UP Board Class 12 Accountancy Question Paper 2023 with Answer Key Code 349 is available for download. The exam was conducted by the Uttar Pradesh Madhyamik Shiksha Parishad (UPMSP) on February 20, 2023 in Morning Session 8 AM to 11:15 AM. The medium of paper was English and Hindi. The question paper comprised a total of 30 questions.

UP Board Class 12 Accountancy (Code 349) Question Paper 2023 with Solutions PDF

| UP Board Class 12 Accountancy Question Paper with Solutions PDF | Check Solutions |

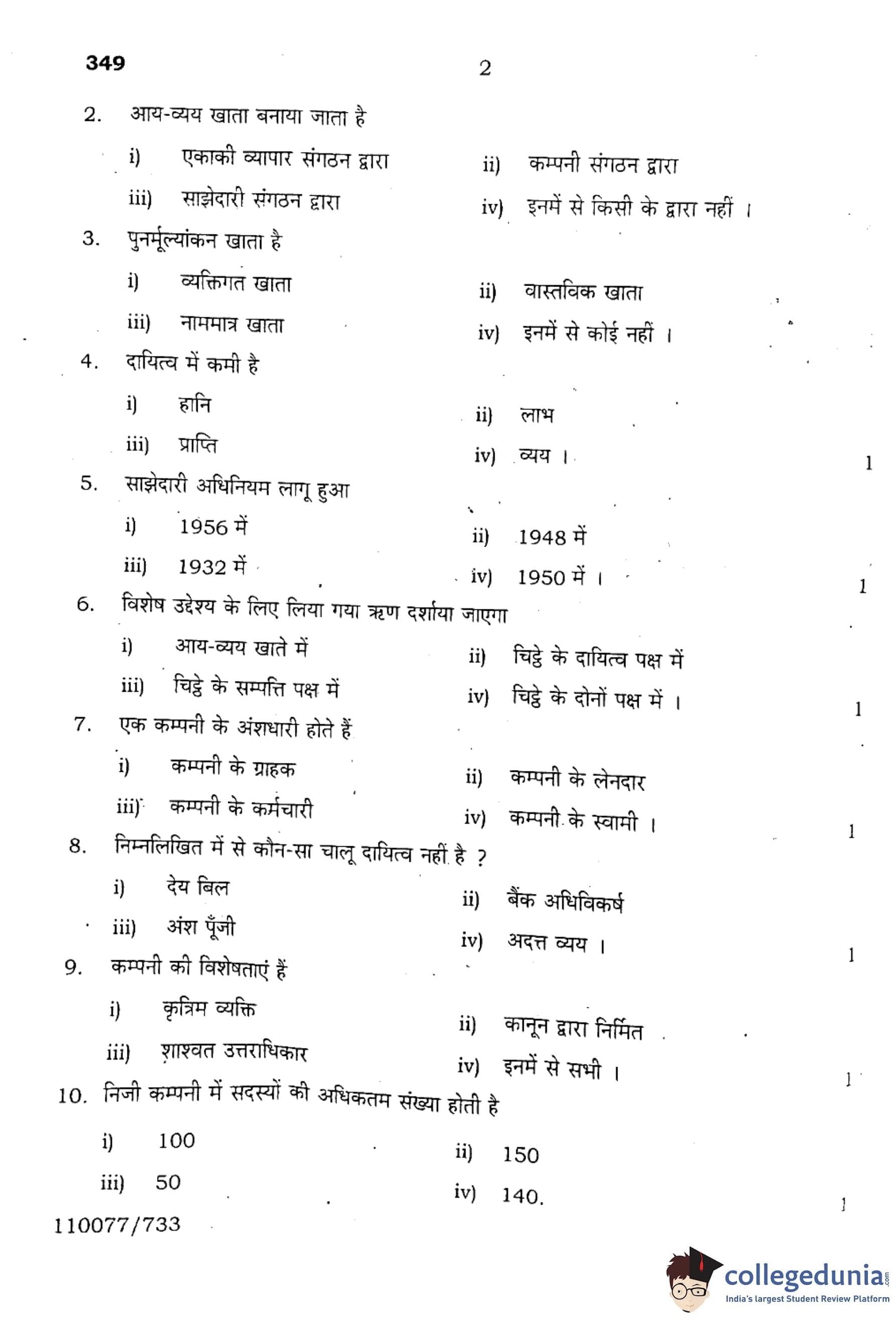

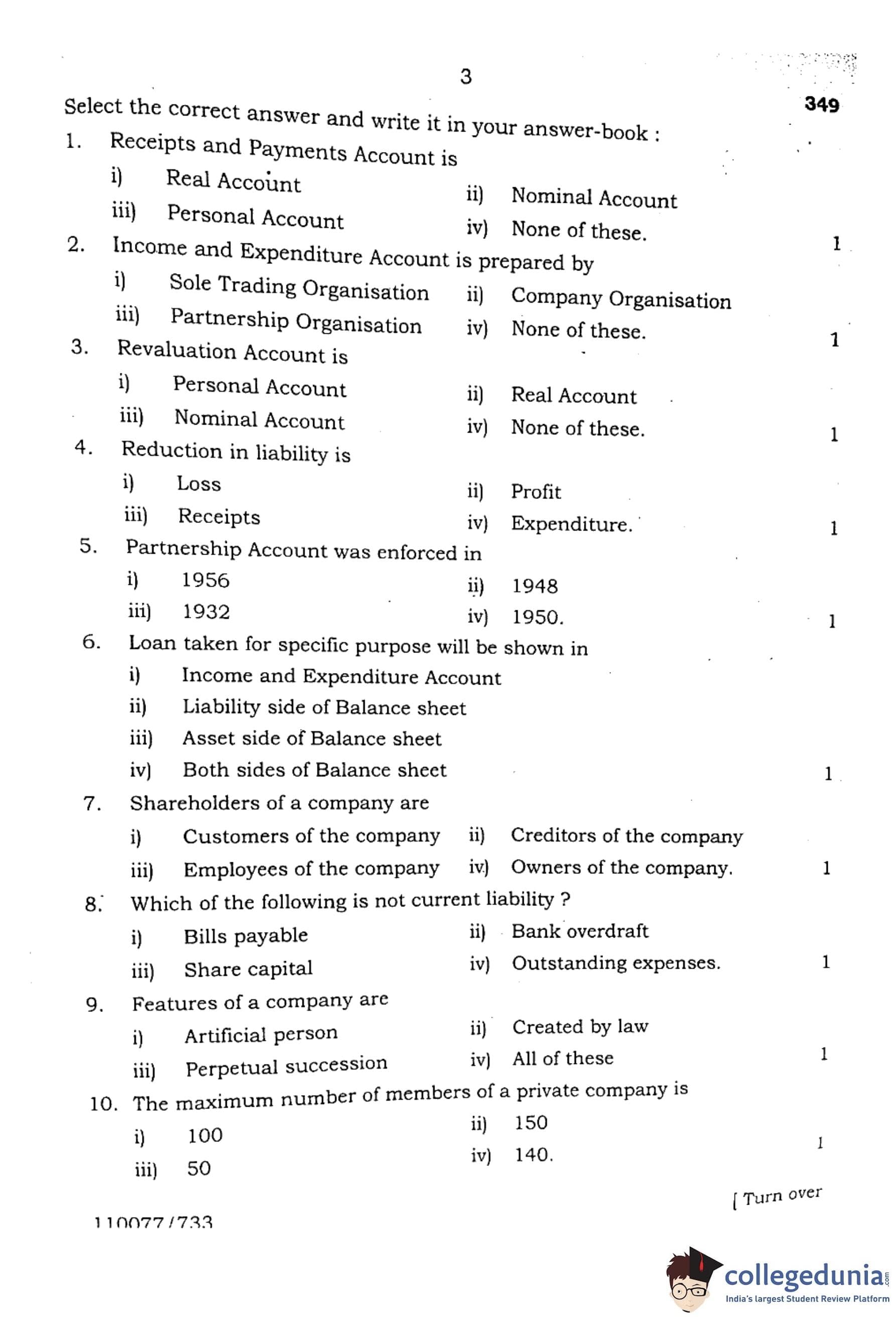

Receipts and Payments Account is

Income and Expenditure Account is prepared by

Revaluation Account is

Reduction in liability is

Partnership Account was enforced in

Loan taken for specific purpose will be shown in

Shareholders of a company are

Which of the following is not a current liability?

Features of a company are

The maximum number of members of a private company is

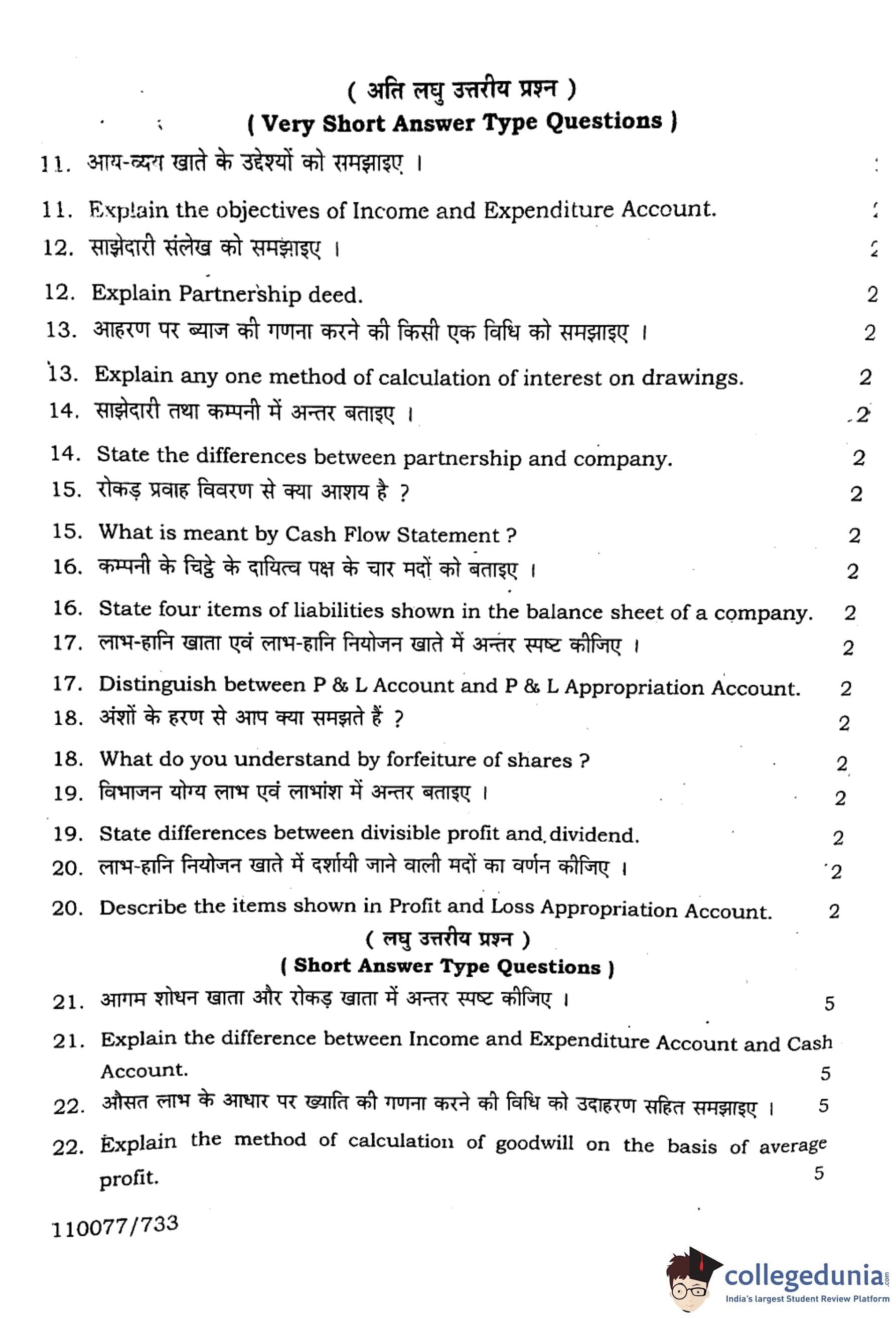

Explain the objectives of Income and Expenditure Account.

Explain Partnership Deed.

Explain any one method of calculation of interest on drawings.

State the differences between partnership and company.

What is meant by Cash Flow Statement?

State four items of liabilities shown in the balance sheet of a company.

Distinguish between P \& L Account and P \& L Appropriation Account.

What do you understand by forfeiture of shares?

State differences between divisible profit and dividend.

Describe the items shown in Profit and Loss Appropriation Account.

Explain the difference between Income and Expenditure Account and Cash Account.

Explain the method of calculation of goodwill on the basis of average profit.

Discuss the types of preference shares.

Describe the significance of analysis of financial statements.

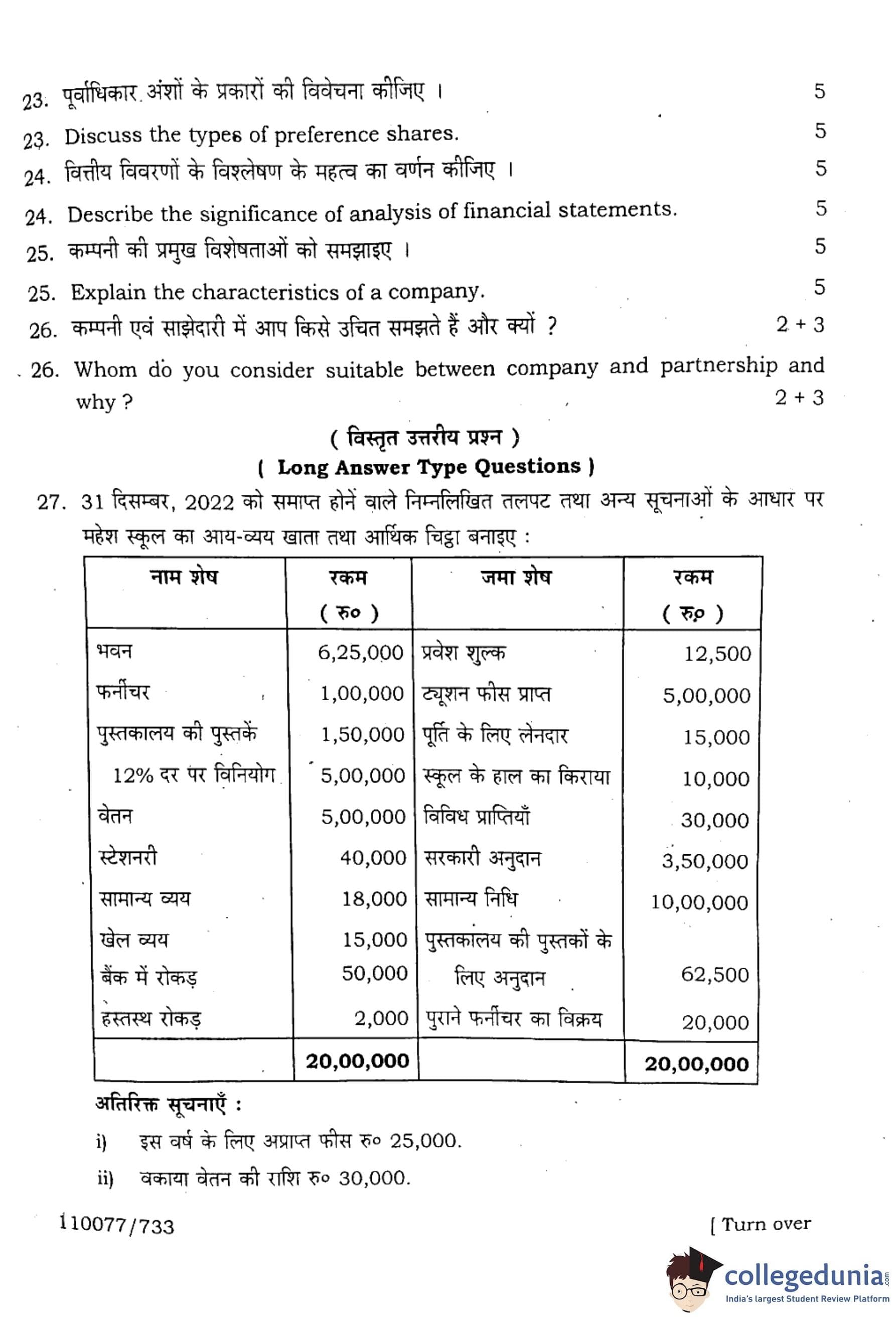

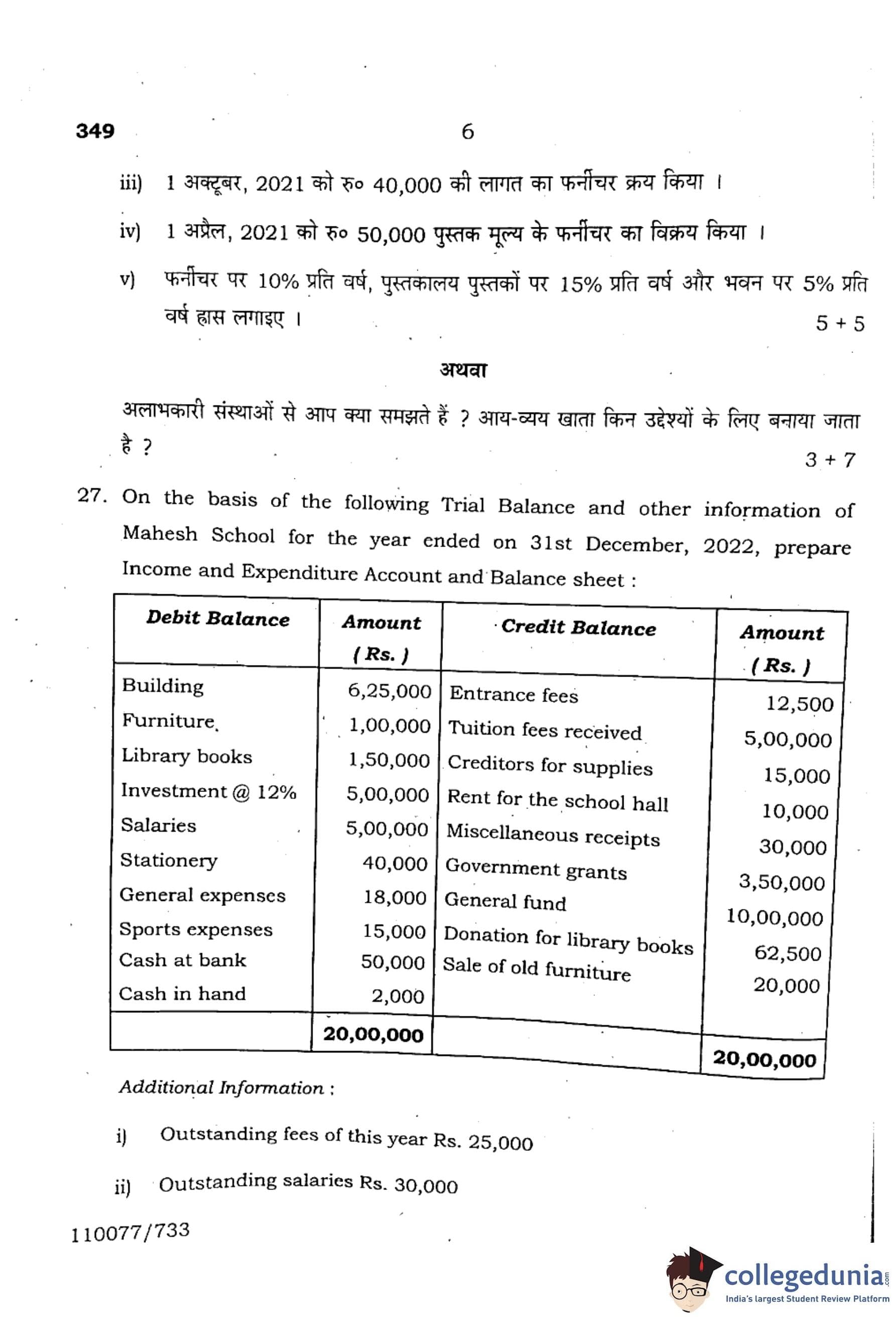

On the basis of the following Trial Balance and other information of Mahesh School for the year ended on 31st December, 2022, prepare Income and Expenditure Account and Balance Sheet:

Additional Information:

Outstanding fees of this year Rs. 25,000.

Outstanding salaries Rs. 30,000.

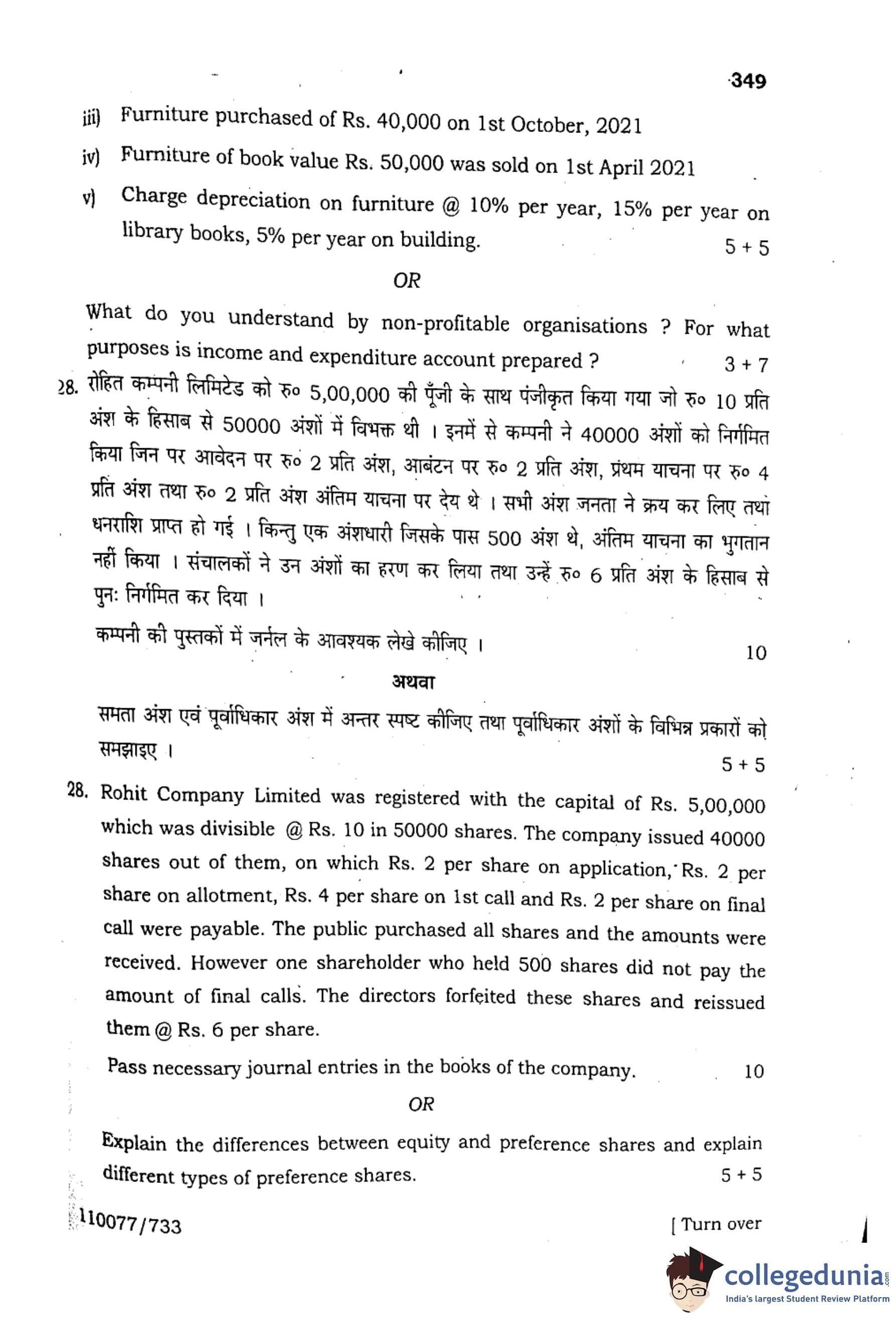

Furniture purchased of Rs. 40,000 on 1st October, 2021.

Furniture of book value Rs. 50,000 was sold on 1st April 2021.

Depreciation on furniture @ 10% per year, 15% per year on library books, 5% per year on building.

What do you understand by non-profitable organisations? For what purposes is income and expenditure account prepared?

Rohit Company Limited was registered with the capital of Rs. 5,00,000, which was divisible @ Rs. 10 in 50,000 shares. The company issued 40,000 shares out of them, on which Rs. 2 per share on application, Rs. 2 per share on allotment, Rs. 4 per share on 1st call and Rs. 2 per share on final call were payable. The public purchased all shares and the amounts were received. However, one shareholder who held 500 shares did not pay the amount of final calls. The directors forfeited these shares and reissued them @ Rs. 6 per share.

Pass necessary journal entries in the books of the company.

Explain the differences between equity and preference shares and explain different types of preference shares.

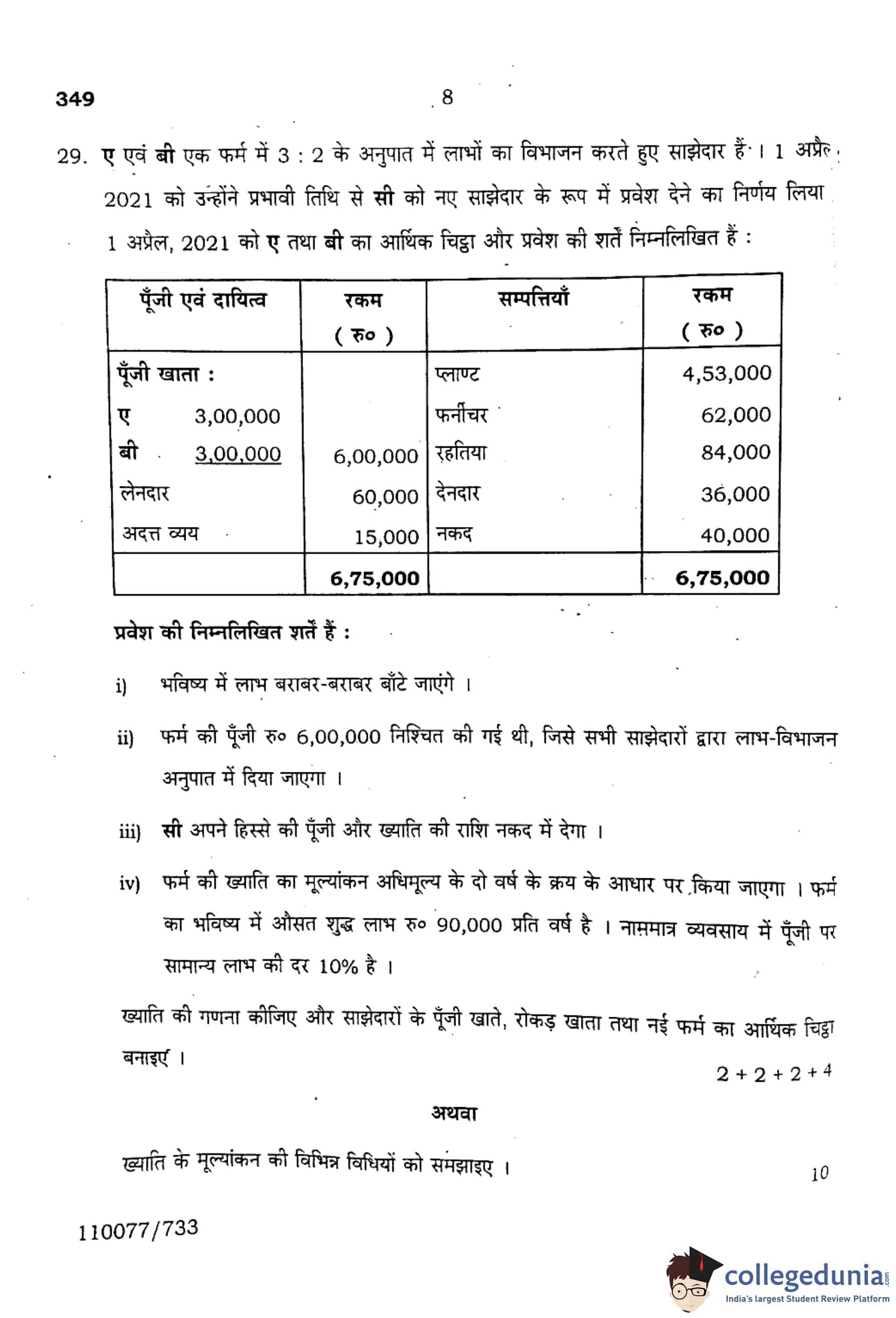

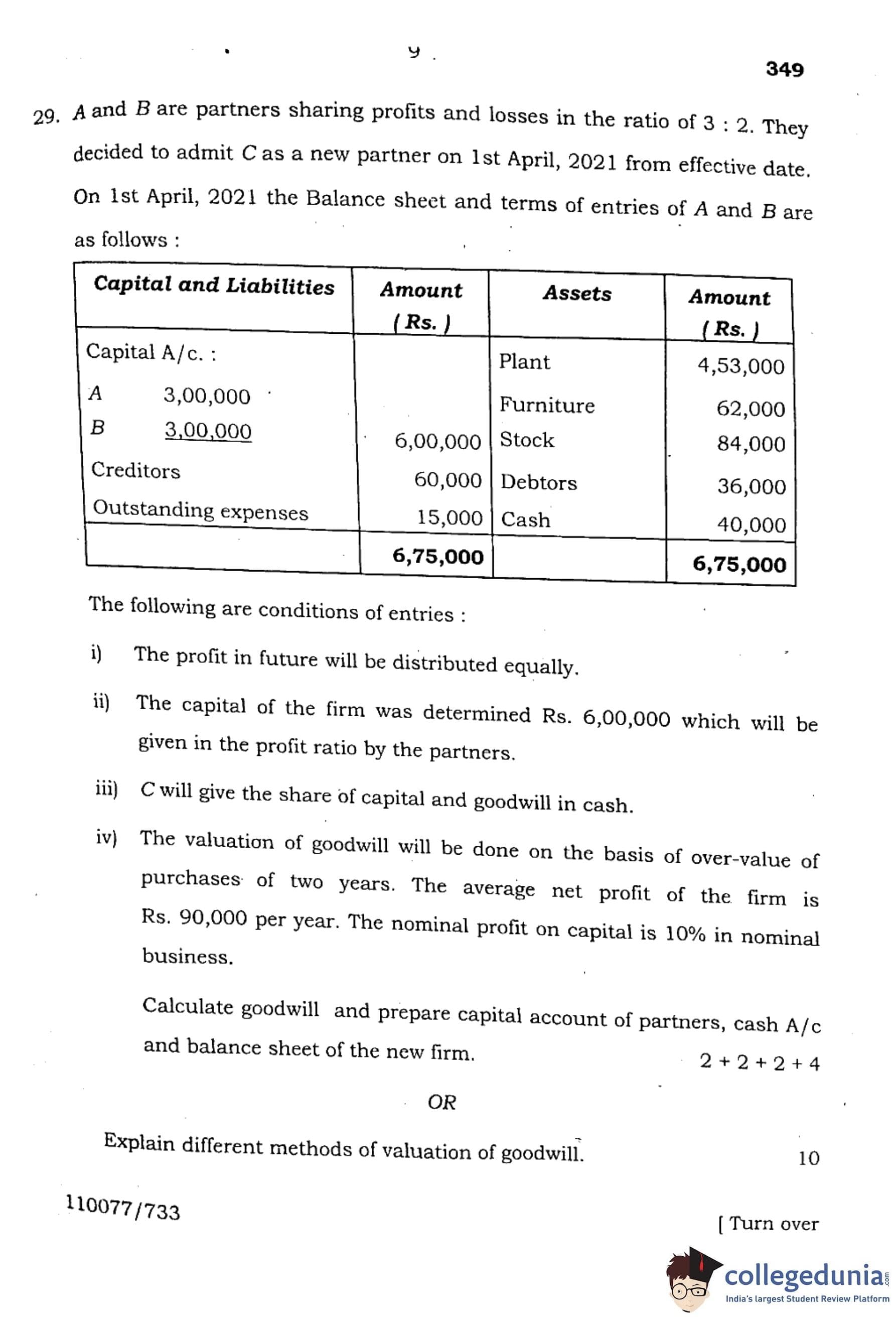

A and B are partners sharing profits and losses in the ratio 3 : 2. They decided to admit C as a new partner on 1st April, 2021 from the effective date. On 1st April, 2021 the Balance Sheet and terms of entries of A and B are as follows:

The following are conditions of entries:

The profit in future will be distributed equally.

The capital of the firm was determined to be Rs. 6,00,000, which will be given in the profit ratio by the partners.

C will give the share of capital and goodwill in cash.

The valuation of goodwill will be done on the basis of over-value of two years’ purchases. The average net profit of the firm is Rs. 90,000 per year. The nominal profit on capital is 10% in nominal business.

Explain different methods of valuation of goodwill.

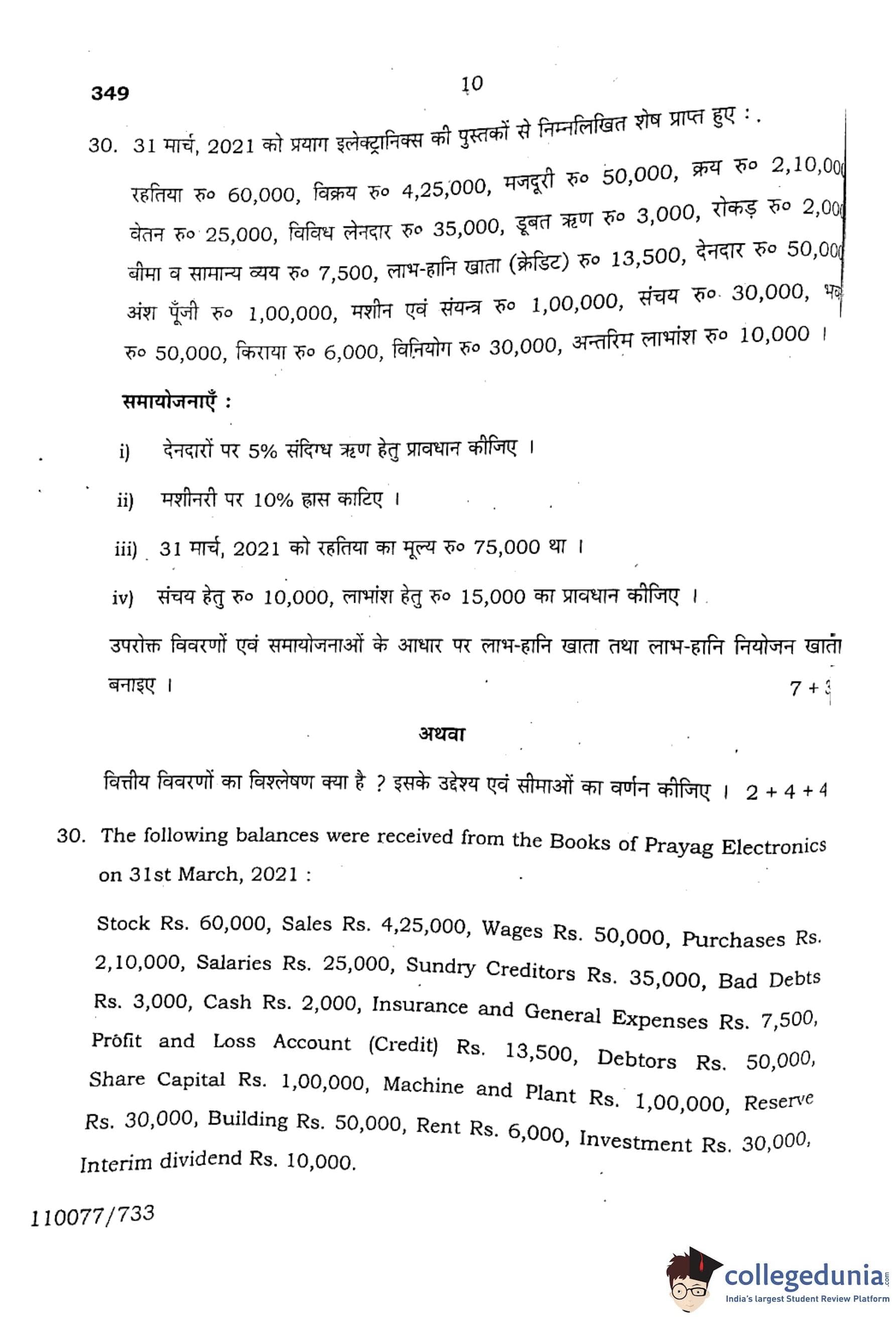

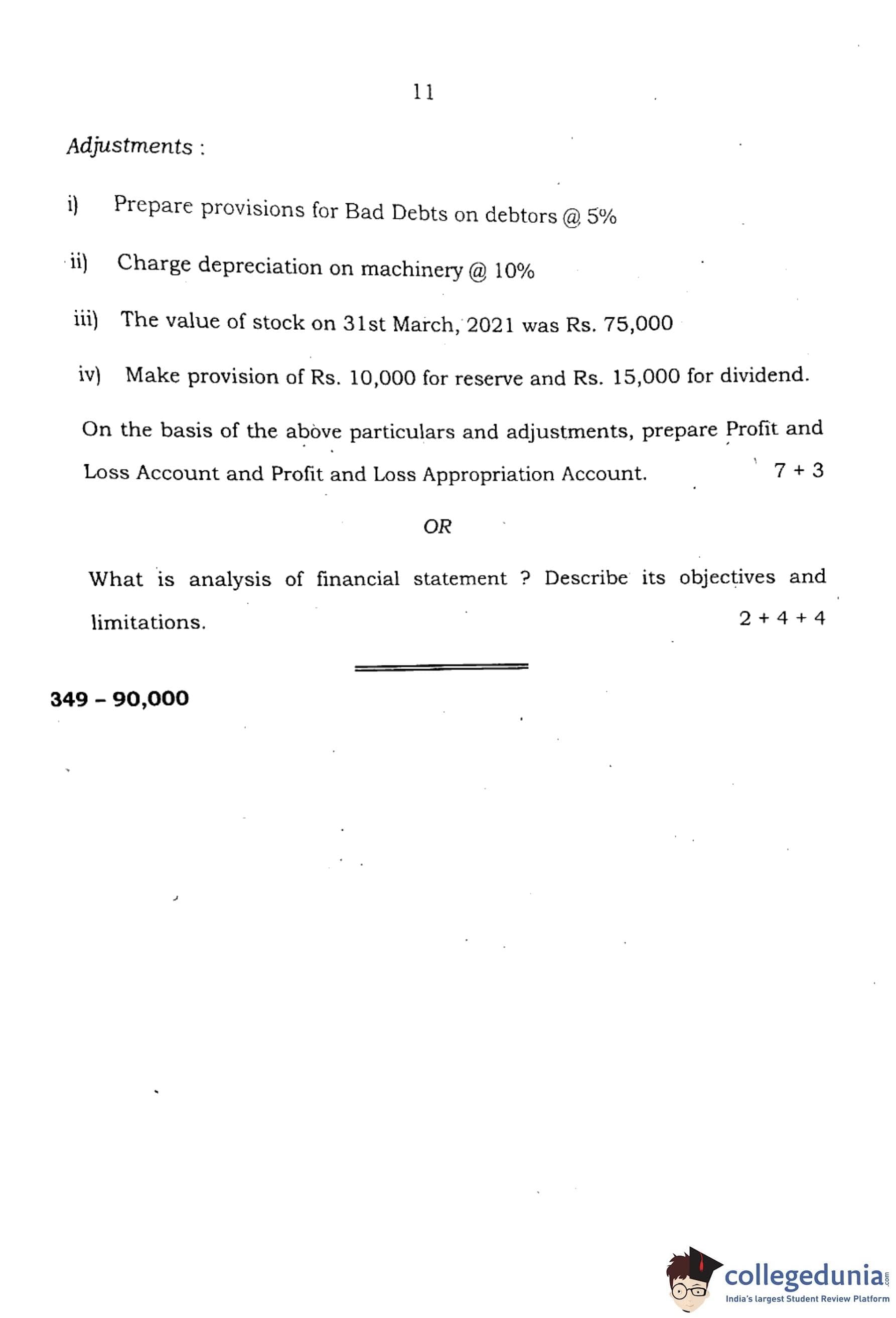

The following balances were received from the Books of Prayag Electronics on 31st March, 2021:

Stock Rs. 60,000, Sales Rs. 4,25,000, Wages Rs. 50,000, Purchases Rs. 2,10,000, Salaries Rs. 25,000, Sundry Creditors Rs. 35,000, Bad Debts Rs. 3,000, Cash Rs. 2,000, Insurance and General Expenses Rs. 7,500, Profit and Loss Account (Credit) Rs. 13,500, Debtors Rs. 50,000, Share Capital Rs. 1,00,000, Machine and Plant Rs. 1,00,000, Reserve Rs. 30,000, Building Rs. 50,000, Rent Rs. 6,000, Investment Rs. 30,000, Interim dividend Rs. 10,000.

Adjustments:

1. Prepare provisions for Bad Debts on debtors @ 5%.

2. Charge depreciation on machinery @ 10%.

3. The value of stock on 31st March, 2021 was Rs. 75,000.

4. Make provision of Rs. 10,000 for reserve and Rs. 15,000 for dividend.

On the basis of the above particulars and adjustments, prepare the Profit and Loss Account and the Profit and Loss Appropriation Account.

What is analysis of financial statement? Describe its objectives and limitations.

Comments