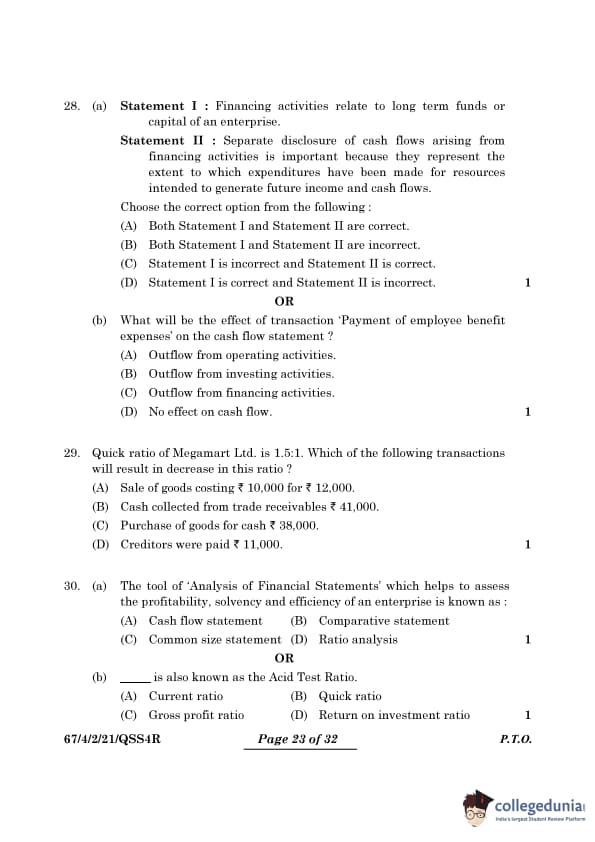

(a) Statement I: Financing activities relate to long-term funds or capital of an enterprise.

Statement II: Separate disclosure of cash flows arising from financing activities is important because they represent the extent to which expenditures have been made for resources intended to generate future income and cash flows.

Choose the correct option from the following:

View Solution

Financing activities refer to the inflow and outflow of funds associated with long-term borrowings or equity-related transactions. Statement II highlights the significance of separately reporting cash flows from financing activities to offer insights into funding sources and resource distribution. Both statements are accurate. Quick Tip: Financing activities encompass raising funds through equity or debt, as well as repaying loans or distributing dividends.

OR

Question 28:

(b) What will be the effect of transaction ‘Payment of employee benefit expenses’ on the cash flow statement?

View Solution

The payment of employee benefit expenses is considered a regular part of business operations. As a result, it is classified as an outflow from operating activities in the cash flow statement. Quick Tip: Operating activities encompass cash flows linked to the core business functions, including both revenue generation and expenses.

Quick ratio of Megamart Ltd. is 1.5:1. Which of the following transactions will result in a decrease in this ratio?

View Solution

The quick ratio is determined by the formula: \[ Quick Ratio = \frac{Quick Assets}{Current Liabilities} \]

When goods are purchased for cash, quick assets (such as cash) decrease, since inventory is not counted as a quick asset. This reduces the numerator, which results in a lower quick ratio. Quick Tip: Quick assets do not include inventories or prepaid expenses. The primary components are cash and receivables.

(a) The tool of ‘Analysis of Financial Statements’ which helps to assess the profitability, solvency and efficiency of an enterprise is known as:

View Solution

Ratio analysis entails calculating different financial ratios to assess a business's profitability, solvency, and operational efficiency. These ratios offer valuable insights into the company’s financial health. Quick Tip: Important ratios include the current ratio, debt-equity ratio, and gross profit ratio, among others.

Question 30:

(b) ...... is also known as the Acid Test Ratio.

View Solution

The quick ratio, often called the Acid Test Ratio, excludes inventory and prepaid expenses, offering a more conservative measure of liquidity. Quick Tip: The quick ratio is calculated as: \[ Quick Ratio = \frac{Quick Assets}{Current Liabilities} \]

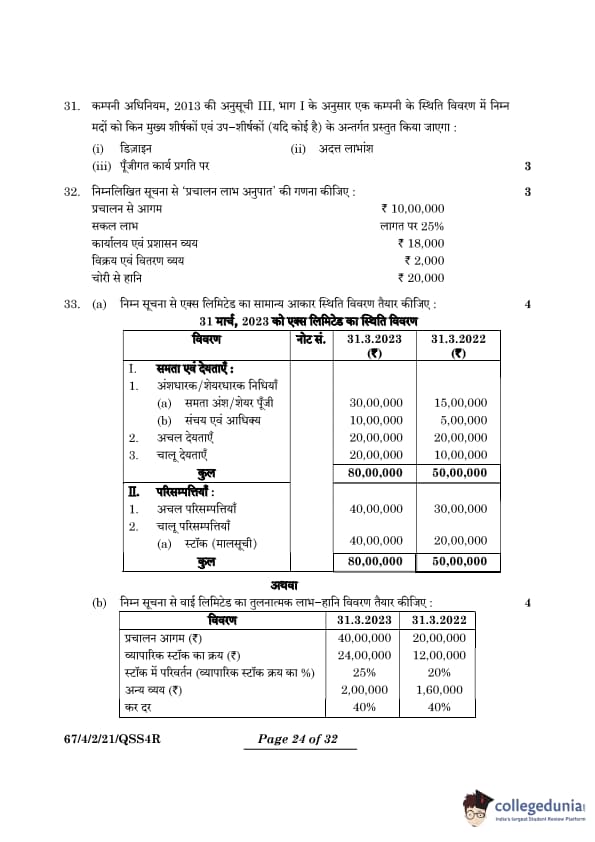

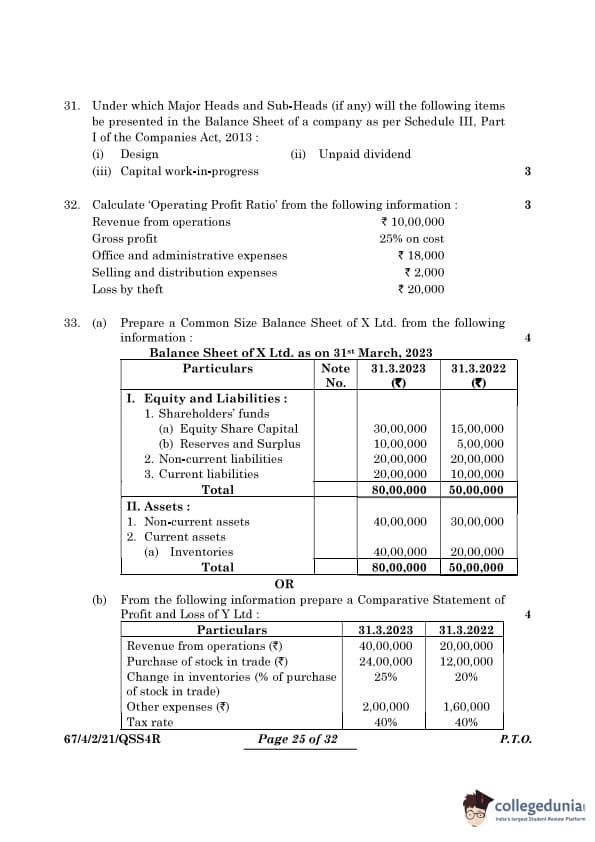

Under which Major Heads and Sub-Heads (if any) will the following items be presented in the Balance Sheet of a company as per Schedule III, Part I of the Companies Act, 2013:

Design

Unpaid dividend

Capital work-in-progress

View Solution

As per Schedule III, Part I of the Companies Act, 2013:

Design: Being an intangible asset, it is classified under \textit{Intangible Assets within the \textit{Non-Current Assets section.

Unpaid Dividend: This is considered a liability and is reported under \textit{Other Current Liabilities in the \textit{Current Liabilities section.

Capital Work-in-Progress: It is listed under \textit{Non-Current Assets, as it represents ongoing capital expenditure. Quick Tip: Always consult Schedule III, Part I of the Companies Act, 2013, for the proper classification and presentation of items in the Balance Sheet.

Calculate ‘Operating Profit Ratio’ from the following information:

Revenue from operations: Rs. 10,00,000

Gross profit: 25% on cost

Office and administrative expenses: Rs. 18,000

Selling and distribution expenses: Rs. 2,000

Loss by theft: Rs. 20,000

View Solution

Step 1: Formula for Operating Profit Ratio

\[ Operating Profit Ratio = \left( \frac{Operating Profit}{Revenue from Operations} \right) \times 100 \]

Step 2: Calculation of Cost of Revenue from Operations

\[ Revenue from Operations = Cost of Revenue from Operations + Gross Profit \]

\[ 10,00,000 = Cost of Revenue from Operations + 25% of Cost of Revenue from Operations \]

\[ Cost of Revenue from Operations = Rs. 8,00,000 \]

Step 3: Calculation of Operating Profit

\[ Operating Profit = Revenue from Operations - Cost of Revenue from Operations - Operating Expenses \]

\[ = 10,00,000 - 8,00,000 - 18,000 - 2,000 \]

\[ = Rs. 1,80,000 \]

(Note: Loss by theft is not an operating expense and is ignored.)

Step 4: Calculation of Operating Profit Ratio

\[ Operating Profit Ratio = \left( \frac{1,80,000}{10,00,000} \right) \times 100 \]

\[ = 18% \]

Correct Answer: (Operating Profit Ratio = 18%) Quick Tip: The Operating Profit Ratio indicates how efficiently a company is managing its core business activities. It excludes non-operating items like income and expenses.

Prepare a Common Size Balance Sheet of X Ltd. from the following information:

Balance Sheet of X Ltd. as on 31st March, 2023

View Solution

N/A Quick Tip: In a common size balance sheet, every item is expressed as a percentage of the total assets or total liabilities, helping to understand their relative significance.

Question 33:

(b) From the following information prepare a Comparative Statement of Profit and Loss of Y Ltd.:

View Solution

N/A Quick Tip: In a comparative statement, calculate the percentage change using the formula: \[ Percentage Change = \frac{Current Year - Previous Year}{Previous Year} \times 100 \]

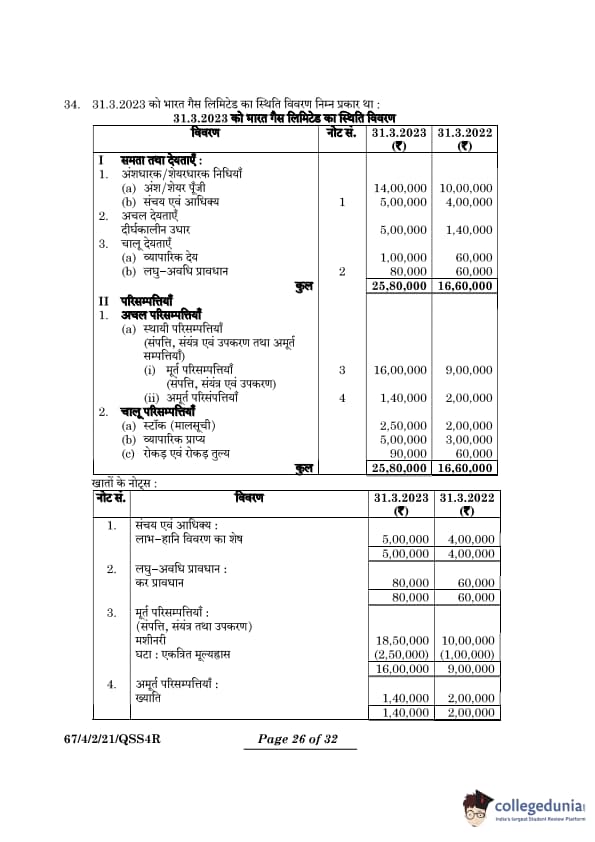

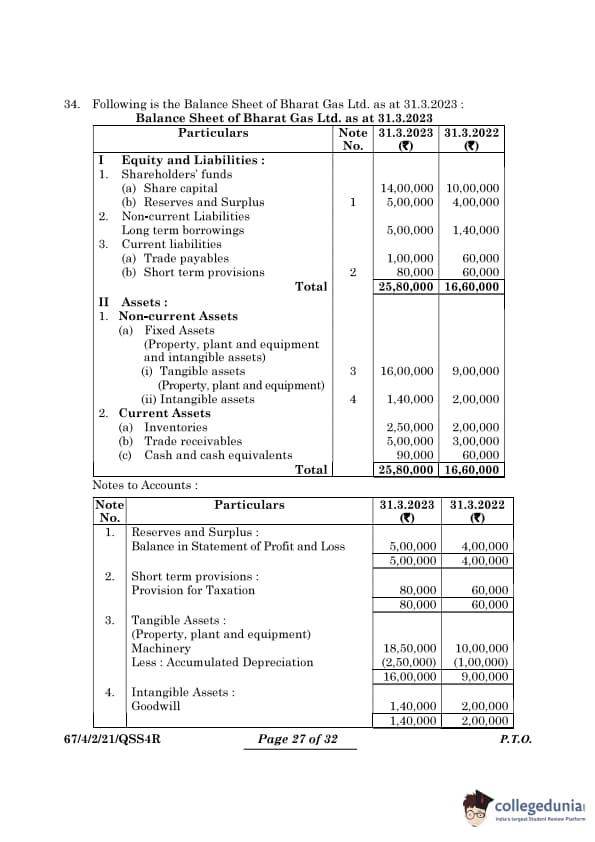

Following is the Balance Sheet of Bharat Gas Ltd. as at 31.3.2023:

Balance Sheet of Bharat Gas Ltd. as at 31.3.2023

Adjustments:

During the year, a machine costing Rs. 3,00,000 on which accumulated depreciation was Rs. 45,000 was sold for Rs. 1,35,000. Calculate ‘Cash Flows from Operating Activities’.

View Solution

N/A Quick Tip: To determine cash flows from operating activities, include adjustments for non-cash items, changes in working capital, and tax provisions.

PART B

OPTION II

(Computerised Accounting)

Question 27:

How are ‘absolute cell references’ and ‘mixed reference’ identified in Excel?

View Solution

In Excel, absolute cell references are denoted by placing a

( sign before both the column and row references (e.g.,

)A

(1). Mixed references, on the other hand, use the

) sign only before either the column or the row reference (e.g.,

(A1 or A

)1). Quick Tip: Absolute references (

(A

)1) lock both the column and row, while mixed references (

(A1 or A

)1) lock only one of them.

(a) Excel considers which of the following group of mathematical operations of equal importance?

View Solution

In Excel, mathematical operations are performed based on the following order of precedence: Parentheses, Exponents, Multiplication/Division (evaluated left to right), and Addition/Subtraction (evaluated left to right). Quick Tip: Use the acronym PEMDAS (Parentheses, Exponents, Multiplication/Division, Addition/Subtraction) to remember the order of operations in Excel.

Question 28:

(b) How many rows are available in Excel 2007?

View Solution

In Excel 2007, the .xls format offers 65,536 rows and 256 columns, while the .xlsx format allows for 1,048,576 rows and 16,384 columns. Quick Tip: The .xlsx format in Excel supports a significantly larger grid compared to the older .xls format.

Which of the following type of software suffers from the limitation of low secrecy level and software being prone to data frauds?

View Solution

Generic software is designed for general use and is not tailored to individual user needs, which makes it more vulnerable to data fraud and privacy concerns due to the absence of customized security features. Quick Tip: Generic software offers less security than customized software, which is specifically developed to meet the needs of particular users or organizations.

(a) ‘A piece of information shown in a graph which is assigned to the data series’ is known as:

View Solution

A legend in a graph is used to describe the different data series represented. It provides labels for the colors, patterns, or symbols used in the chart to differentiate between various data series. Quick Tip: A chart’s data series is made up of multiple data points, each visually representing a piece of data.

Question 30:

(b) ‘LABELS’ in Excel means:

View Solution

In Excel, labels are text, special characters, or descriptive details that help identify rows or columns. Labels cannot be used in mathematical calculations. Quick Tip: Labels enhance clarity in Excel spreadsheets but are not considered numerical values.

How to use ‘Mark Common Formula Error’ in Excel? Explain.

View Solution

The ‘Mark Common Formula Error’ feature in Excel helps pinpoint common formula errors, such as division by zero, invalid cell references, or inconsistent formulas. To use this feature, follow these steps:

Enable Error Checking:

Navigate to File > Options > Formulas and ensure the \textit{Error Checking option is turned on.

Identify Errors:

When an error occurs, Excel will display a small green triangle in the top-left corner of the affected cell.

Review Error Messages:

Hover over the cell to reveal a warning icon. Click on the icon to open a dropdown list of possible errors.

Fix the Error:

Select the appropriate option from the dropdown, such as \textit{Edit in Formula Bar, to correct the error.

Use Formula Auditing Tools:

Go to \textit{Formulas > Formula Auditing to trace the error or evaluate formulas step-by-step. Quick Tip: Common formula errors include \textit{\#DIV/0!, \#REF!, and \#NAME?. Ensure correct references and double-check for typos in your formulas.

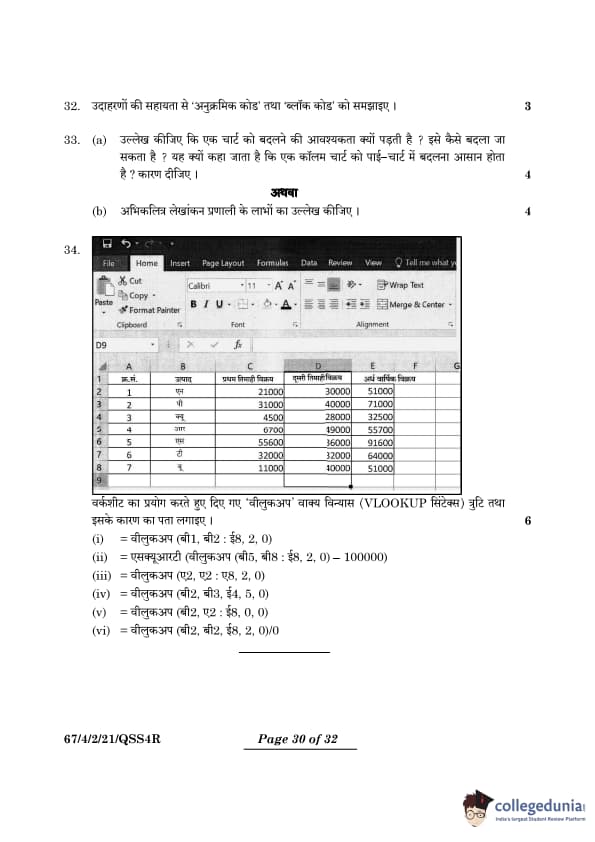

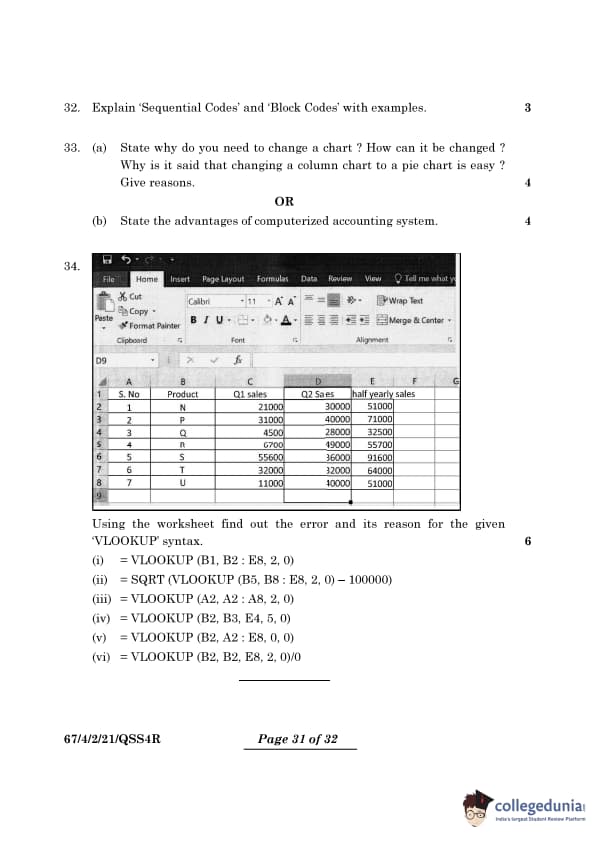

Explain ‘Sequential Codes’ and ‘Block Codes’ with examples.

View Solution

Sequential Codes:

Sequential codes are numbers or identifiers assigned in a consecutive order, ensuring each code is distinct.

Example: Invoice numbers such as 001, 002, 003, or employee IDs like E001, E002, E003.

Advantages:

Simple to understand and implement.

Ideal for maintaining records in a chronological order, like sales invoices or admission forms.

Disadvantages:

Lacks categorization or significance in the codes.

Missing codes can cause confusion or create gaps in records.

Block Codes:

Block codes allocate specific number ranges for distinct categories or groups.

Example: In a library, science books could be assigned codes 100–199, literature books as 200–299, etc.

Advantages:

Simplifies organization and retrieval of information.

Allows flexibility to expand a category's range without affecting others.

Disadvantages:

More complex to implement than sequential codes.

Can lead to underutilized number ranges, causing inefficiency. Quick Tip: Use sequential codes for unique identification and block codes for organizing related items for more efficient classification.

(a) State why do you need to change a chart? How can it be changed? Why is it said that changing a column chart to a pie chart is easy? Give reasons.

View Solution

Why change a chart?

To enhance data visualization and analysis according to the specific objective.

To emphasize different data aspects such as trends, proportions, or relationships.

To make the chart clearer and more visually appealing for the intended audience.

How can a chart be changed?

Select the existing chart.

Right-click and choose \textit{Change Chart Type.

Pick the desired chart type (e.g., Pie Chart, Line Chart, etc.) and confirm by clicking \textit{OK.

Modify chart elements like labels, legends, and colors as needed to align with the new chart type.

Why is it easy to change a column chart to a pie chart?

Both chart types share the same data structure: a single series with categories and values.

Tools like Excel enable effortless conversion between these chart types while maintaining the original data.

Column charts use bars to represent data, whereas pie charts display the same data as segments of a circle to indicate proportions. Quick Tip: Choose chart types based on the data's purpose: Pie charts for showing proportions, column charts for comparisons, and line charts for trends.

Question 33:

(b) State the advantages of a computerized accounting system.

View Solution

A computerized accounting system offers several advantages over traditional manual systems:

Accuracy: Minimizes human errors in calculations and ensures precise financial records.

Efficiency: Accelerates data entry, processing, and the generation of financial statements.

Real-Time Data: Provides immediate access to financial data, enabling timely decision-making.

Integration: Connects various business functions like payroll, inventory, and sales into a cohesive system.

Data Security: Safeguards sensitive financial information using encryption and regular data backups.

Compliance: Eases compliance with tax regulations and laws through automated calculations and reports.

Cost-Effective: Reduces the need for manual bookkeeping, cutting down on time and labor costs.

Scalability: Effectively manages increasing transaction volumes as the business grows.

Customizable Reports: Produces a variety of tailored reports, such as profit and loss statements, balance sheets, and cash flow statements, based on the business's requirements.

Error Detection: Detects discrepancies or inconsistencies in real time, reducing the chances of fraud. Quick Tip: A computerized accounting system is crucial for businesses to improve efficiency, ensure accuracy, and meet modern challenges.

Using the worksheet below, find out the error and its reason for the given ‘VLOOKUP’ syntax:

% VLOOKUP Syntax

(i) = VLOOKUP(B1, B2 : E8, 2, 0)

(ii) = SQRT(VLOOKUP(B5, B8 : E8, 2, 0) - 100000)

(iii) = VLOOKUP(A2, A2 : A8, 2, 0)

(iv) = VLOOKUP(B2, B3 : E4, 5, 0)

(v) = VLOOKUP(B2, A2 : E8, 0, 0)

(vi) = VLOOKUP(B2, B2 : E8, 2, 0)/0

View Solution

\renewcommand{\arraystretch{1.5

\begin{tabular{|p{3cm|p{7cm|p{7cm|

\hline

VLOOKUP Syntax & Error & Reason

\hline

(i) \texttt{=VLOOKUP(B1, B2:E8, 2, 0) & Error: \texttt{\#N/A & The lookup value \texttt{B1 is not found in the first column of the range \texttt{B2:E8. The first column must contain the lookup value.

\hline

(ii) \texttt{=SQRT(VLOOKUP(B5, B8:E8, 2, 0) - 100000) & Error: \texttt{\#N/A & The lookup value \texttt{B5 is missing in the first column of the range \texttt{B8:E8. The lookup value must be in the first column.

\hline

(iii) \texttt{=VLOOKUP(A2, A2:A8, 2, 0) & Error: \texttt{\#VALUE! & The column index (\texttt{2) exceeds the number of columns in the range \texttt{A2:A8, which only has one column.

\hline

(iv) \texttt{=VLOOKUP(B2, B3:E4, 5, 0) & Error: \texttt{\#REF! & The column index (\texttt{5) is invalid since the range \texttt{B3:E4 only contains 2 columns.

\hline

(v) \texttt{=VLOOKUP(B2, A2:E8, 0, 0) & Error: \texttt{\#VALUE! & The column index (\texttt{0) is not valid. It must be a positive integer greater than or equal to \texttt{1.

\hline

(vi) \texttt{=VLOOKUP(B2, B2:E8, 2, 0)/0 & Error: Division by zero & The formula attempts to divide by zero, which results in an undefined operation.

\hline

\end{tabular Quick Tip: \textbf{Quick Tip:} Ensure the lookup value appears in the first column of the table array. The column index should align with the structure of the table array. Avoid division by zero or incorrect references to ranges.

Comments