CBSE Class 10 Elements of Book Keeping & Accountancy Question Paper with Answer Key and Solutions PDF is Available Here

The CBSE Class 10 Elements of Book Keeping & Accountancy was conducted on 17th Feb 2024 from 10:30 AM to 13:30 PM. The question paper includes a variety of questions covering different topics in Elements of Book Keeping & Accountancy. The official CBSE previous year question papers are the best and most effective resources to prepare for the upcoming CBSE Class 10 exams. Practicing these papers helps students understand the exam pattern, manage time efficiently, and identify important topics.

You can download the CBSE Class 10 Elements of Book Keeping & Accountancy Question Paper, Answer Key, and Solutions in PDF format here.

CBSE Class 10 ELEMENTS OF BOOK-KEEPING & ACCOUNTANCY Question Paper 2024 Set 4 (135) with Answer Key

| CBSE Class 10 ELEMENTS OF BOOK-KEEPING & ACCOUNTANCY Question Paper 2024 Set 4 (135) with Answer Key | Check Solutions |

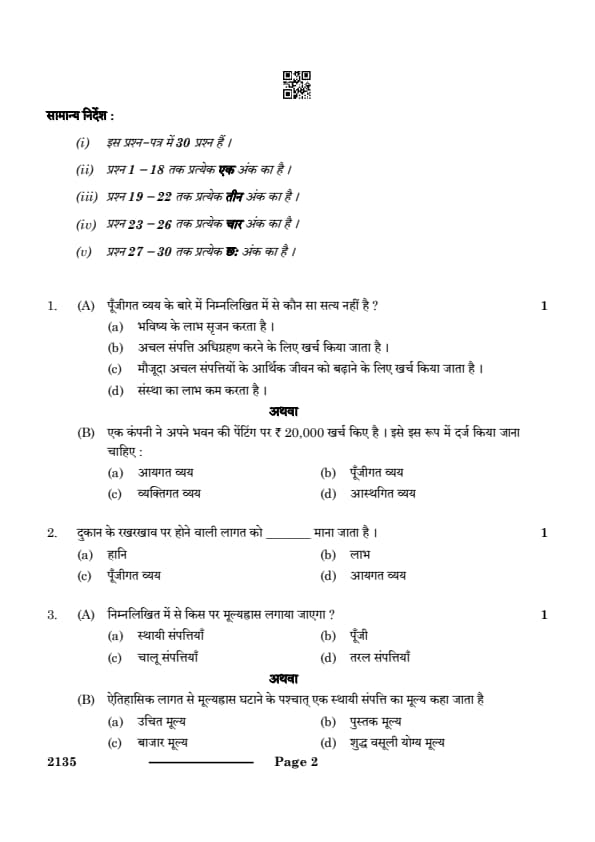

Which of the following is not true about Capital Expenditure?

View Solution

Capital expenditure refers to funds used by a company to acquire, upgrade, or maintain physical assets like buildings, machinery, or equipment. It is typically incurred with the aim of generating future economic benefits over a long period of time. Capital expenditures are considered investments, not expenses, and are capitalized as assets on the balance sheet.

In contrast to operating expenses, which reduce profits in the period they are incurred, capital expenditures do not directly reduce the profit of the concern in the year they are incurred. Instead, they are depreciated over time, which spreads the expense across multiple periods. Therefore, option (d) is incorrect as capital expenditure does not reduce profits immediately but contributes to the creation of long-term value. Quick Tip: Capital expenditure creates future benefits and is recorded as an asset rather than an expense.

A company spent Rs. 20,000 on painting of its building. It should be recorded as:

View Solution

In accounting, expenditures are classified based on their nature and the long-term benefit they provide to the company. Capital expenditures (CapEx) are typically associated with acquiring or improving long-term assets that will benefit the company for many years, such as purchasing machinery or building a new office.

In contrast, revenue expenditures (RevEx) are short-term costs that are necessary to maintain the normal functioning of an existing asset but do not increase its value or extend its useful life significantly.

The expenditure of Rs. 20,000 on painting the building falls under the category of revenue expenditure because it does not improve the building's value or extend its life. It is considered a maintenance cost aimed at keeping the building in a usable condition rather than enhancing it. Since the painting is intended to maintain the current state of the building, it is recorded as a revenue expenditure and directly charged to the income statement in the period it is incurred.

The key characteristic of revenue expenditures is that they are recurring costs that are essential to keep the business running but do not result in an increase in asset value. Therefore, option (a) is correct because it appropriately classifies the painting expense as a revenue expenditure. Quick Tip: Revenue expenditures are generally for maintenance purposes, keeping assets in their current state of operation, and are accounted for as expenses in the income statement.

Cost incurred for the maintenance of a shop is considered as:

View Solution

The maintenance cost of a shop is considered a routine expense incurred to keep the shop's operations running smoothly. These costs do not add any long-term value to the asset or extend its useful life. Maintenance costs are typically treated as Revenue Expenditure, as they are recurring in nature and are necessary for the business to continue functioning on a day-to-day basis.

Unlike capital expenditures (CapEx), which are aimed at enhancing or improving an asset to create future economic benefits, revenue expenditures (RevEx) are short-term costs that are charged to the income statement in the period they are incurred. Since the maintenance does not create future benefits or improve the asset's value, it is treated as an expense and not as a capital expenditure.

Thus, option (d) is correct because the maintenance of the shop is a necessary operational cost, and it is classified as a revenue expenditure. Quick Tip: Routine costs like maintenance, repairs, or upkeep of assets are considered Revenue Expenditure because they ensure the asset continues to function but do not increase its value.

Depreciation will be charged on which of the following?

View Solution

Depreciation is a method of allocating the cost of a tangible fixed asset over its useful life. It is charged to reflect the wear and tear, deterioration, or obsolescence that occurs as the asset is used in business operations over time. Fixed assets, which include long-term assets like machinery, buildings, vehicles, and equipment, are subject to depreciation because they are expected to provide benefits over several years, but their value declines gradually as they are used.

Capital, current assets, and liquid assets, on the other hand, are not depreciated. Capital refers to the funds invested in the business, while current and liquid assets are assets that are expected to be consumed or converted into cash within one year. These assets do not experience depreciation because they are not subject to the same wear and tear as fixed assets. Therefore, depreciation is only applicable to fixed assets, making option (a) the correct choice. Quick Tip: Depreciation is a non-cash expense that applies only to tangible fixed assets that have a limited useful life, such as buildings, machinery, or vehicles.

The value of a fixed asset after deducting depreciation from the historical cost is called:

View Solution

The Book Value of a fixed asset is the value recorded on the company’s balance sheet after deducting accumulated depreciation from the asset's original or historical cost. Over time, as depreciation is charged, the book value of an asset decreases. The book value represents the remaining value of the asset that has not yet been depreciated.

It is important to note that the book value does not necessarily reflect the current market value or fair value of the asset. The historical cost is used as the basis for calculating the book value, and depreciation is deducted to account for the wear and tear or obsolescence of the asset.

Thus, option (b) is correct because the value after deducting depreciation from the historical cost is known as the book value. Quick Tip: Book value is a historical measure that reflects the asset's value in the books after accounting for depreciation. It differs from market value or fair value, which are influenced by current market conditions.

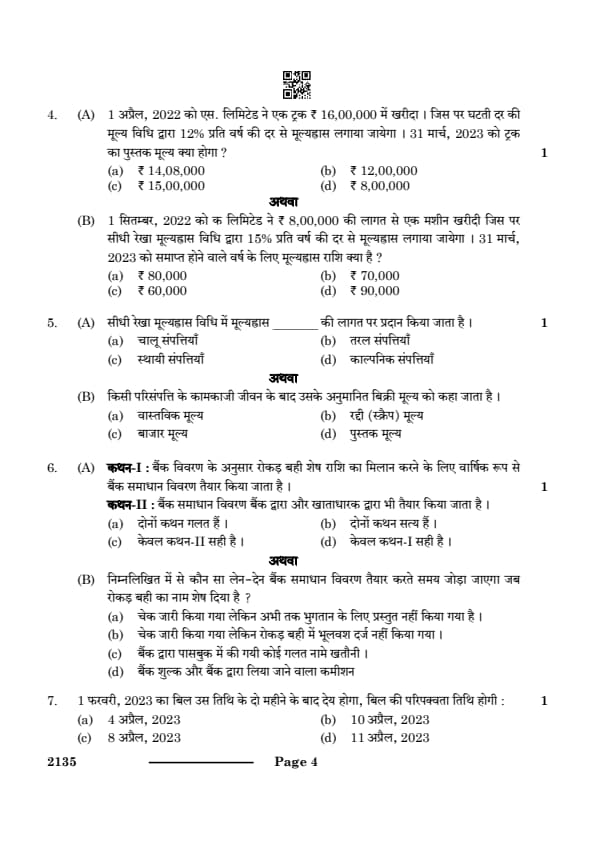

On 1st April, 2022 S. Ltd. purchased a Truck costing Rs. 16,00,000. Depreciation was to be charged @ 12% p.a. by written down value method. What will be the book value of the Truck on 31st March 2023?

View Solution

The depreciation under the Written Down Value (WDV) method is calculated based on the book value of the asset at the start of the year. The formula for depreciation is:

\[ Depreciation = Cost \times Rate of Depreciation \]

Given:

- Cost of the truck = Rs. 16,00,000

- Rate of depreciation = 12%

To calculate the depreciation for the first year, we use the formula:

\[ Depreciation = 16,00,000 \times \frac{12}{100} = Rs. 1,92,000 \]

Next, we calculate the book value at the end of the first year by subtracting the depreciation from the original cost:

\[ Book Value = Cost - Depreciation \] \[ Book Value = 16,00,000 - 1,92,000 = Rs. 14,08,000 \]

Thus, the book value of the truck on 31st March 2023 is Rs. 14,08,000. Quick Tip: In the Written Down Value method, depreciation is charged on the remaining book value each year, which causes the depreciation amount to decrease over time as the asset's value reduces.

On 1st September 2022, A Ltd. purchased a machine costing Rs. 8,00,000. Depreciation was to be charged @ 15% p.a. by straight-line method. What amount of depreciation will be charged for the year ending on March 31, 2023?

View Solution

Under the Straight-Line Method (SLM), depreciation is calculated as:

\[ Depreciation = Cost \times Rate \times Time \]

Given:

Cost = Rs. 8,00,000

Rate = 15%

Time = 7 months (from September to March)

Now, calculating depreciation:

\[ Depreciation = 8,00,000 \times \frac{15}{100} \times \frac{7}{12} \] \[ Depreciation = 8,00,000 \times 0.0875 = Rs. 70,000 \]

Hence, the depreciation for the year ending on March 31, 2023, is Rs. 70,000.

Quick Tip: In the Straight-Line Method, depreciation is calculated on the original cost of the asset, irrespective of its age. This method results in equal depreciation expense every year.

Depreciation is provided in S.L.M. on cost of:

View Solution

Depreciation is a method of allocating the cost of an asset over its useful life. In the case of the **Straight Line Method (S.L.M.)**, depreciation is charged equally over the asset's estimated useful life. This method is applied to Fixed Assets, which are long-term assets such as buildings, machinery, and equipment.

Fixed assets are subject to depreciation because they have a limited useful life, and their value decreases over time due to usage, wear and tear, or obsolescence. In contrast, current assets (e.g., inventory, cash), liquid assets (e.g., cash equivalents), and fictitious assets (e.g., goodwill, deferred charges) do not undergo depreciation since they are either short-term in nature or not subject to the same physical deterioration.

Thus, depreciation is only applicable to fixed assets, and the correct answer is (c) Fixed Assets. Quick Tip: Depreciation spreads the cost of fixed assets over their useful life, ensuring that the asset's cost is matched with the revenue it helps generate over time.

Estimated sale value of an asset after its working life is called:

View Solution

The Scrap Value of an asset is its estimated residual value at the end of its useful life. It represents the expected selling price of the asset after it becomes obsolete or unfit for further use. This value is important in determining how much of the asset's cost is expected to be recovered after its service life has ended.

In accounting, the scrap value is considered when calculating depreciation, particularly in methods like the Straight-Line Method. It is subtracted from the original cost of the asset to determine the total amount of depreciation to be charged over its useful life.

Quick Tip: Scrap value is essential for calculating depreciation using methods like the Straight-Line Method, as it helps in determining the depreciable amount of an asset.

Statement-I: Bank Reconciliation Statement is prepared annually to reconcile balance as per Cash Book with balance as per Bank Statement.

Statement-II: Bank Reconciliation statement is prepared by the bank and also the account holder.

View Solution

- Statement-I is correct: A Bank Reconciliation Statement (BRS) is prepared to reconcile the balance as per the Cash Book and the balance as per the Bank Statement. It helps identify discrepancies between the two records, ensuring accurate financial reporting. Typically, it is prepared more frequently than annually, often monthly, but the general idea remains the same: to reconcile the two balances.

- Statement-II is incorrect: The Bank Reconciliation Statement is prepared by the account holder, not the bank. While the bank provides the bank statement, the responsibility for preparing the BRS lies with the account holder or the accounting department to identify any discrepancies and adjustments that need to be made.

Quick Tip: A Bank Reconciliation Statement (BRS) helps identify errors, omissions, or timing differences between the Cash Book and Bank Statement, ensuring that the financial records are accurate.

Which of the following transaction will be added while preparing Bank Reconciliation statement when debit balance as per Cash Book is given?

View Solution

If a cheque issued is omitted to be recorded in the Cash Book, the balance as per the Cash Book will be lower. While preparing the Bank Reconciliation Statement, this amount must be added back to reconcile the balances. This adjustment ensures that the cash book reflects all transactions, providing an accurate representation of the company's financial position. Adding this amount helps to reconcile the discrepancy between the bank balance and the book balance.

Quick Tip: Ensure all issued cheques are recorded in the Cash Book to avoid discrepancies in the Bank Reconciliation Statement. Regularly updating the Cash Book helps maintain accurate financial records.

A bill dated 1st February, 2023 is payable three months after date. The maturity date of the bill will be:

View Solution

The maturity date of a bill is calculated by adding the specified number of months to the bill's issue date and then considering any grace period. Here, the bill is payable three months after the date.

1. Add 3 months from the bill date (1st February 2023):

- February \(\rightarrow\) March \(\rightarrow\) April.

This brings the due date to 1st May 2023.

2. A grace period of 3 days is added as per the standard practice for bills of exchange.

- 1st May + 3 days = 11th April, 2023.

Thus, the maturity date of the bill is 11th April, 2023. Quick Tip: While calculating the maturity date for bills of exchange, add the given months and include a standard 3-day grace period to determine the exact due date.

The Bill receivable account is a/an:

View Solution

The Bill Receivable Account represents an amount owed to the business, which is an Asset. It is recorded on the asset side of the Balance Sheet under current assets, as it represents amounts the business expects to receive in the near future. Bills Receivable arise when the business accepts a bill from a debtor, and it is a claim for payment that is expected to be realized soon.

Quick Tip: Bills receivable are treated as current assets because they are expected to be realized within a year. These are shown under the current assets section of the Balance Sheet.

Credit balance as per Cash Book was Rs. 30,000, cheque deposited Rs. 5,000 were not credited by bank and cheque issued Rs. 7,000 were not presented for payment. What will be the resulting balance as per Bank Statement?

View Solution

The formula to reconcile the Bank Statement is:

\[ Balance as per Cash Book + Cheques issued but not presented - Cheques deposited but not credited \]

Given:

Balance as per Cash Book = Rs. 30,000

Cheque deposited but not credited = Rs. 5,000 (deduct)

Cheque issued but not presented = Rs. 7,000 (add)

\[ Resulting Balance = 30,000 + 7,000 - 5,000 = Rs. 28,000 \] Quick Tip: To reconcile balances, always add cheques issued but not presented and subtract cheques deposited but not yet credited.

A bank reconciliation statement is –

View Solution

A Bank Reconciliation Statement (BRS) is prepared by the account holder (customer) to reconcile the balance as per the Cash Book and the Bank Pass Book. It identifies any discrepancies caused by timing differences, such as outstanding cheques or deposits in transit, or errors in recording by either the bank or the business. The objective is to ensure that both the Cash Book and the Bank Pass Book reflect the same balance after the reconciliation process.

Quick Tip: The BRS ensures accurate records by reconciling differences between the Bank Pass Book and Cash Book. It is a useful tool for detecting errors and understanding the true financial position.

A Pass Book is a copy of:

View Solution

A Pass Book is a mirror copy of the customer’s account as maintained in the bank’s ledger. It records all the transactions associated with the customer's account, including deposits, withdrawals, interest, and bank charges. Essentially, it represents the bank’s view of the customer’s account, showing the bank’s records of the transactions.

This is why the correct answer is (a), as the Pass Book reflects the bank’s ledger entries regarding the customer’s account. It does not directly reflect the cash book or the firm’s receipts, which are related to other aspects of accounting. Quick Tip: The Pass Book reflects the bank's perspective on a customer’s account and is useful for reconciling any discrepancies between the bank’s and the customer’s records.

Gross profit of the firm was Rs. 1,20,000. There were salary of staff Rs. 50,000 and interest received Rs. 40,000. Net Profit will be ______.

View Solution

The formula for Net Profit is:

\[ Net Profit = Gross Profit - Expenses + Other Income \]

Given:

Gross Profit = Rs. 1,20,000

Expenses (Salary) = Rs. 50,000

Interest Received = Rs. 40,000

Now, calculating the Net Profit:

\[ Net Profit = 1,20,000 - 50,000 + 40,000 = Rs. 1,30,000 \]

Thus, the Net Profit is Rs. 1,30,000.

Quick Tip: Net Profit accounts for all incomes and expenses after calculating the Gross Profit. It gives a clear picture of a company's profitability after all costs and revenues have been accounted for.

Gross profit of the firm was Rs. 5,00,000. Which of the following will result in an increase of Net Profit?

View Solution

The formula for Net Profit is: \[ Net Profit = Gross Profit - Expenses + Other Income \]

Given:

Gross Profit = Rs. 5,00,000

Expenses include: Advertisement, Rent, Repairs (which reduce Net Profit)

Other Income includes: Commission received (which increases Net Profit)

\[ If Commission Received = X then Net Profit = Gross Profit - Total Expenses + X \]

Where \(X\) is the additional income from commission. Quick Tip: Net Profit increases with additional income streams and decreases with additional expenses post-calculating Gross Profit.

When Bank Reconciliation Statement is prepared with credit balance as per Pass Book, the balance derived will be:

View Solution

A Credit Balance in the Pass Book indicates a favorable balance (amount deposited). The corresponding balance in the Cash Book would be a Debit Balance, as the two records are mirror images of each other. This is because the Bank Reconciliation Statement helps reconcile any discrepancies between the balances in both books, and it shows the actual available balance in the Cash Book.

Quick Tip: A credit balance in the Pass Book always corresponds to a debit balance in the Cash Book, as both reflect the same transaction but from different perspectives.

A bill of exchange consists of:

View Solution

A bill of exchange is a financial instrument that contains an order to pay a specific sum of money by one party (the drawee) to another party (the payee) at a specified time. It is different from a promissory note, which contains a promise to pay rather than an order. The drawee is typically a bank or another financial institution, and the bill serves as a method of transferring payment obligations. Quick Tip: A bill of exchange is different from a promissory note as it is an order to pay, not a promise.

Generally, incomplete records are maintained by ____.

View Solution

Incomplete records (also called single-entry accounting) are generally maintained by small traders or individuals who do not follow double-entry accounting due to simplicity and cost constraints. These traders usually record only cash transactions and do not keep a full set of books, making it easier for them to manage limited transactions without the need for complex accounting systems.

Quick Tip: Incomplete records are commonly used by small businesses with limited transactions. It's an easy method but may not provide a complete picture of the financial health of the business.

If capital at the end of the year is Rs. 40,000; Additional Capital introduced during the year Rs. 30,000; drawing for the year Rs. 20,000 and loss for the year is Rs. 60,000, then capital at the beginning of the year was:

View Solution

The formula to calculate capital at the beginning of the year is:

\[ Capital at Beginning = Capital at End - Additional Capital + Drawings + Loss \]

Given:

Capital at End = Rs. 40,000

Additional Capital = Rs. 30,000

Drawings = Rs. 20,000

Loss = Rs. 60,000

\[ Capital at Beginning = 40,000 - 30,000 + 20,000 + 60,000 = Rs. 70,000 \] Quick Tip: Capital at the beginning can be derived by adjusting additional capital, drawings, and profit/loss to the closing capital.

Balance Sheet shows:

View Solution

A Balance Sheet is a financial statement that shows the financial position of a business at a specific date. It reports the assets, liabilities, and equity of the business, helping stakeholders understand the company's financial health. The Balance Sheet provides a snapshot of what the business owns (assets) and owes (liabilities), as well as the net worth (equity) of the company at a particular point in time.

Quick Tip: The Balance Sheet reflects the company's financial health, including what it owns and owes. It does not show profit or loss, which is reported separately in the Profit and Loss statement.

Excess of debit in Profit and Loss Account is called:

View Solution

If the debit side of the Profit and Loss Account exceeds the credit side, it indicates a Net Loss. This happens when total expenses exceed total revenues, meaning the business has spent more than it has earned during the accounting period. Quick Tip: Net loss occurs when a business's expenses are greater than its revenue in a given accounting period.

Closing Stock is shown on the ____.

View Solution

Closing Stock is shown on the Credit side of the Trading Account. It represents the unsold goods at the end of an accounting period. The closing stock is added to the trading account to calculate the cost of goods sold. Additionally, it is shown as a current asset in the Balance Sheet, as it reflects the value of inventory still held by the business.

Quick Tip: Closing Stock appears on the credit side of the Trading Account to match against the cost of goods sold. This helps in determining the gross profit or loss for the period.

Rent from Tenant is shown on the ____.

View Solution

Rent from Tenant is an income for the business and is shown on the Credit side of the Profit and Loss Account. This helps in determining the net profit or loss of the business. Although the question suggests the Debit side, rent is actually shown on the Credit side as income, not as an expense. Quick Tip: Incomes like rent received are recorded on the credit side of the Profit and Loss Account.

In single entry system ____ are recorded.

View Solution

The Single Entry System records only cash receipts and cash payments. It does not record credit transactions or maintain a complete double-entry system. This makes it simpler but less accurate, as it misses vital financial details such as credit sales or purchases. Quick Tip: The single entry system is simple and economical but lacks accuracy and completeness as it omits credit transactions.

Give any three examples of Capital expenditure.

2. Installation of new machinery.

3. Expenditure incurred to extend the life of existing fixed assets.

View Solution

Capital Expenditure refers to spending incurred to acquire or improve fixed assets, which provide long-term benefits to the business. These expenditures are not recorded as expenses in the Profit and Loss account but are capitalized and appear as assets on the Balance Sheet. Capital expenditures typically result in increased productive capacity or extended asset life, and they contribute to the overall growth of the business. Examples of capital expenditure include the purchase of land, installation of machinery, or repairs that enhance the life of existing assets.

Quick Tip: Capital expenditures are non-recurring and appear as assets on the Balance Sheet, not in the Profit \& Loss Account. This distinguishes them from revenue expenditures, which are short-term costs.

Rita incurred the following expenditure on various items during the year ended 31st March, 2023. Identify the name/type of expenditure.

(a) Capital Expenditure

(b) Revenue Expenditure

(c) Capital Expenditure

View Solution

1. Installation of a new machine: This is Capital Expenditure as it creates a new fixed asset providing long-term benefits. It will be capitalized and reflected on the Balance Sheet as an asset.

2. Repairs due to negligence: This is Revenue Expenditure as it is recurring and does not create a new asset. It is considered an operational cost and is charged to the Profit and Loss Account.

3. Air-conditioning for the office: This is Capital Expenditure as it improves the value and functionality of the office, providing long-term benefits. The cost will be capitalized as an asset.

Quick Tip: Capital expenditures create or improve fixed assets, while revenue expenditures maintain the existing assets without increasing their value.

Under which method of charging depreciation more amount is charged in the initial years as compared to the later years of its life? Give any two merits of this method.

View Solution

The Written Down Value (WDV) Method charges depreciation on the book value of the asset, which decreases over time. As a result, higher depreciation is charged in the initial years, and the amount decreases in later years.

Merits of the WDV Method:

1. It matches depreciation expense with the asset's usage, which is typically higher in the initial years.

2. It reduces the tax burden in the early years, as higher depreciation leads to lower taxable profits. Quick Tip: The WDV method is suitable for assets that lose value rapidly in their initial years, such as machinery and vehicles.

On 1st January, 2023, X sold goods to Y for Rs. 50,000. On the same date X drew a bill on Y for Rs. 50,000 due after three months. Y accepted the bill and returned it to X. X retained the bill till the due date, and Y met the bill on due date. Pass journal entries for the above transactions in the books of X.

View Solution

The following journal entries will be recorded in the books of X:

| Date | Particulars | Debit (Rs.) | Credit (Rs.) |

|---|---|---|---|

| 1st Jan 2023 | Y's A/c Dr. | 50,000 | |

| To Sales A/c | 50,000 | ||

| (Being goods sold to Y on credit) | |||

| 1st Jan 2023 | Bills Receivable A/c Dr. | 50,000 | |

| To Y's A/c | 50,000 | ||

| (Being bill accepted by Y and retained by X) | |||

| 1st April 2023 | Cash/Bank A/c Dr. | 50,000 | |

| To Bills Receivable A/c | 50,000 | ||

| (Being bill honored by Y on maturity date) |

Quick Tip: Bills receivable are treated as assets in the books of the drawer and are honored when paid by the drawee on the due date.

On 1st December, 2023 Z purchased goods from R for Rs. 35,000 and accepted a bill for two months. The bill was met on due date. Pass journal entries for the above transactions in the books of Z.

View Solution

The following journal entries will be recorded in the books of Z:

| Date | Particulars | Debit (Rs.) | Credit (Rs.) |

|---|---|---|---|

| 1st Dec 2023 | Purchases A/c Dr. | 35,000 | |

| To R's A/c | 35,000 | ||

| (Being goods purchased on credit) | |||

| 1st Dec 2023 | R's A/c Dr. | 35,000 | |

| To Bills Payable A/c | 35,000 | ||

| (Being bill accepted by Z) | |||

| 1st Feb 2024 | Bills Payable A/c Dr. | 35,000 | |

| To Cash/Bank A/c | 35,000 | ||

| (Being bill met on maturity date) |

Quick Tip: Bills payable are treated as liabilities in the books of the acceptor and must be settled on the maturity date to avoid dishonor.

On 15th March, 2023 Y accepted a bill drawn upon him by X for four months for Rs. 10,000. X discounted the bill on 15th April, 2023 at 18% p.a. from his bank and Y met the bill on maturity. Give the Journal Entries in the books of X and Y.

View Solution

The following journal entries will be recorded in the books of X and Y:

In the books of X:

| Date | Particulars | Debit (Rs.) | Credit (Rs.) |

|---|---|---|---|

| 15th March 2023 | Bills Receivable A/c Dr. | 10,000 | |

| To Y's A/c | 10,000 | ||

| (Being bill drawn and accepted by Y) | |||

| 15th April 2023 | Bank A/c Dr. | 9,850 | |

| Discount A/c Dr. | 150 | ||

| To Bills Receivable A/c | 10,000 | ||

| (Being bill discounted at 18% p.a. for 4 months) | |||

| 15th July 2023 | No Entry (Bill met by Y) |

In the books of Y:

| Date | Particulars | Debit (Rs.) | Credit (Rs.) |

|---|---|---|---|

| 15th March 2023 | X's A/c Dr. | 10,000 | |

| To Bills Payable A/c | 10,000 | ||

| (Being bill accepted in favor of X) | |||

| 15th July 2023 | Bills Payable A/c Dr. | 10,000 | |

| To Cash/Bank A/c | 10,000 | ||

| (Being bill honored on maturity date) |

Quick Tip: When a bank discounts bills, they deduct the interest upfront. This discount must be recorded as an expense.

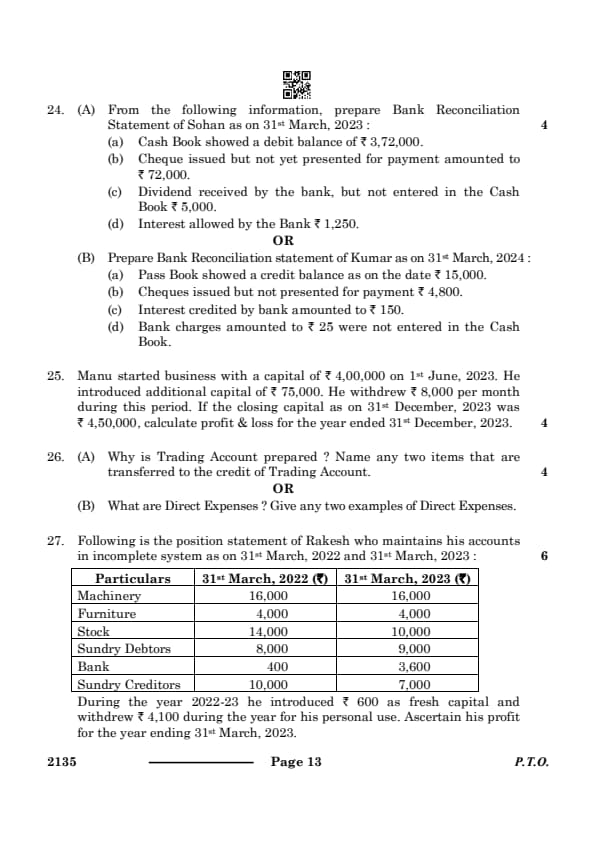

From the following information, prepare Bank Reconciliation Statement of Sohan as on 31st March, 2023:

(a) Cash Book showed a debit balance of Rs. 3,72,000.

(b) Cheque issued but not yet presented for payment amounted to Rs. 72,000.

(c) Dividend received by the bank, but not entered in the Cash Book Rs. 5,000.

(d) Interest allowed by the Bank Rs. 1,250.

View Solution

Bank Reconciliation Statement of Sohan as on 31st March, 2023:

| Particulars | Add (Rs.) | Less (Rs.) |

|---|---|---|

| Debit balance as per Cash Book | 3,72,000 | |

| Cheque issued but not yet presented | 72,000 | |

| Dividend received by bank (not entered in Cash Book) | 5,000 | |

| Interest allowed by bank | 1,250 | |

| Adjusted Balance as per Bank Statement | 4,50,250 |

Explanation:

1. Cheques issued but not yet presented for payment increase the Bank Statement balance.

2. Dividend and interest allowed by the bank increase the balance, but these were not recorded in the Cash Book.

Quick Tip: Add any receipts or credits not recorded in the Cash Book and deduct outstanding payments when reconciling balances.

Prepare Bank Reconciliation statement of Kumar as on 31st March, 2024:

(a) Pass Book showed a credit balance as on the date Rs. 15,000.

(b) Cheques issued but not presented for payment Rs. 4,800.

(c) Interest credited by bank amounted to Rs. 150.

(d) Bank charges amounted to Rs. 25 were not entered in the Cash Book.

View Solution

Bank Reconciliation Statement of Kumar as on 31st March, 2024:

| Particulars | Add (Rs.) | Less (Rs.) |

|---|---|---|

| Credit balance as per Pass Book | 15,000 | |

| Cheque issued but not presented | 4,800 | |

| Interest credited by bank | 150 | |

| Bank charges not recorded in Cash Book | 25 | |

| Adjusted Balance as per Cash Book | 19,950 |

Explanation:

1. Cheques issued but not presented increase the balance in the Pass Book.

2. Interest credited by the bank increases the Pass Book balance.

3. Bank charges reduce the balance.

Quick Tip: Always adjust for unrecorded transactions like bank charges and interest when preparing the Bank Reconciliation Statement.

Manu started business with a capital of Rs. 4,00,000 on 1st June, 2023. He introduced additional capital of Rs. 75,000. He withdrew Rs. 8,000 per month during this period. If the closing capital as on 31st December, 2023 was Rs. 4,50,000, calculate profit \& loss for the year ended 31st December, 2023.

View Solution

The formula to calculate profit/loss is:

\[ Profit/Loss = Closing Capital - Opening Capital - Additional Capital + Drawings \]

Given:

- Opening Capital = Rs. 4,00,000

- Additional Capital = Rs. 75,000

- Withdrawals = Rs. 8,000 per month for 7 months (June to December):

\[ Drawings = 8,000 \times 7 = Rs. 56,000 \]

- Closing Capital = Rs. 4,50,000

Calculation:

\[ Profit/Loss = 4,50,000 - 4,00,000 - 75,000 + 56,000 \] \[ Profit/Loss = Rs. 31,000 \, (Profit). \] Quick Tip: To determine profit or loss using the capital approach, adjust for additional capital introduced and drawings made during the period.

Why is Trading Account prepared? Name any two items that are transferred to the credit of Trading Account.

View Solution

The Trading Account is prepared to determine the Gross Profit or Gross Loss of a business during an accounting period. It records direct incomes and direct expenses related to the core business operations.

Two items transferred to the credit of Trading Account:

1. Sales (Net Sales).

2. Closing Stock. Quick Tip: The Trading Account focuses on direct transactions, like purchases and sales, to ascertain Gross Profit or Loss.

What are Direct Expenses? Give any two examples of Direct Expenses.

View Solution

Direct Expenses are costs directly attributable to the production of goods or rendering of services. These expenses are incurred during the manufacturing or trading activities and are essential for generating revenue.

Two examples of Direct Expenses:

1. Wages paid for production.

2. Carriage Inwards.

Quick Tip: Direct expenses are directly related to the production process and are debited to the Trading Account. They are essential for calculating the cost of goods sold.

Following is the position statement of Rakesh who maintains his accounts in incomplete system as on 31st March, 2022 and 31st March, 2023:

| Particulars | 31st March, 2022 (Rs.) | 31st March, 2023 (Rs.) |

|---|---|---|

| Machinery | 16,000 | 16,000 |

| Furniture | 4,000 | 4,000 |

| Stock | 14,000 | 10,000 |

| Sundry Debtors | 8,000 | 9,000 |

| Bank | 400 | 3,600 |

| Sundry Creditors | 10,000 | 7,000 |

Additional Information:

Fresh Capital introduced = Rs. 600.

Drawings = Rs. 4,100.

View Solution

To calculate the profit, we use the formula:

Profit = Closing Capital - Opening Capital - Fresh Capital Introduced + Drawings

Step 1: Calculate Capital at the beginning and end of the year.

Opening Capital (as on 31st March, 2022):

Assets - Liabilities = (16,000 + 4,000 + 14,000 + 8,000 + 400) - 10,000 = 32,400

Closing Capital (as on 31st March, 2023):

Assets - Liabilities = (16,000 + 4,000 + 10,000 + 9,000 + 3,600) - 7,000 = 35,600

Step 2: Apply the formula.

Profit = Closing Capital - Opening Capital - Fresh Capital Introduced + Drawings

Profit = 35,600 - 32,400 - 600 + 4,100 = Rs. 6,700

Conclusion: The profit for the year ending 31st March, 2023 is Rs. 6,700. Quick Tip: When using the incomplete records system, always calculate capital as Assets minus Liabilities to determine profit or loss.

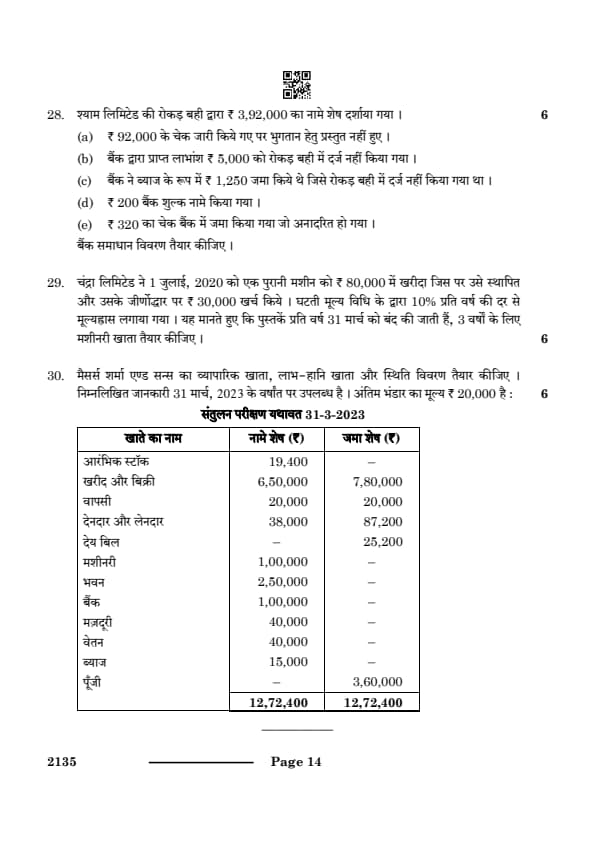

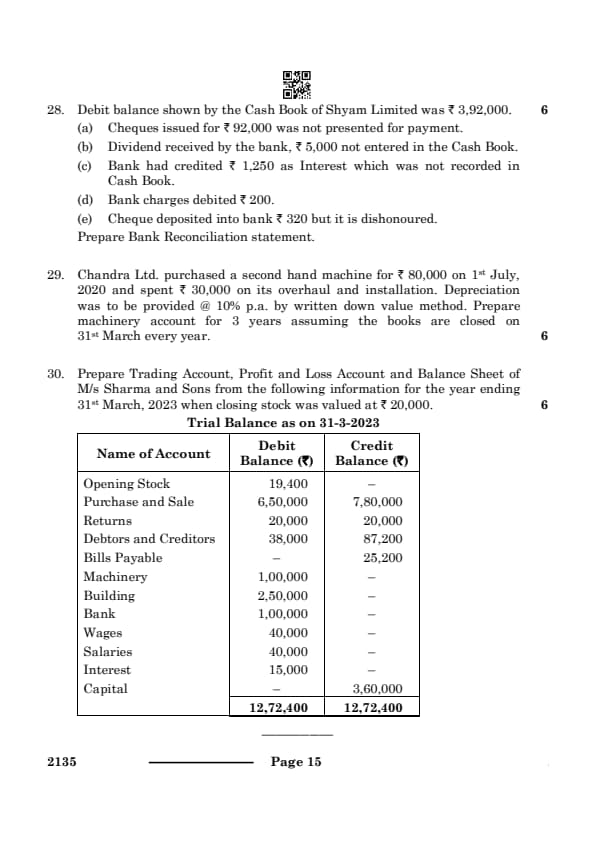

Debit balance shown by the Cash Book of Shyam Limited was Rs. 3,92,000.

View Solution

Bank Reconciliation Statement of Shyam Limited as on 31st March:

| Particulars | Add (Rs.) | Less (Rs.) |

|---|---|---|

| Debit balance as per Cash Book | 3,92,000 | |

| Cheques issued but not presented | 92,000 | |

| Dividend received by bank | 5,000 | |

| Interest credited by bank | 1,250 | |

| Bank charges debited | 200 | |

| Cheque dishonoured | 320 | |

| Adjusted Balance as per Bank Statement | 4,90,050 |

Quick Tip: When preparing a Bank Reconciliation Statement, add unrecorded receipts and subtract any unrecorded payments or dishonoured cheques. This ensures that the cash book and bank statement are aligned.

Chandra Ltd. purchased a second-hand machine for Rs. 80,000 on 1st July, 2020 and spent Rs. 30,000 on its overhaul and installation. Depreciation was to be provided @ 10% p.a. by written down value method. Prepare machinery account for 3 years assuming the books are closed on 31st March every year.

View Solution

Machinery Account (WDV Method)

| Date & Particulars | Debit (Rs.) | Credit (Rs.) | |

|---|---|---|---|

| 2020 | |||

| 1st July | To Bank A/c (Cost + Installation) | 1,10,000 | |

| 31st March | By Depreciation A/c (10% on Rs. 1,10,000) | 11,000 | |

| 31st March | By Balance c/d | 99,000 | |

| 2021 | |||

| 1st April | To Balance b/d | 99,000 | |

| 31st March | By Depreciation A/c (10% on Rs. 99,000) | 9,900 | |

| 31st March | By Balance c/d | 89,100 | |

| 2022 | |||

| 1st April | To Balance b/d | 89,100 | |

| 31st March | By Depreciation A/c (10% on Rs. 89,100) | 8,910 | |

| 31st March | By Balance c/d | 80,190 |

Quick Tip: The Written Down Value (WDV) method applies depreciation on the book value at the beginning of each year.

Prepare Trading Account, Profit and Loss Account, and Balance Sheet of M/s Sharma and Sons from the following information for the year ending 31st March, 2023 when closing stock was valued at Rs. 20,000.

Trial Balance as on 31-3-2023

| Name of Account | Debit Balance (Rs.) | Credit Balance (Rs.) |

|---|---|---|

| Opening Stock | 19,400 | -- |

| Purchase and Sale | 6,50,000 | 7,80,000 |

| Returns | 20,000 | 20,000 |

| Debtors and Creditors | 38,000 | 87,200 |

| Bills Payable | -- | 25,200 |

| Machinery | 1,00,000 | -- |

| Building | 2,50,000 | -- |

| Bank | 10,000 | -- |

| Wages | 40,000 | -- |

| Salaries | 40,000 | -- |

| Interest | 15,000 | -- |

| Capital | -- | 3,60,000 |

| Total | 12,72,400 | 12,72,400 |

View Solution

Trading Account for the year ending 31st March, 2023:

| Particulars | Rs. | Particulars | Rs. |

|---|---|---|---|

| Opening Stock | 19,400 | Sales | 7,80,000 |

| Purchases | 6,50,000 | Closing Stock | 20,000 |

| Wages | 40,000 | Gross Loss c/d | 1,09,400 |

| Total | 7,09,400 | Total | 7,09,400 |

Quick Tip: Trading Account helps determine Gross Profit or Loss by comparing direct revenues and expenses.

Comments