CBSE Class 12 Accountancy Question Paper 2026 Set-3 (Code: 67/5/3) is now available for download. CBSE conducted the Class 12 Accountancy examination on Feb 24, 2026, from 10:30 AM to 1:30 PM. The question paper consists of 34 questions carrying a total of 80 marks. Part A is compulsory for all candidates. Part B has two options. Candidates have to attempt only one of the given options. Option I : Analysis of Financial Statements and Option II : Computerised Accounting. The Accountancy question paper 2026 was rated moderately difficult by the students.

CBSE Class 12 Accountancy Question Paper 2026 (Set 3- 67/5/3) with Answer Key

Candidates can use the link below to download the CBSE Class 12 Accountancy 2026 Set 3 Question Paper with detailed solutions.

| CBSE Class 12 2026 Accountancy Question Paper Set 3 with Answer Key | Download PDF | Check Solution |

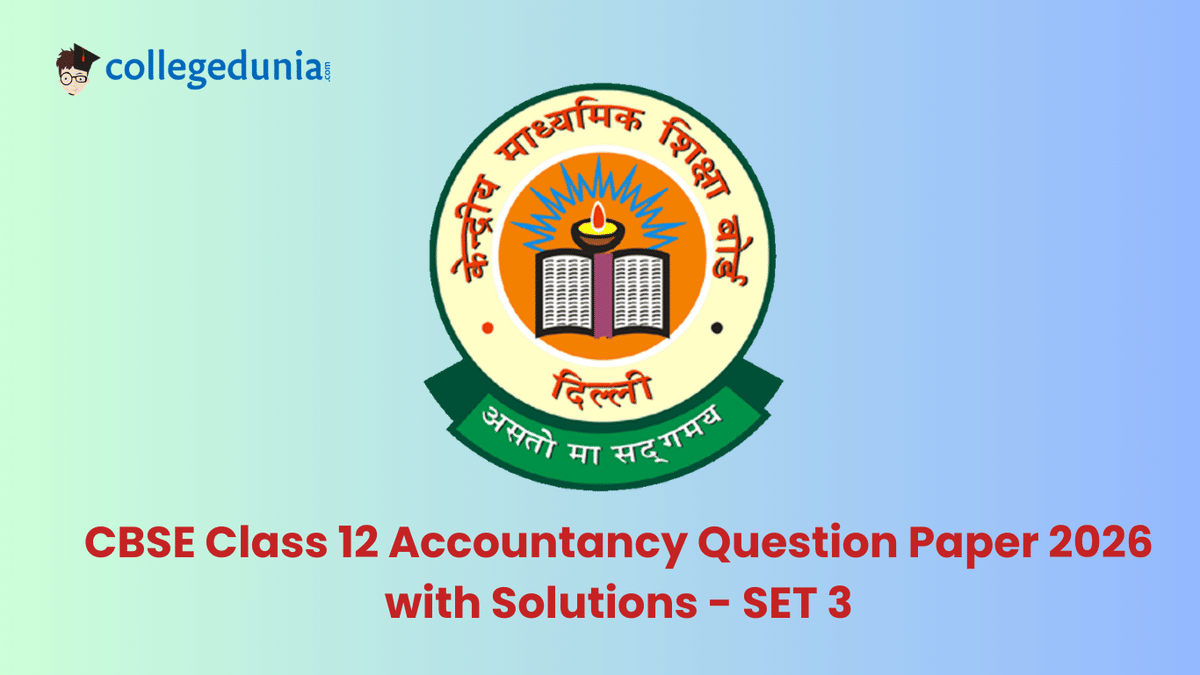

Munna and Sonu were partners in a firm sharing profits and losses in the ratio of 4 : 1. Their fixed capitals were Rs.40,00,000 and Rs.30,00,000 respectively. During the year ended 31st March, 2025, Munna withdrew Rs.50,000 for personal use. Interest on drawings was to be charged @ 6% p.a. The journal entry for charging interest on Munna's drawings will be:

Sujata and Laxmi were partners in a firm sharing profits and losses in the ratio of 2 : 1. On 1st April, 2025, they admitted Raghu as a new partner for 1/5th share in the profits of the firm. On the date of Raghu's admission, it was found that the equipment is undervalued by Rs.90,000. After revaluation, the Balance Sheet of Sujata, Laxmi and Raghu showed equipment at Rs.3,00,000. The value of equipment shown in the books of the firm of Sujata and Laxmi before Raghu's admission was:

Universal Ltd. took over machinery of Rs.3,30,000, furniture of Rs.1,60,000 and liabilities of Rs.80,000 from Amol Ltd. for a purchase consideration of Rs.4,50,000. The payment to Amol Ltd. was made by issue of 10% Debentures of Rs.50 each at a discount of 10%. The number of debentures issued to Amol Ltd. was:

At the time of forfeiture of shares, 'Share Capital Account' is debited with:

Tanay and Ishaan were partners in a firm and their capitals were Rs.4,00,000 and Rs.1,00,000 respectively. Normal rate of return in a similar business was 15% and goodwill of the firm was valued at Rs.1,00,000. If goodwill was calculated at two years purchase of super profits, the average profits of the firm were:

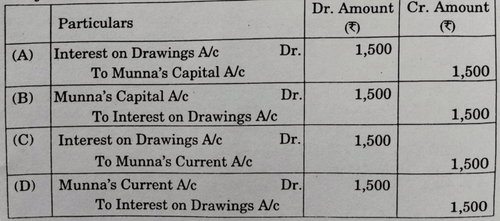

(a) Guru and Prakash were partners in a firm sharing profits and losses in the ratio of 7 : 3. They admitted Anu as a new partner for 1/4th share in the profits of the firm. On the date of Anu's admission, the Profit and Loss Account of Guru and Prakash showed a credit balance of Rs.40,000. The necessary journal entry will be:

OR

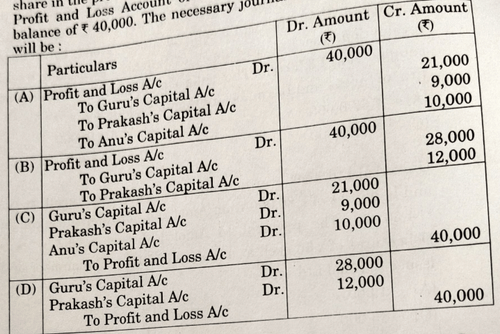

(b) Samta, Mamta and Geeta were partners in a firm sharing profits and losses in the ratio of 11 : 5 : 4. On 31st March, 2025 Samta died. On Samta's death, the goodwill of the firm was valued at Rs.1,80,000. The necessary journal entry for the treatment of goodwill on Samta's death will be:

Sushil and Sapna were partners in a firm sharing profits and losses in the ratio of 3 : 2. On 31st March, 2025, the firm was dissolved. On the date of dissolution there existed a balance of Rs.1,20,000 in sundry creditors account. The sundry creditors were payable after three months. They were paid immediately at a discount of 12% p.a. The amount paid to sundry creditors was:

Anish, Neha and Bindu were partners in a firm sharing profits and losses in the ratio of 4 : 2 : 1. On 1st October, 2024 Anish advanced a loan of Rs.4,00,000 to the firm. In the absence of a partnership agreement, the amount of interest on loan due to Anish on 31st March, 2025 will be:

Arora and Gurmeet were partners in a firm sharing profits and losses in the ratio of 3 : 2. Starting from 1st October, 2024 Arora withdrew Rs.30,000 at the beginning of each quarter for his personal use. Interest on drawings was to be charged @ 12% per annum. Interest on Arora's drawings for the year ended 31st March, 2025 was:

There are two statements Assertion (A) and Reason (R):

Assertion (A): At the time of admission of a new partner in a partnership firm, the newly admitted partner brings an agreed amount of capital either in cash or in kind.

Reason (R): On admission, the new partner gets the right to acquire share in the assets and profits of the partnership firm.

Choose the correct option:

(a) Merak Ltd. forfeited 6,000 equity shares of Rs.10 each for non-payment of final call of Rs.3 per share. The minimum amount per share at which these shares can be reissued will be:

On 1st April, 2024, MM Ltd. issued 4,000, 9% Debentures of Rs.50 each at a premium of 5%, redeemable at a premium of Rs.10 per debenture after five years. Interest on the debentures was to be paid on half-yearly basis on 30th September and 31st March. Interest on debentures for the year ended 31st March, 2025 will be:

(a) Reserve capital is that portion of the \hspace{2cm} capital that can be called only in the event of winding up of the company.

(a) John, Honey and Racob were partners in a firm sharing profits and losses equally. On 31st July, 2025 John died. His share in the profits of the firm from the date of last balance sheet till the date of his death will be:

(a) Sudama, Sharma and Varun were partners in a firm sharing profits and losses in the ratio of 6 : 4 : 3. Sharma retired from the firm on 31st March, 2025. The gaining ratio of Sudama and Varun will be:

Shaurya, Morya and Gaurav were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. On 31st March, 2025, Shaurya retired. The balance in his capital account after making the necessary adjustments on account of reserves and revaluation of assets and reassessment of liabilities was Rs.3,20,000. Shaurya was paid Rs.3,90,000 in full settlement of his claim. The value of goodwill of the firm on the date of Shaurya's retirement was:

Namita, Narendra and Kunwar were partners in a firm sharing profits and losses in the ratio of 3 : 1 : 1. The firm closes its books on 31st March every year. Kunwar died on 30th September, 2025. His share in the profits of the firm from 1st April, 2025 to 30th September, 2025 was calculated as per the provisions of the partnership deed which amounted to Rs.15,600. On the date of Kunwar's death, the Balance Sheet of the firm showed General Reserve of Rs.40,000 and Profit and Loss Account (Dr.) Rs.80,000. Pass necessary journal entries on Kunwar's death in the books of the firm.

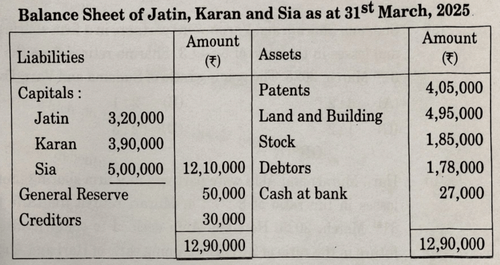

Jatin, Karan and Sia were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. On 31st March, 2025, their Balance Sheet was as follows:

on the above date on the following terms:

(i) Goodwill of the firm was valued at Rs.3,00,000 and the same was to be treated without opening goodwill account.

(ii) Revaluation of assets and reassessment of liabilities resulted in a loss of Rs.75,000.

(iii) Amount payable to Jatin was transferred to his loan account.

Pass necessary journal entries for goodwill, general reserve and revaluation of assets and reassessment of liabilities on Jatin's retirement.

(a) Kiara Ltd. purchased assets worth Rs.12,40,000 and took over liabilities of Rs.3,40,000 of Amrex Ltd. for a purchase consideration of Rs.11,00,000. Kiara Ltd. paid half the amount by cheque. The balance amount was settled by issuing 9% debentures of Rs.100 each at a premium of 10%. Pass necessary journal entries for the above transactions in the books of Kiara Ltd.

(b) On 1st April, 2024, Zara Ltd. issued 8,000, 9% Debentures of Rs.100 each at a discount of 10%. The company had a balance of Rs.50,000 in the Securities Premium Account on the same date. Pass necessary journal entries for the issue of debentures and to write off discount on issue of debentures.

Diksha, Raj and Amit were partners in a firm sharing profits and losses in the ratio of 6 : 3 : 1. On 1st April, 2025 Amit retired. On the date of Amit's retirement, there existed a balance of Rs.90,000 in Workmen's Compensation Fund. Pass the necessary journal entries for treatment of Workmen's Compensation Fund on Amit's retirement in each of the following cases:

(i) Claim on account of Workmen's Compensation was estimated at Rs.1,00,000.

(ii) Claim on account of Workmen's Compensation was estimated at Rs.70,000.

\ (iii) Claim on account of Workmen's Compensation was estimated at Rs.90,000.

Pass necessary journal entries for issue of debentures for the following transactions:

(i) KL Ltd. issued 80,000, 9% Debentures of Rs.100 each at a premium of 10%, redeemable at a premium of 5%.

(ii) UH Ltd. issued 40,000, 9% Debentures of Rs.100 each at par, redeemable at a premium of 10%.

Jain and Gupta were partners in a firm sharing profits and losses in the ratio of 3 : 1. On 1st April, 2024, Agarwal was admitted as a new partner for 1/5th share in the profits of the firm with a minimum guaranteed amount of Rs.75,000. Any deficiency arising out of this account will be borne by Jain and Gupta in the ratio of 1 : 3. During the year ended 31st March, 2025, the firm earned a net profit of Rs.3,00,000. Prepare Profit and Loss Appropriation Account of Jain, Gupta and Agarwal for the year ended 31st March, 2025.

Annu, Bandhu, Sheelu and Golu were partners in a firm sharing profits and losses in the ratio of 4 : 3 : 2 : 1. On 1st April, 2025, they decided to share the future profits equally. For this purpose the goodwill of the firm was valued at Rs.4,00,000. Calculate gain or sacrifice of the partners on change in profit sharing ratio and pass a single adjustment journal entry for the treatment of goodwill.

Ajanta Ltd. invited applications for issuing 30,000 equity shares of Rs.10 each at a premium of Rs.5 per share. The amount was payable as follows: On Application and Allotment – Rs.10 per share (including premium); On first and final call – Balance. Applications for 50,000 shares were received. Applications for 10,000 shares were rejected and their application money was refunded. Pro-rata allotment was made to the remaining applicants. Excess money received with application was adjusted towards sums due on first and final call. Sonu, an applicant of 4,000 shares, paid his entire share money with application. Vedika, to whom 300 shares were allotted, failed to pay the first and final call. After giving her the mandatory notice, her shares were forfeited. Pass necessary journal entries for the above transactions in the books of Ajanta Ltd.

Rao Ltd. forfeited 750 equity shares of Rs.10 each for non-payment of first call of Rs.3 per share (including premium of Rs.1 per share). The second and final call of Rs.3 per share was not yet made. Of the forfeited shares, 500 were re-issued for Rs.2,500, Rs.7 per share paid-up. Pass necessary journal entries for the above transactions in the books of Rao Ltd.

Lily Ltd. forfeited 2,000 equity shares of Rs.10 each for non-payment of first and final call of Rs.2 per share. 750 of the forfeited shares were reissued to Ashok for Rs.10,000 as fully paid-up. The remaining shares were reissued to Sudha at Rs.9 per share fully paid-up. Pass necessary journal entries for the above transactions in the books of Lily Ltd.

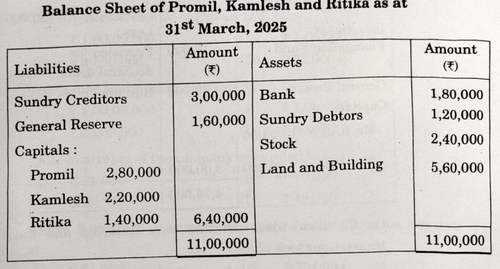

Promil, Kamlesh and Ritika were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. From 1st April, 2025 they decided to share future profits in the ratio of 2 : 3 : 5. On 31st March, 2025, their Balance Sheet was as follows:

It was agreed that: (i) Land and Building will be valued at Rs.6,62,000. (ii) A provision of 5% on debtors will be made for bad and doubtful debts. (iii) Goodwill of the firm will be valued at Rs.1,80,000 and the same will be treated without opening goodwill account. (iv) The value of stock will be reduced to Rs.2,00,000. Showing your working clearly, pass necessary journal entries for the above transactions in the books of the firm.

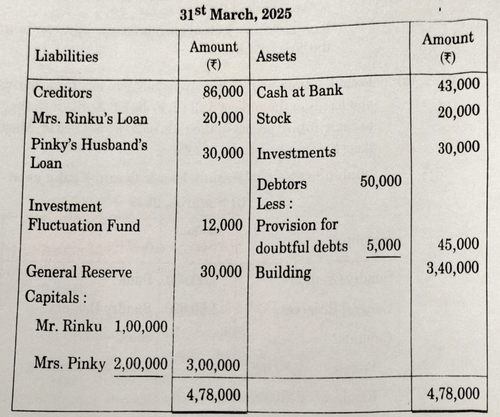

Mr. Rinku and Mrs. Pinky were partners in a firm sharing profits and losses in the ratio of 3 : 2. On 31st March, 2025, their balance sheet was as follows:

On the above date the firm was dissolved:

(i) Mr. Rinku agreed to pay Mrs. Rinku's loan and took away stock for Rs.16,000. (ii) Mrs. Pinky took half of the investments at 10% less. Debtors realised Rs.44,000, Building realised Rs.4,00,000, Creditors were paid Rs.5,000 less and the remaining investments were sold for Rs.19,000. An old furniture not recorded in the books was taken over by Mrs. Pinky for Rs.18,000. Realisation expenses amounted to Rs.6,000. Prepare Realisation Account.

Diwan Ltd. was registered with an authorised capital of Rs.1,00,00,000, divided into 1,00,000 equity shares of Rs.100 each. The company invited applications for issuing 50,000 shares. The amount was payable as follows:

On Application and Allotment – Rs.30 per share

On First call – Rs.40 per share

On Second and Final call – balance

The issue was fully subscribed. All amounts were duly received except from Nawal, a shareholder holding 700 shares, who failed to pay the second and final call. His shares were forfeited.

On the basis of the above information, answer the following questions:

(i) The Registered capital of Diwan Ltd. is:

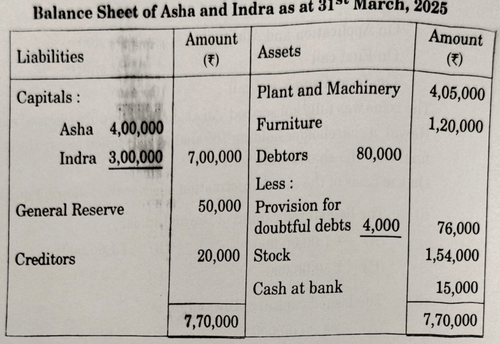

Asha and Indra were partners in a firm sharing profits and losses in the ratio of 3 : 2. Their Balance Sheet on 31st March, 2025 was as following:

On 1st April, 2025, Suraj was admitted for 1/4th share in the profits of the firm on the following terms:

(i) Suraj will bring capital proportionate to his share in the profits of the firm.

(ii) Goodwill of the firm was valued at Rs.1,00,000 and Suraj will bring his share of goodwill premium in cash.

(iii) Furniture was taken over by Asha at Rs.1,00,000.

(iv) A liability of Rs.5,000 included in creditors was not likely to arise.

(v) Plant and Machinery was revalued at Rs.4,35,000. Prepare Revaluation Account and Partners' capital accounts on Suraj's admission.

Show the calculation of proportionate capital clearly.

Statement I: In case of non-financial enterprises, payment of interest and dividend are classified as financing activities.

Statement II: In case of financial enterprises, payment of interest and dividend are classified as investing activities.

Choose the correct option:

During the year ended 31st March, 2025, H.P. Ltd. paid an interim dividend of Rs.50,00,000. From the following, choose the correct option for the purpose of preparing 'Cash Flow Statement':

Which of the following is a financing activity for the purpose of preparing a Cash Flow Statement?

The following information is obtained from the books of Devdutt Ltd.:

Working capital – Rs.4,00,000

Trade Payables – Rs.50,000

Other Current liabilities – Rs.1,00,000

Current assets of Devdutt Ltd. are:

(a) From the following information obtained from the books of accounts of Ananda Ltd., calculate 'Quick Ratio' of the company: Total Current Assets (including stock and prepaid expenses) Rs.2,00,000; Stock Rs.20,000; Prepaid expenses Rs.10,000; Current liabilities Rs.1,70,000.

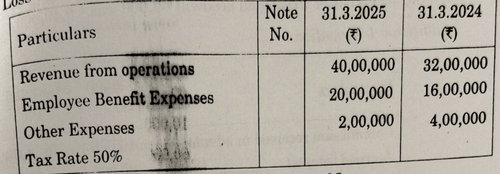

The following information was extracted from the Statement of Profit and Loss of Chaman Ltd. for the year ended 31st March, 2025:

Prepare a Comparative Statement of Profit and Loss.

Under which major head and sub-heads (if any) will the following items be presented in the Balance Sheet of a company as per Schedule III, Part I of the Companies Act, 2013? (i) Demand deposits with banks (ii) Long-term loans (iii) Livestock

'Net Asset Turnover' ratio of a company is 2 times. State with reason whether the following transactions will increase, decrease or not affect the ratio: (i) Cash sales Rs.3,00,000 (ii) Issue of equity shares Rs.10,00,000 (iii) Issue of 9% debentures Rs.5,00,000 (iv) Credit purchase of goods Rs.50,000.

From the following information, calculate 'Proprietary Ratio' and 'Debt-to-Equity Ratio': Equity Share Capital Rs.3,00,000; Preference Share Capital Rs.1,00,000; Reserves and Surplus Rs.1,00,000; Plant and Machinery Rs.3,50,000; Non-Current Investments Rs.1,00,000; Current Assets Rs.2,00,000; Long-term Borrowings Rs.1,50,000.

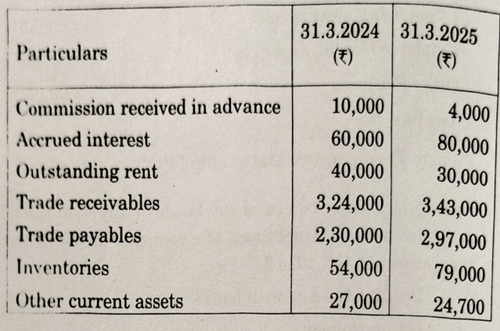

From the following information obtained from the books of 'Sawera Ltd.', calculate Cash from Operations:

Net Profit for the year ended 31st March, 2025 after charging depreciation of Rs.80,000 and after writing off goodwill Rs.2,000 was Rs.5,40,000.

How is navigation conducted from the first to the last cell in a cluster of data in a column by skipping all the cells in between?

(a) Which of the following is not a feature of Tailored accounting software?

Comments